- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

On Monday 5 September, Liz Truss won the Conservative Party leadership race and has now become the UK Prime Minister (PM). In this Macro Flash Note, Joaquin Thul discusses the challenges ahead for Truss and the main items in her domestic and foreign policy agenda.

After almost two months of campaigning, Liz Truss became UK Prime Minister receiving 57% of the votes from Conservative Party members and beating former chancellor Rishi Sunak for the top job. The difference in votes between candidates was smaller than initially anticipated by political commentators and represents the lowest vote share for a successful candidate since the current system to elect Conservative Party leaders was introduced in 2001.1

The campaign was almost entirely focused on the UK’s rising cost of living and potential solutions to the country’s decelerating economy. Truss will now have a maximum term of over two years before the next general election which must be held before January 2025. In her first speech outside 10 Downing Street, Truss highlighted three key priorities for her government:

1. Promote growth through tax cuts and economic reforms.

2. Tackle the energy crisis in the country driven by Russia’s invasion of Ukraine.

3. Support the National Health Service, with over 6 million people still waiting for treatments.

Regardless of the policies implemented to achieve these objectives, she could benefit from the very low expectations set for her government given the difficult economic environment she is inheriting. Opinion polls give the Conservatives only 32% of voting intentions, 10 percentage points behind Labour.2 Additionally, the Tories’ 75 seat majority in the House of Commons should allow Truss meaningful political flexibility to pass legislation.

Challenging domestic scenario

Truss has started her term as PM with the difficult task of dealing with a worsening domestic economic outlook, marked by the rising cost of living, a deterioration in public finances and difficult relations with workers’ unions. According to forecasts from the Bank of England, UK GDP is expected to decline in Q4 2022 and enter a recession from the first quarter of 2023. GDP is expected to contract between 1.5% and 2% in 2023. At the same time, inflation is expected to peak at 13% in Q4-2022 before easing back to single-digits in Q3 2023, assuming global energy prices stabilise and tradable goods prices decline.

Although there have been no official policy announcements yet, Truss is expected to:

- Reverse the rise in National Insurance Contributions of 1.25%, which was introduced by Sunak in April of this year. According to the Institute of Fiscal Studies (IFS), this would have cost £13 billion per year.

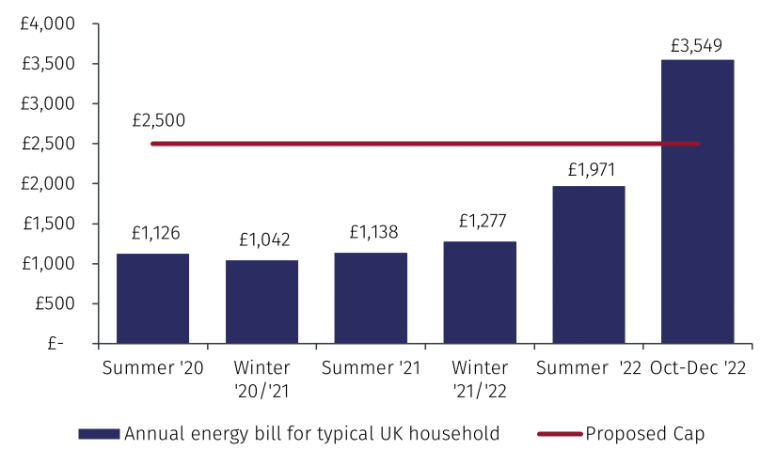

- Set a cap on household energy bills at about £2,500 for the next two years, helping to protect consumers from surging gas and electricity prices, see Figure 1.

- Cancel the planned increase in corporation tax from 19% to 25%, scheduled for next year, and oppose any further windfall taxes on energy firms, in a clear signal to attract investment to the UK.

- Review taxation of families and the use of tax allowances to tackle problems with affordability of childcare.

Source: BBC and EFGAM. Data as of 6 September 2022.

With public debt rising above £2 trillion, the IFS estimates that some of Truss’s policies could cost more than £30 billion per year and warned about the negative impact on public finances of some of these promised tax cuts. Although the Office for Budget Responsibility (OBR) estimated in March the government would have headroom of approximately £30 billion against the existing fiscal rules, the outlook for the UK economy has worsened since then. Therefore, the fiscal space is likely smaller and some of the additional spending would need to be financed by debt issuance.

