- Date:

- Author:

- Joaquin Thul and Sam Jochim

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

On 3 August the Bank of England’s (BoE) Monetary Policy Committee (MPC) voted to hike interest rates by 25 basis points to 5.25%. With annual inflation at 7.9%, the central bank is expected to raise rates at least twice more to encourage inflation to return to the 2% target. In this Macro Flash Note, economists Joaquin Thul and Sam Jochim look at the outlook for UK inflation and the implications for the BoE’s next steps.

Following the August meeting, several members of the MPC noted that interest rates in the UK are restrictive for economic activity, but risks to inflation remain tilted to the upside. Sharp increases in energy, food, and other import prices over the last two years have affected domestic prices and wages. These effects are taking longer to unwind than initially anticipated. Hence, despite some recent improvement, annual inflation remains too high at 7.9%.

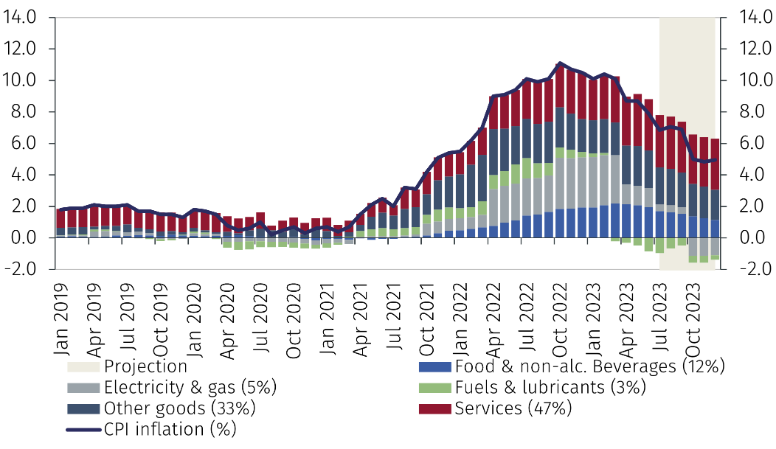

(*) Figures in parentheses are CPI basket weights in 2023.

Source: Bank of England and EFGAM. Data as of 3 August 2023

Nevertheless, economic activity has been more resilient than previously expected. Underlying quarterly GDP growth was around 0.2% in the first half of 2023, with BoE officials expecting a similar rate of growth for the coming quarters. Relative to the previous forecasting round in May, the BoE revised up its projection for GDP growth in 2023 from 0.25% year-on-year (YoY) to 0.5% YoY. However, the BoE’s forecasts are conditioned on the market-implied path of interest rates which, given the persistence of inflation, has shifted up since May. With the higher rates path expected to weigh on demand in 2024 and 2025, GDP growth forecasts have been revised down for those years. The BoE now expects GDP growth to remain around 0.5% YoY in 2024 before slowing to 0.25% in 2025.

MPC members had previously acknowledged they were surprised by the increase in services prices of 7.4% YoY and private sector wage growth of 7.7% YoY in May, prompting a 50bps increase in interest rates at the June meeting. The decision to take a smaller step of 25bps in August was attributed to the improvement in inflation data during the month. After the meeting, MPC members explained that three indicators will be key to assess the future path of monetary policy:

- Services prices. These have been in an uptrend since mid-2021, driven by factors such as rising labour costs that have been slow to build up and are proving slower to unwind. The latest data on prices for services showed an increase of 7.2% YoY, representing a slight improvement from the 7.4% YoY increase in May. Nevertheless, the contribution of services is expected to remain elevated for the rest of 2023 (see Chart 1).

