- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Four days after its meeting on June 9, the ECB realised it must act to reassure markets. In this Macro Flash Note, GianLuigi Mandruzzato looks at what has been announced by the European Central Bank (ECB) and what remains unclear after the extraordinary meeting on June 15.

European financial assets - the stock market, bonds and the exchange rate - have been in almost free fall since the press conference following the ECB monetary policy meeting on June 9. The trigger was President Lagarde saying that the Governing Council (GC) had not discussed how the ECB will manage the widening of sovereign spreads vis-à-vis Germany as monetary policy is tightened.

Source: Refinitiv and EFGAM calculations. Data as at June 15 2022. Past performance is not an indication of future results.

Spreads widened strongly after ECB rate increases in 2008 and 2011, so the market reaction to the pre-announced start of the next ECB rate hiking cycle is not so surprising. On both prior occasions, the lack of a tool to deal with spread widening and the ECB's hesitation to create one exacerbated the negative effects on the eurozone economy. Furthermore, at the beginning of the pandemic in March 2020, Lagarde's indifference to widening sovereign spreads at that time encouraged them to move sharply higher, prompting the ECB to correct the message and launch the pandemic emergency purchase programme (PEPP) shortly after.

In 2020 it also took four days for the ECB to react after the initial communication blunder. Nevertheless, the latest ECB statement is extraordinarily vague, merely saying that:

- the ECB will “apply flexibility” in reinvesting maturing bonds bought under the PEPP, as already communicated after the June 9 meeting;

- the GC mandated “the relevant Eurosystem Committees together with the ECB services to accelerate the completion of the design of a new anti-fragmentation instrument for consideration by the Governing Council”.

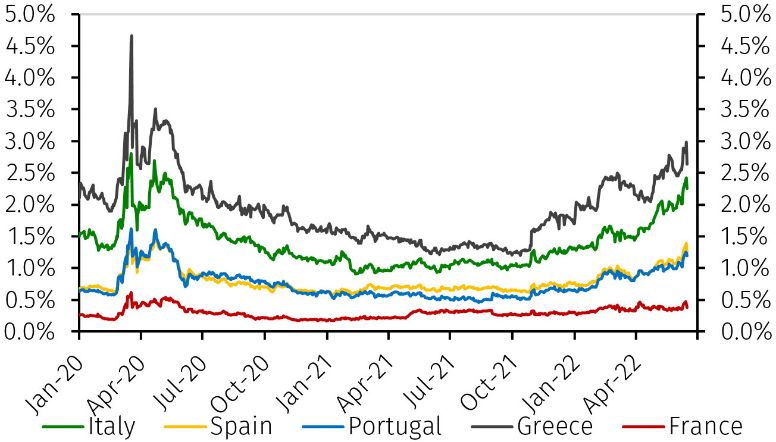

Markets reacted positively, extending the gains that followed the announcement of the extraordinary ECB meeting. The spread of Italian bond yields over German fell by about 30 basis points, although they remain about 1 full percentage point higher than at the beginning of the year. However, the lack of detail remains a concern and begs the question of whether the favourable market reaction is sustainable.

Markets reacted positively, extending the gains that followed the announcement of the extraordinary ECB meeting. The spread of Italian bond yields over German fell by about 30 basis points, although they remain about 1 full percentage point higher than at the beginning of the year. However, the lack of detail remains a concern and begs the question of whether the favourable market reaction is sustainable.

Questions resulting from the ECB's statement include:

- When does the Governing Council intend to define the new tool to combat financial fragmentation?

- What characteristics will the tool have?

- Will it, for example, be subject to constraints and conditionalities, per Draghi’s (Outright Monetary Transactions) OMT tool, or will the ECB Governing Council be responsible only for its activation?

- If the aim of the new tool is to prevent financial fragmentation and ensure the homogeneous transmission of monetary policy within the eurozone, at what level of spread would the GC consider using it?

- And what prevented the ECB from defining the new instrument before the end of bond purchases and the start of monetary policy normalisation?

In conclusion, despite the positive market reaction to the extraordinary ECB meeting on June 15, doubts remain about the substance of what was announced. The credibility of the ECB in preserving monetary union is again at stake and with it eurozone financial stability. It would be advisable for the Governing Council to make sure that details of the new anti-financial fragmentation instrument meet market expectations and to announce them as soon as possible rather than waiting until the next monetary policy meeting on July 21. Markets may not remain complacent that long.

1 The Outright Monetary Transaction facility was announced on August 2, 2012 a few days after Draghi’s famous “whatever it takes”. The facility allows the ECB to buy unlimited amounts of the bonds of a country that, at risk of losing market access, had committed to the “strict and effective conditionality attached to an appropriate European Financial Stability Facility/European Stability Mechanism (EFSF/ESM) programme”. Because the stigma attached to asking for support from the ESM prevented countries from turning to it, the OMT has never been used.