- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

The focus of financial markets remains firmly on inflation. Expectations for a decline have been misguided in the past, but we are optimistic that it will now recede. We expect the headwinds that have faced markets to ease.

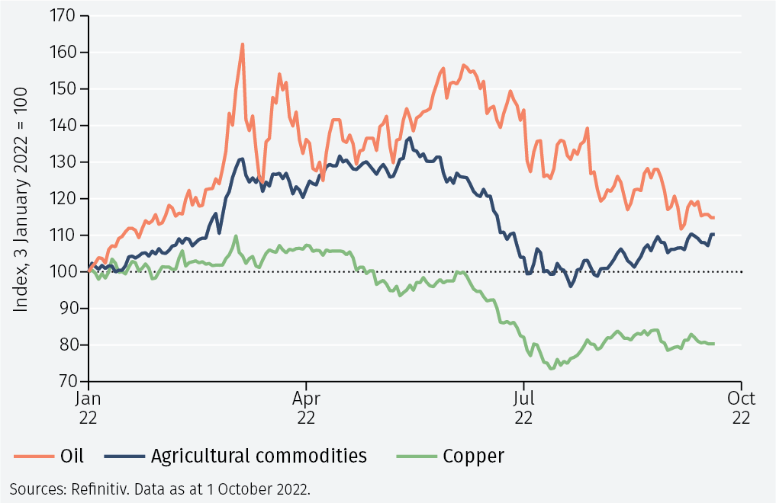

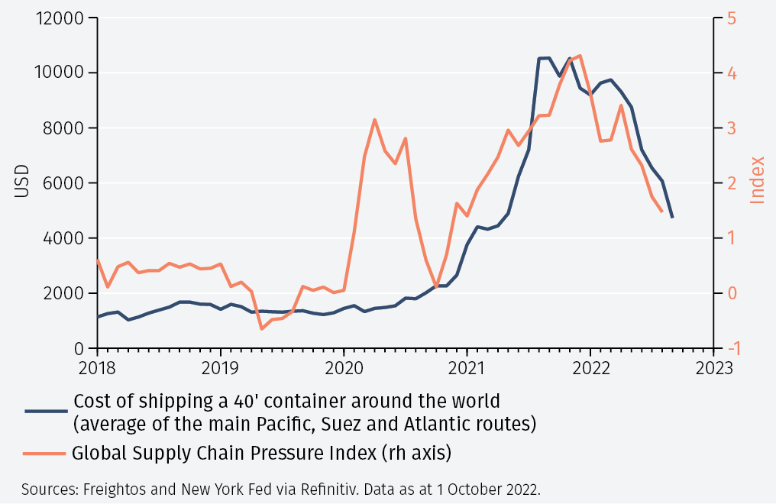

The attention of financial markets in the final months of 2022 will be primarily on one key issue: the path of inflation. In the US, UK and eurozone, markets would like to see a quick return towards 2% central bank targets. That would simultaneously restore policy credibility, ease pressure on interest rates, soothe concerns about an impending recession and underpin equity valuations. A trio of ingredients are in place for those favourable winds to blow. Key commodity prices have fallen back (see Figure 1). Supply chain pressures have eased (see Figure 2). And, from San Francisco to central London, there is a softening of conditions in the housing market. However, optimism about the trend in inflation has been misplaced throughout 2022. There is, therefore, a good deal of nervousness about whether the decline will materialise.

Rear view mirror

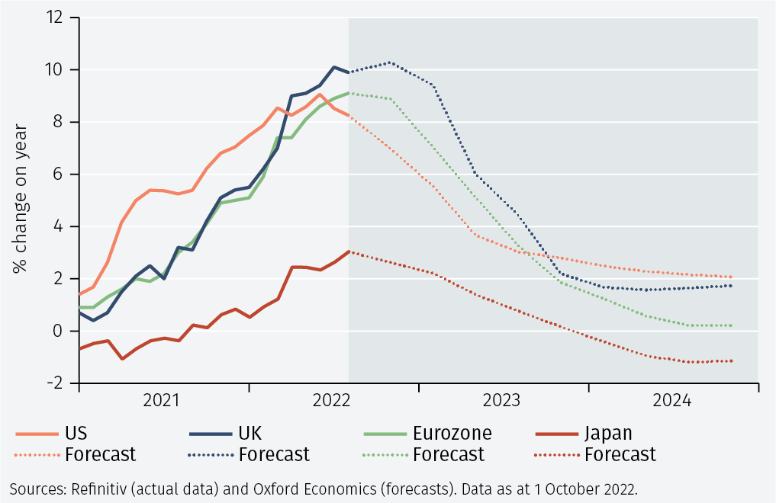

We are cautiously optimistic that as we travel through late 2022 and into 2023, the inflation spike will retreat into the distance. Projections from one mainstream forecaster are shown in Figure 3. But the journey is unlikely to be smooth.