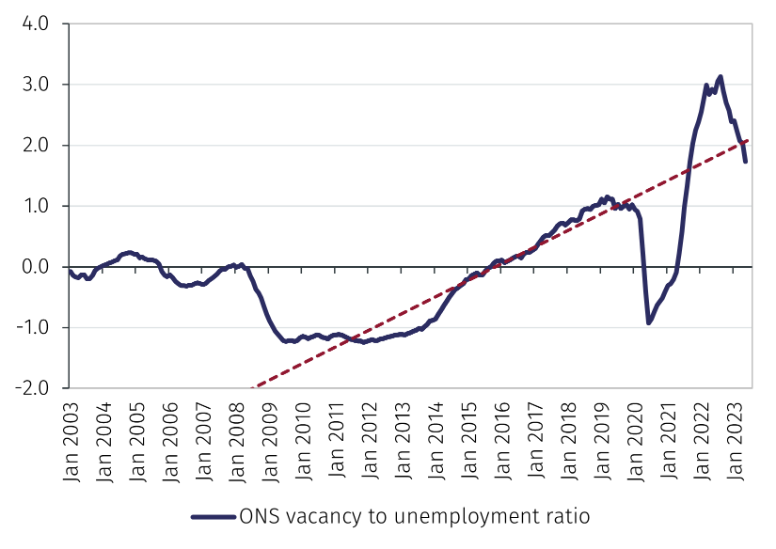

- Labour market. The strength of the labour market has driven improvements in household income following the Covid pandemic. However, some signs of loosening are emerging. The unemployment rate rose to 4.0% in the three months to May and the vacancies-to-unemployment ratio has declined, though it remains above its pre-pandemic level (see Chart 2.1).1

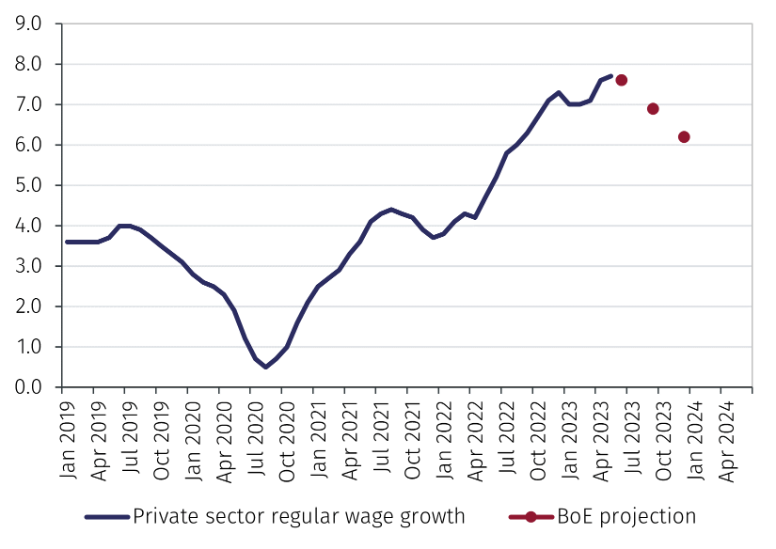

- Wage growth. Despite the tightness in the labour market, which has contributed to the rise in wage growth, some forward-looking indicators suggest that it will moderate in the second half of 2023. Indicators of private sector earnings growth, estimated by the BoE and the Office for National Statistics, show that wage growth is close to peaking and should decline to around 6% by year-end (see Chart 2.2).

Source: Bank of England and EFGAM. Data as of 3 August 2023

If, as we expect, the growth in services prices gradually declines, and labour market conditions continue to loosen, which contributes to wage growth moderating, then the MPC is likely to raise rates twice more by 25 basis points. This would bring UK interest rates to 5.75% by the end of 2023. However, if these indicators remain elevated and labour markets do not loosen, MPC members have not ruled out a further tightening of monetary policy.

To conclude, following August’s MPC meeting, the BoE stressed that the future path of interest rates will be data dependent. Further rate increases are likely to be required in the coming months and, at the same time, committee members noted that interest rates will need to remain restrictive for a sufficiently long time to return inflation to the 2% target. This is not expected to be achieved before Q2 2025. In the meantime, the transmission of monetary policy tightening to the economy through the housing market and the exchange rate will continue to put pressure on borrowers and moderate import prices through an appreciation of the pound. These effects are expected to contribute to inflation falling to around 5% by the end of 2023. Whilst this represents significant improvement, it is still a long way from the BoE’s target.

1 The MPC expects that the unemployment rate will gradually rise to 4.8% in the next three years. A declining job vacancies-to-unemployment ratio indicates a loosening labour market.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.