The new PM will also face the difficult task of negotiating with trade unions. Last month she revealed plans to raise the minimum threshold for voting in favour of strike action from 40% to 50%, restricting the ability of trade unions to call strikes. She also plans to propose a change in legislation that guarantees a minimum service during strikes to reduce disruptions.

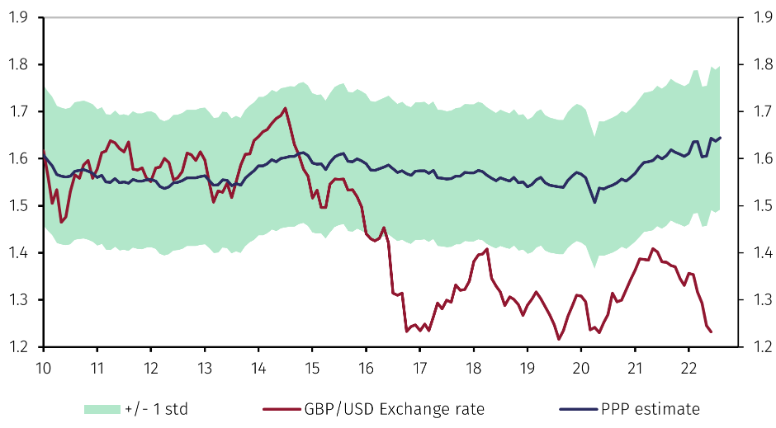

Despite being critical of the Bank of England’s (BoE) strategy to tackle inflation over the last year, she has explicitly supported the independence of the central bank. However, she has spoken about the need to reassess its mandate, which was set in 1997. The deterioration of the outlook for the UK economy and the recent strength of the US dollar has been reflected in the price of the pound which recently reached $1.15, the lowest level since 1985. We expect the BoE to follow through on its announcements to tighten monetary policy more aggressively in the coming months which will support sterling, particularly if US interest rates peak earlier than other central banks. Furthermore, the current estimated undervaluation of the pound against the dollar could also shrink as US Producer Price Index (PPI) falls on lower energy prices and UK PPI rises further in the coming months, see Figure 2.

Source: Refinitiv and EFGAM. Data as of 6 September 2022.

Busy foreign agenda

The implementation of post-Brexit trading arrangements with Northern Ireland has resulted in a deterioration of the relationship between the UK and the EU. Truss expressed her intention to push forward unilateral legislation to override the Northern Ireland protocol, a key part of the Brexit deal. If enacted, it could be perceived as a provocative action from the UK and risk increasing tensions with EU leaders.

Despite voting in favour of the UK remaining in the EU in the 2016 referendum, she is committed to continuing Johnson’s Brexit policies and overhauling the UK’s immigration and trade rules. Before her appointment as PM, she confronted French President Macron over the migrant crisis which will be another important item on her agenda for the next two years.

The incoming PM has maintained strong support for Ukraine, pledging to continue providing weapons and maintaining sanctions on Russia. Moreover, Truss has pledged to increase UK defence spending to 3% of GDP by 2030.

Finally, during her term as Foreign Secretary Truss was particularly hawkish on China. She stated her intention to declare China a “threat” to national security, which could lead to a review of investments involving Chinese companies in the UK. However, it remains unclear what her priorities will be on this front.

Conclusion

The appointment of Liz Truss as PM did not come as a surprise to markets. She faces a very difficult economic scenario marked by the rise in inflation, the reduction in real wages, rising energy prices, a geopolitical conflict with Russia and strained relations with the EU. Although expectations are very low regarding how much Truss will be able to achieve, her government will be a beneficiary of the Party’s large majority in Parliament and the fact they will not face an election for over two years.

1 In 2001 Iain Duncan Smith obtained 61% of membership votes, David Cameron got 68% in 2005 and Boris Johnson got 66% in 2019. Theresa May did not face a membership vote in 2016 as her opponent, Andrea Leadsom, pulled out after the first two rounds.

2 https://www.politico.eu/europe-poll-of-polls/united-kingdom/

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.