- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The European price of natural gas exceeded EUR 300 MW/h driven by concern about supplies from Russia ahead of the winter. In this Macro Flash Note, GianLuigi Mandruzzato looks at the fundamentals of the European natural gas market to assess current prices.

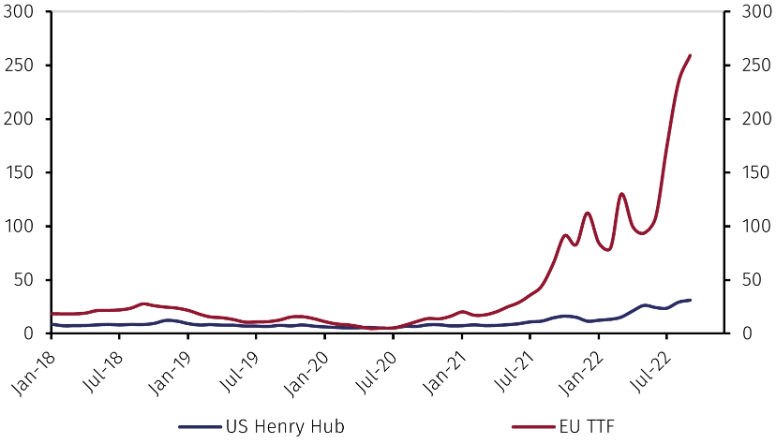

On August 26, the European natural gas price hit a new intraday record at EUR 340 MW/h, before falling at the time of writing this note to EUR 230 MW/h.1 The price has increased by about 200% since mid-June and is about six times higher than its 2021 average. Furthermore, the European price of natural gas is almost 8 times more expensive than the US Henry Hub benchmark.

Source: Refinitiv and EFGAM calculations. Monthly average data as at 30.08.2022.

As natural gas is used to produce electricity, for home heating, and as an input in many industrial processes, including chemical and fertiliser production, its high price is one of the main reasons for the high inflation in Europe that clouds the economic outlook.

Many commentators explain the surge in European natural gas prices in recent months with the collapse of supplies from Russia, with reduced electricity production by French nuclear power plants and the hydroelectric sector due to the drought in Europe. The spectre of gas shortages next winter that could lead to rationing would have pushed sector operators to purchase at any cost at a time of increased demand for gas for electricity generation.

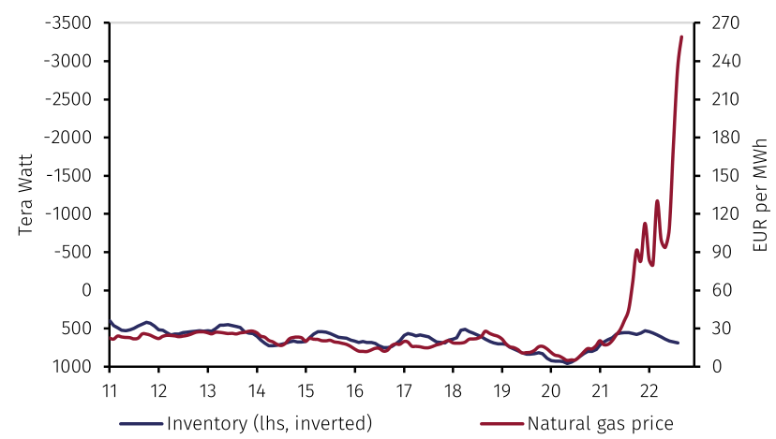

The evidence casts doubt on this interpretation. Despite the panic raised by the 80% contraction of Russian natural gas exports to Europe, EU storage of gas has risen to over 80% of capacity, up from less than 67% at this time of the year in 2021. It is notable that it has risen steadily in the last two months, suggesting that there was sufficient electricity generation capacity available elsewhere in the system to meet demand.

Source: AGSIE, Refinitiv and EFGAM calculations. Monthly average data as at 30.08.2022.