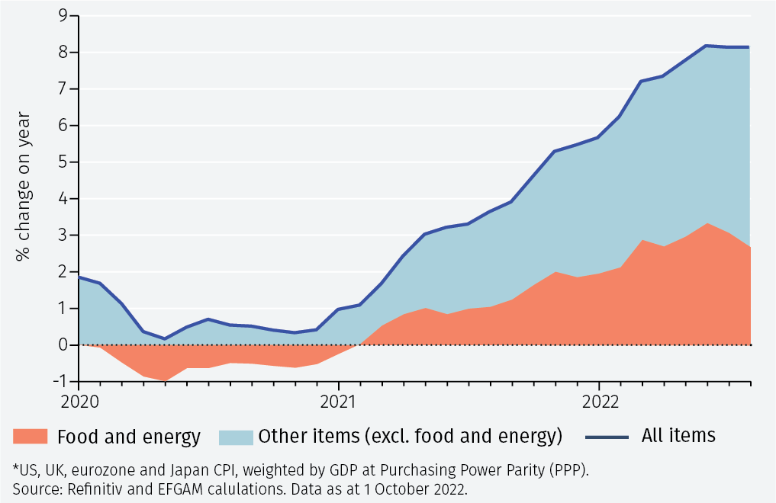

Food and energy prices (often excluded from inflation measures to give a guide to ‘underlying’ conditions) currently contribute more than two percentage points to the average inflation rate in advanced economies. They ‘eat up’ central banks’ inflation allowance. Adding in the contribution from all other items, the average inflation rate in advanced economies is around 8% (see Figure 4). That is not a picture which suggests that central bank interest rate increases can be reversed quickly. Equally, however, we think there will soon come a time when it is appropriate for them to pause and to assess the tightening which has already taken place. That is especially the case in those economies (notably the US and UK) where important market interest rates (particularly for mortgages and corporate debt) have already risen sharply. In that sense, financial markets have already effected a tightening.

Obstacles in the road

Although we are optimistic about a retreat in inflation rates, there are two main obstacles in the road ahead. First, in the US economy, ‘shelter’ costs – actual and implied rents – account for around one-third of the consumer price index. They tend to lag the trend in house prices. So, the most recent softening of house prices may well not show up in lower consumer price inflation for some time. Second, and much more fundamentally, for two decades the world appears to have been in a state of continued crisis. The global financial crisis morphed into the eurozone crisis; the Russian invasion of Ukraine came before the Covid pandemic was fully in retreat; and the current cost of living crisis is part of a bigger energy security and climate change crisis. By their very nature such crises are hard to predict: we simply do not know what might lie ahead.

Of course, the policy response to such crises in the past has been to ease monetary policy - to cut interest rates and expand quantitative easing1 and, more recently, use various fiscal support measures (such as the furlough schemes in response to the Covid pandemic and energy price caps in response to higher oil and gas prices). The big question raised by this is whether such activism can be expected in the future.

Large reversals in policy interest rates have followed previous tightening periods, notably in the US. That may happen again but fiscal policy flexibility is limited. The reaction to recent UK fiscal largesse (a weaker value of sterling, a rise in UK gilt yields, a rebuke from the IMF and unprecedented Bank of England intervention to support the government bond market) is a warning signal for other policymakers considering easing.

The rise in government bond yields we have seen in 2002 can also be seen as an overdue adjustment to low rates. For some time we have highlighted the unusually low, indeed often negative, levels of real bond yields, such as those on Treasury Inflation-Protected Securities (see Figure 5). These have now reverted to positive, albeit still low, rates. Although that 2022 reversal in real interest rates has been rapid and has caused some market dislocation, we see positive rates as generally a good sign of appropriate market pricing.

Higher interest rates and bond yields have heightened concerns about recession. Certainly, in continental Europe, the area most directly affected by the war in Ukraine, a near-term recession seems likely; but for the US we still judge any recession as unlikely before 2023 and, even then, mild. Excess savings built in the pandemic still remain high and will help cushion any downturn in consumer spending (see Figure 6).

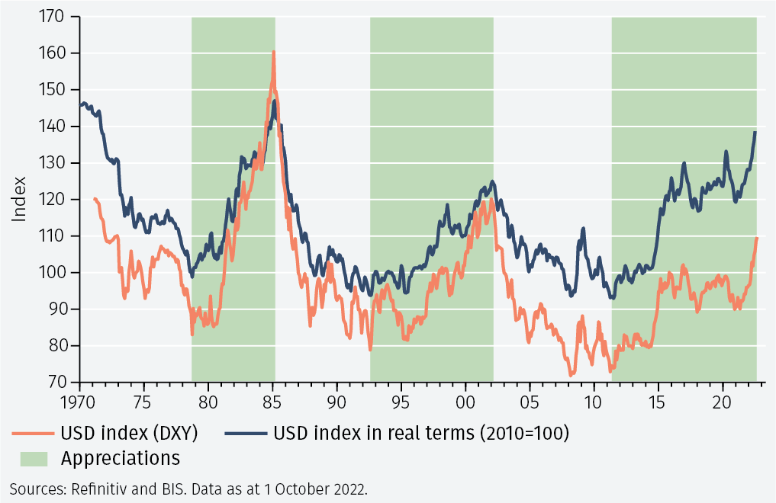

US dollar strength

The other key issue, looking ahead, is whether the US dollar can continue strengthening (see Figure 7). The relative stance of monetary policy (a pause in US tightening as other economies catch up) and the fact that the dollar is nearing historic peaks in real terms suggest to us that the favourable winds helping the dollar will recede.

To continue reading, please download the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.