- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the February edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The IMF recently released its latest World Economic Outlook Update. While the sharp economic downturn in 2020 was followed by strong growth in 2021, the IMF now forecasts lower global growth in 2022 than it did in its October projections. For the year as a whole, the IMF expects the global economy to expand by 4.4%, down from the 4.9% forecast last October. The revision to US growth, from 5.2% to 4.0%, is particularly large, due in part to the challenges the Biden administration has faced in getting the Build Back Better spending package passed. However, despite these downward revisions, the global and US economies are still projected to grow above trend.

The IMF also projects that inflation will stay high in the near term, averaging 3.9% in advanced economies and 5.9% in emerging market and developing economies in 2022. Relative to its October projections, that represents a 1.6% upward revision for the advanced economies and 1.0% for the emerging market and developing economies.

It is worth noting that these projections should be regarded as highly uncertain. For example, many commentators are concerned about further adverse Covid developments or a further increase in geopolitical tensions such as those associated with the conflict in Ukraine.

The combination of lower growth and higher inflation complicates central banks’ management of monetary policy and makes it more difficult for market participants to judge the outlook for interest rates. Lower growth points to a delay in the normalisation of monetary policy, but higher inflation indicates the need for tighter policy. Central banks’ policy choices will differ, depending on the relative importance of these two offsetting forces.

The way the Federal Reserve manages this process will be critical for financial markets. The FOMC suggested in December that it might raise the interest rate three times in 2022, but the change in the economic outlook points to both upside and downside risks. In January the FOMC said that it anticipates that it will be appropriate to raise rates soon, which points to a high probability of a rate increase in March. Further uncertainty pertains to the outlook for the Fed’s balance sheet. While the Fed indicated that bond buying will stop in March, the question arises when and how fast it will seek to reduce the size of its balance sheet. Although in January the FOMC indicated that it intends to do so significantly but in a predictable manner, it seems likely that this process will put upward pressure on long bond yields and lead to tighter monetary conditions.

These concerns have been front and centre over the last few weeks during which equity markets have come under pressure. Yet, the overall favourable growth outlook underpins corporate profitability, something that should support equity prices and justifying a moderate overweight in risky assets within a balanced portfolio. In the context of rising bond yields, value stocks look attractive as do those markets for which monetary policy will be more supportive, including Europe and China. Fixed income markets remain under pressure, but convertible bonds have cheapened significantly in the last few months. Finally, to hedge the portfolio against market volatility, some exposure to gold, the Swiss franc and the Japanese yen remains advisable in our opinion.

Global Asset Allocation: Summary

Equities

- We have been warming up to European equities due to a more favourable rate environment and attractive valuations. However, given that this was the worst January in years for the S&P 500 index, it is not appropriate to upgrade European equities at the expense of US equities at this moment.

- We instead intend to wait for a bounce back in US stocks and use that as an opportunity to tactically downgrade US equities to neutral.

- Positioning in US equities should be split between large cap value stocks, reflecting the change in the economic cycle, and small cap growth, to benefit from a mean reversion trade. This could be implemented over the quarter.

- We maintain our tactical UK overweight given economic strength and expectations of strong GDP growth in 2022, the fastest among G7 economies.

- Policy in Japan, Europe and Latin America could provide a tailwind to their respective markets.

Fixed Income

- Fixed income markets have experienced disappointing performance at the start of 2022. Yields have slowly picked up over the month, as markets have priced in more rate hikes from the Federal Reserve. Sovereign bonds continue to be strategically underweight.

- Spreads in investment grade credit tightened at the end of 2021 back to pre-pandemic levels and remain exposed to changes in interest rates. So far, credit spreads have not reflected the pick-up in government yields so we hold a neutral position.

- We are starting to warm up to emerging market bonds, both in hard and local currencies, for 2022 given higher rates and weaker currencies.

- We stay overweight in convertible bonds despite the weak start to the year for this asset class, hurt by the rotation away from tech names.

Alternative Investments

- Infrastructure is one of the more favoured areas in the alternatives space and should also offer some protection for investors concerned about rising inflation.

- While volatility has increased, the M&A market has repriced making the opportunity set more attractive. Competitive bidding tensions, particularly in rapidly consolidating industries, make this a fluid strategy in 2022. We also see opportunities in spin-offs, divestments, and IPOs,which should be good for special situations and activist managers. The uncorrelated profile of the strategy makes it a compelling diversifier and an alternate alpha stream in portfolios in our view.