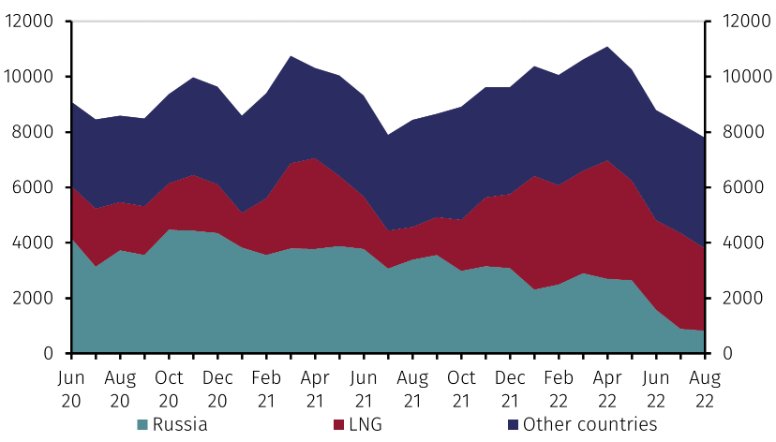

In fact, European countries are much less dependent on Russia for natural gas supplies than earlier. Since the invasion of Ukraine, European natural gas imports from Russia have fallen and now represent only about 10% of EU total imports, down from more than 40% in 2020.

Source: AGSIE, Refinitiv and EFGAM calculations. Monthly average data as at 30.08.2022.

In this period, liquified natural gas (LNG), mainly imported from the US and the Middle East, has become more prominent along with pipeline supplies from Norway and North Africa. Supply capacity from Norway will rise further when the new Baltic Pipe comes online in October, delivering gas to Denmark and Poland. In addition, in early 2023 new LNG terminals will be operational, further reducing European dependence on Russian supplies.

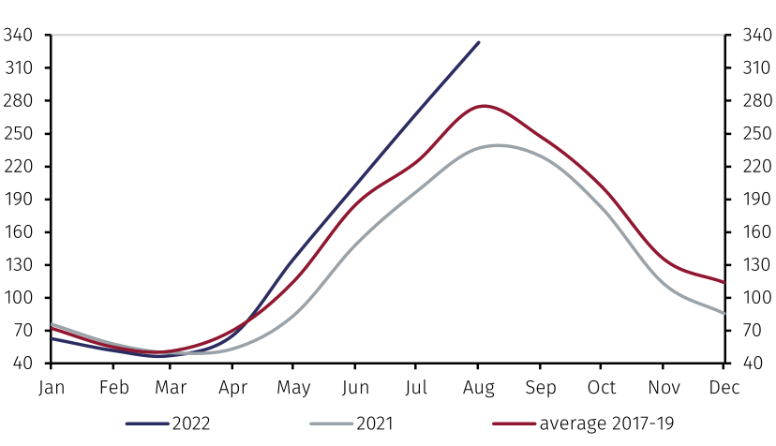

Reduced demand, also because of high prices, contributed to the improved availability of natural gas. In the first seven months of 2022, consumption of natural gas in Europe fell by 15.4% from a year before, and more measures to limit its demand for non-industrial purposes, including reducing by 1 degree Celsius the heating of homes and offices, are under discussion among European leaders. As a result, at the end of August, the coverage of days of demand guaranteed by natural gas storage is much higher than last year and the 2017-2020 average.

Source: AGSIE, Refinitiv and EFGAM calculations. Monthly average data as at 30.08.2022.

In conclusion, the increase in natural gas prices in Europe reflects more the fear of a possible shortage during the coming winter than an actual scarcity of gas. The diversification of suppliers has already significantly reduced the European dependence on Russia and allowed abundant stocks to be accumulated well ahead of the winter. Even in the event of a complete stop to Russian exports to Europe, the impact should not be as devastating as it would have been only 12 months ago.

Furthermore, new supply from Norway and new LNG terminals will soon be available and the reduction of natural gas and electricity demand because of surging prices has increased the resilience of the European economy to the unpredictability of Russian supplies.

This should moderate European natural gas prices to more sustainable levels, although markets will likely wait until the beginning of winter to assess how meaningful the risk of an actual shortage is. If the energy bills for European households and businesses will stay high in the short term, there are reasons to believe that they will fall in and beyond 2023.

1 The European benchmark is the one-month delivery futures contract to the Title Transfer Facility (TTF) in the Netherlands.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.