- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the latest Swiss National Bank monetary policy decision and at the outlook for Swiss interest rates.

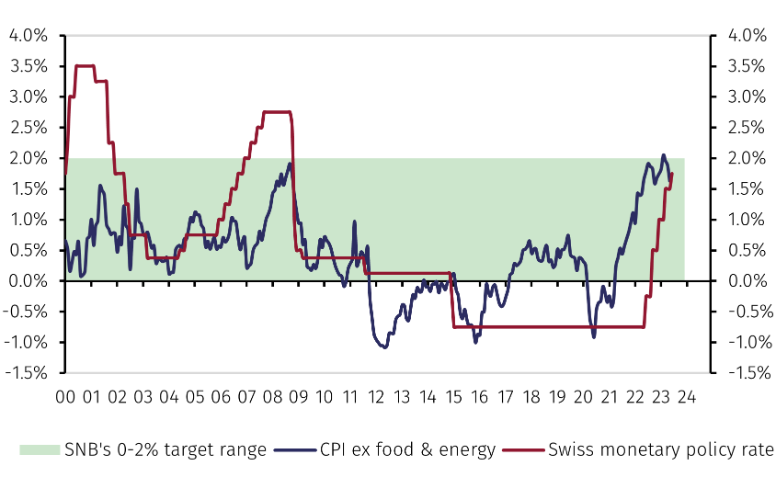

On 22 June the Swiss National Bank (SNB) increased the policy rate by 0.25%, a smaller step than at previous meetings, bringing it to 1.75% (see Chart 1). The smaller size of the rate adjustment acknowledges that the peak in rates is now close. However, another 0.25% rate increase in September is a possibility. The SNB repeated that additional rate rises “cannot be ruled out”. Furthermore, the central bank remains “willing” to sell foreign currency to strengthen the Swiss franc and limit imported inflation.

Source: Refinitiv and EFGAM calculations, data as of 22 June 2023.

The tightening bias reflects the SNB’s concern that inflation will not moderate fast enough. This is best seen in the upward revision of the SNB’s conditional inflation forecast for 2024 and beyond despite lower expected inflation in 2023. The end point of the projection remained at 2.1%, above the 0-2% target range.

Interestingly, the SNB linked the upward revision of inflation to “second round effects, higher electricity prices and rents”, and higher inflation abroad. However, the rise of electricity prices announced for January 2024 are not due to increased demand, meaning monetary policy will have no impact on them, and they will eventually be a drag on GDP growth.

Furthermore, rents, that represent about a fifth of the Swiss CPI basket, will rise because of the indexation to mortgage rates, which have risen following the SNB’s policy tightening. The rent indexation mechanism risks creating a vicious circle where the SNB increases rates to lower inflation, but inflation remains high, if not higher, due to rising rents. To limit such risk, it would make sense for the SNB to also monitor price developments net of rents as currently done by the Riksbank in Sweden, where rents are also indexed to interest rates.

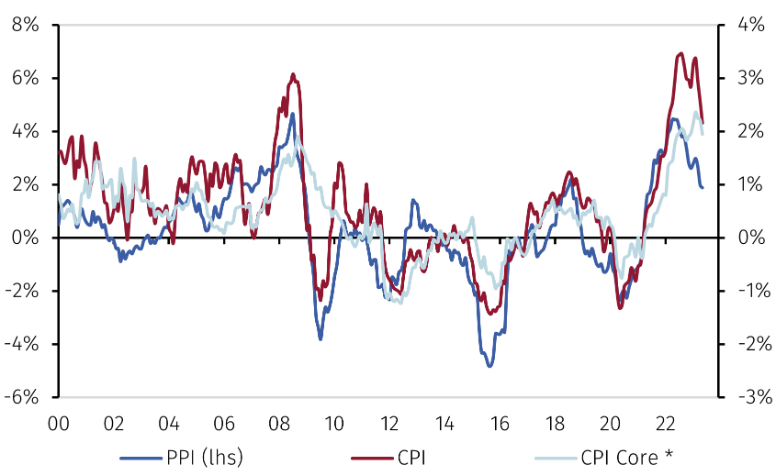

Finally, many indicators, including producer price inflation, already point to a return of inflation to levels consistent with the SNB definition of price stability (see Chart 2).

Source: Refinitiv and EFGAM calculations, data as of 22 June 2023.

To conclude, it is legitimate to ask if, under these circumstances, higher interest rates are appropriate to tame inflation and if they do not risk being too much of a burden for the economy. In its comments, the SNB highlighted the prevalence of downside risks to growth and tighter financing conditions will raise the chances these risks materialise.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.