- Date:

- Author:

- Sam Jochim

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The US Federal Reserve appears to be nearing the end of its rate tightening cycle. In this Infocus report, Economist Sam Jochim analyses the implications for fixed income investors and assesses yield curve positioning.

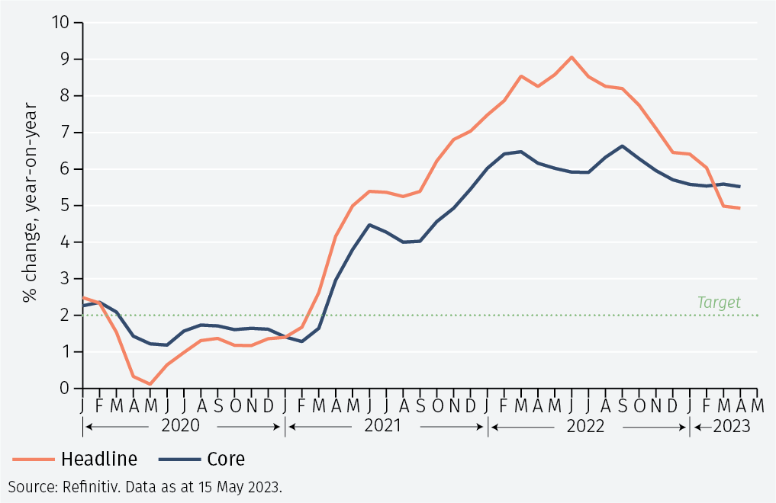

Having risen sharply from mid-2020 until mid-2022, inflation in the US appears to have peaked and is in a declining trend (see Figure 1). Despite the Fed’s dramatic tightening of monetary policy, involving 500 bps interest rate increases over 14 months, inflation remains above the Fed’s 2% target. While headline inflation has come down, core inflation, which excludes the volatile energy and food price components, has remained more persistently elevated. At 5.5%, it is far above the Fed’s 2% objective. Debate therefore continues regarding whether the Fed is likely to increase interest rates further.

Market expectations regarding interest rates have moved quickly. As recently as 8 March, markets expected the Fed funds rate to be 50 basis points above its current level after the FOMC’s June meeting (see Figure 2) with a good possibility of further hikes at subsequent meetings this year.

However, following recent bank failures, it became evident that one trade-off the Fed faces is between stabilising inflation and ensuring financial stability. As a consequence, rate expectations quickly shifted and rate cuts are now anticipated towards the end of the year.

This shift in expectations has been associated with a rally in fixed income markets. Treasury yields declined by around 40 basis points on average across the term structure from 8 March to 12 May.

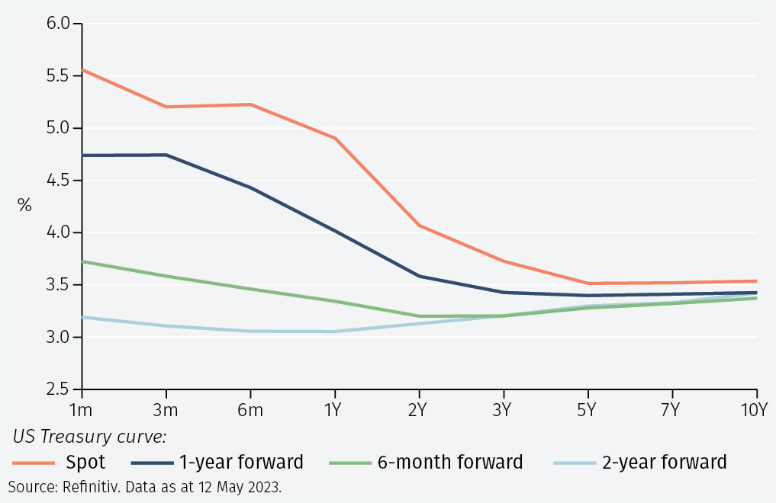

The possibility that the Fed funds rate has peaked has important implications for fixed income investors. Across the US government bond term structure, the yield is highest at the short-end of the curve as market participants are expecting short-term interest rates to fall in the months and quarters ahead (see Figure 3).

The inversion of the yield curve – the fact that short-term interest rates exceed longer term rates – is notable. This has historically been a strong predictor of recessions. Given that the cumulative impact of the large monetary tightening of the past year is yet to be fully felt, and credit conditions have tightened significantly, we believe it is likely the US economy will enter a mild recession later in 2023 or possibly early 2024.1

At the press conference following the latest FOMC meeting, Chairman Powell stated that it was more likely than not that the US would avoid a recession this year.2 If there is a recession and it turns out to be deeper than expected, for instance because credit conditions tighten further, the Fed may cut rates by more than markets currently anticipate. However, if the labour market remains tight and core inflation persistently elevated, and the Fed adopts a more hawkish tone, it is possible markets begin pricing in more rate hikes. Risks today are in both directions and each scenario would have important implications for fixed income markets.

For example, over a three-year time horizon, an investor could invest in a 3-year Treasury and hold it until maturity. Alternatively, they could invest in a 1-year Treasury to gain a higher yield and then reinvest at maturity into another Treasury of the same tenor and continue to do so until the end of the three-year period (roll-over strategy).

If the path of interest rates is in line with market expectations,the returns of both strategies would be similar (see Figure 4). However, if the Fed cuts interest rates more rapidly than markets currently expect, the return on the roll-over strategy will drop below the level currently implied by futures markets (as depicted in Scenario A in Figure 4). This would result in total returns over a 3-year period falling below what would be received had an investor locked in yields for the entire period. If the path of interest rates is above what markets currently expect (as depicted in Scenario B in Figure 4), total returns over a 3-year period would be higher for the roll-over strategy than for locking in yields for the entire period.

In summary, the Fed has increased interest rates sharply in the past year in response to high inflation. Concerns about financial stability have accompanied a decline in market expectations for the Fed funds rate, with the risk of recession in the US rising materially. However, if core inflation remains elevated, the Fed could adopt a more hawkish stance. Interest rate expectations can move quickly and there are important implications for fixed income investors who believe that the future path of interest rates will differ from what is currently priced by markets.

1 See EFGAM Infocus, ‘Bank lending standards and recessions’, https://tinyurl.com/4c3a7rwm

2 https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20230503.pdf

3 Calculations based on data as at close on 12 May 2023. Returns compounded over three years. The scenario analysis assumes that rates fall or rise relative to current market conditions in each year over the three-year period. For example, a decline of 50 basis points per annum in the 1-year Treasury yield over the next three-years produces a return of 10.1%.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.