Currencies

- After a strong 2021, the US dollar has started the year flat against a basket of currencies. Over a longer time frame, the curve has flattened which should continue to re-enforce dollar strength.

- The value of the euro against the US dollar weakened in the first month of 2022 on account of higher inflation in the US and an associated shift in relative rate expectations. We have adjusted our target, consistent with our expectation that the ECB will remain dovish for longer. Market positioning remains neutral, consistent with our view.

- We remain cautiously underweight the Swiss franc, anticipating that current conditions could warrant further weakening of the currency versus the dollar.

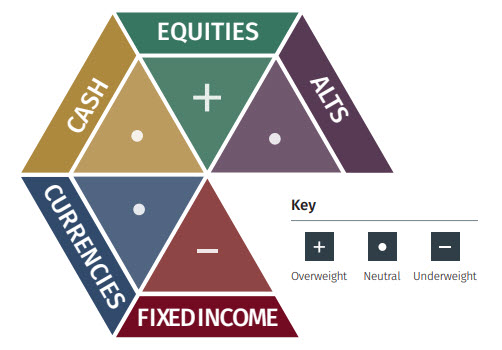

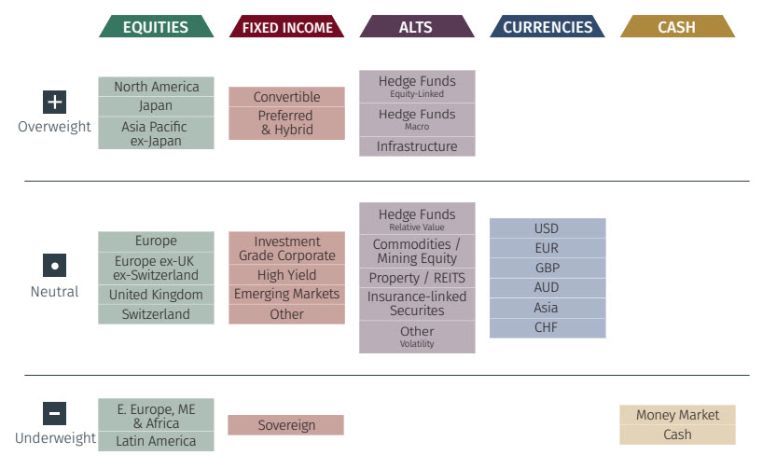

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breakdown

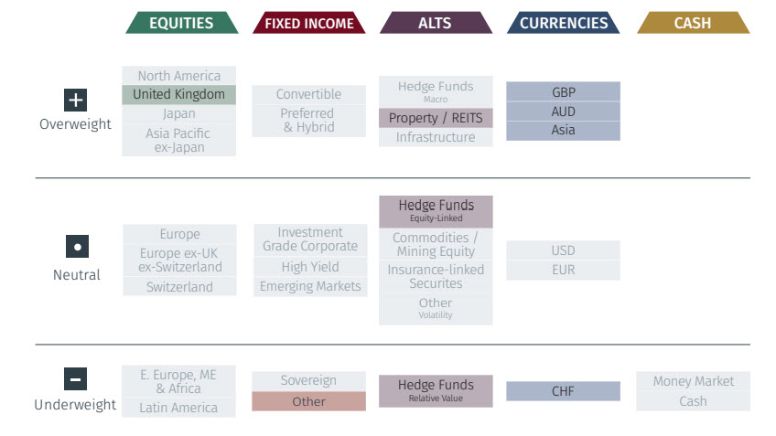

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

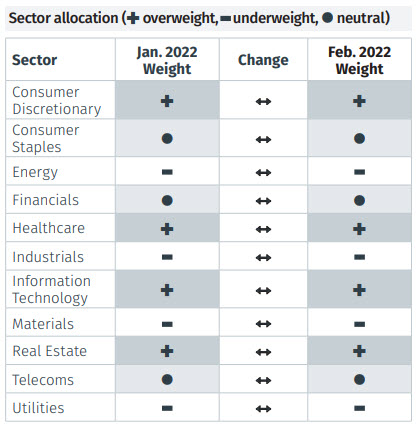

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.