- Date:

- Author:

- Sam Jochim and GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Stronger than expected CPI inflation in September firmed expectations that the Federal Reserve will raise rates by 0.75% on 2 November. However, subtle changes are taking place both in the underlying price dynamics and in the Fed’s communications. In this Macro Flash Note, Sam Jochim and GianLuigi Mandruzzato look at the implications for future Fed policy.

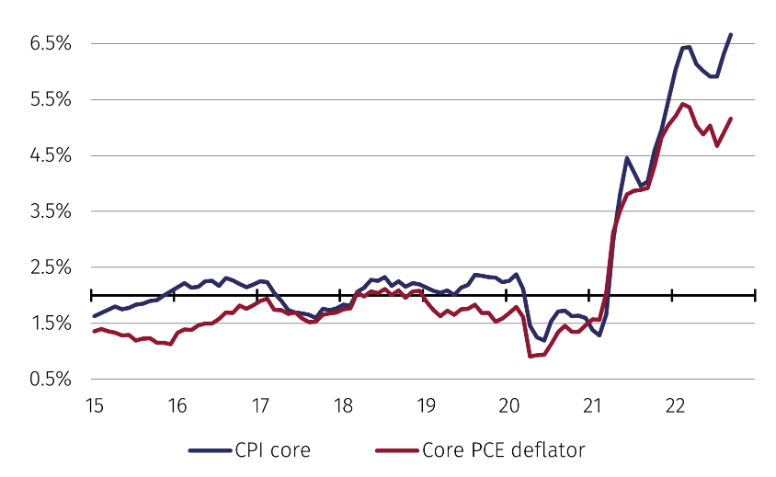

September CPI inflation was once again stronger than expected. Both headline and core CPI inflation were 0.1% higher than consensus expectations. However, the Fed’s preferred measure of inflation is PCE inflation, which will not be released until 28 October. Using CPI data to estimate PCE inflation suggests a decline in headline PCE to 6.1% year-on-year (yoy) and an increase in core PCE to 5.1% yoy. While broadly in line with consensus, these estimates leave PCE inflation much above the Fed’s 2% objective (see Chart 1). Unsurprisingly, the CPI release cemented market expectations that the Federal Reserve will again increase the fed funds rate by 0.75% when it meets on 2 November.

Source: Bureau of Labor Statistics, Refinitiv and EFGAM calculations.

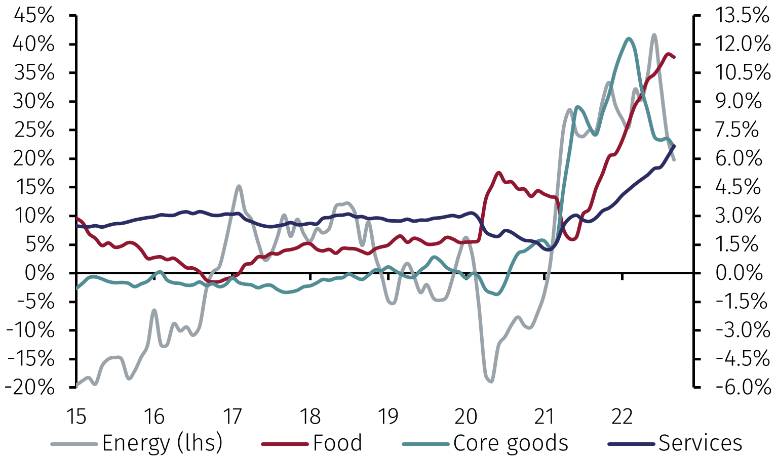

However, inflationary pressures are easing. This is best seen by looking at the four main components of the CPI basket: energy, food, core goods, and services. Chart 2 shows that the rate of increase of all of these components except services is moderating. The decline is most evident in energy and core goods prices, which reflect the normalisation of global supply chains. The rate of change of food prices has also moderated and lower fertiliser and gas and oil prices point to further falls ahead.

Source: Refinitiv and EFGAM calculations.

Services prices, instead, continued to accelerate, pushed higher by housing and health care costs. The good news is that the housing and rental markets have already lost momentum, reflecting the tightening of monetary policy since March. It is only a matter of time before this is reflected in CPI inflation.1

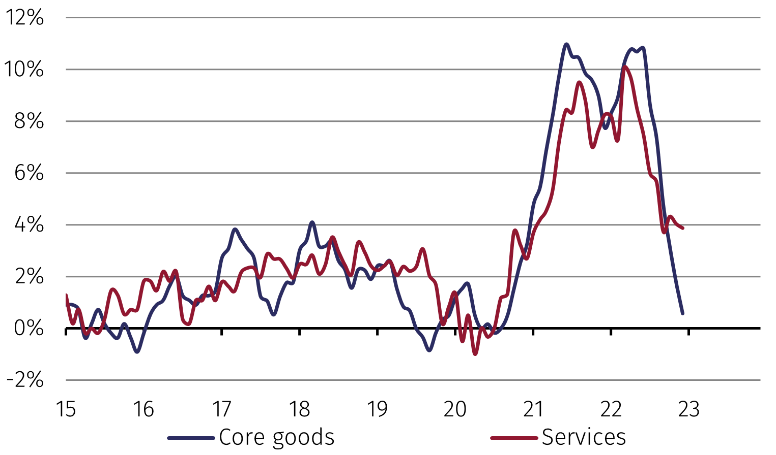

Furthermore, inflationary pressures are abating fast at factory gates (see Chart 3). Although annual increases of final demand PPI for both core goods and services remain historically high their six-month annualised changes have fallen sharply since the spring, returning within or close to the range that prevailed before the pandemic.

Source: Refinitiv and EFGAM calculations.

It is notable that sentiment at the Fed has shifted subtly, as suggested by a recent Wall Street Journal article. This is evident when comparing statements made between July and September with those made in October (see Appendix).

Vice Chair Lael Brainard has recently noted that risks to the financial system will rise as policy becomes more restrictive and that Fed policy needs to be judged together with the monetary tightening elsewhere in the world economy.

Nonetheless, future Fed policy will remain heavily dependent on incoming data. The fact that a more balanced debate about policy may have started within the FOMC, having previously been focused entirely on inflation, will soon become more evident. If we were to see a couple of months of weaker economic data and if inflation were to continue to roll over as more and more evidence suggests, it would be natural to expect the Fed to adjust its tone and policy to the new circumstances.

Appendix – Quotes taken from recent Fed speeches

Mary Daly, Federal Reserve Bank of San Francisco

29 September - “Navigating the economy toward a more sustainable path necessitates higher interest rates and a downshift in the pace of economic activity and the labor market. […] Resolute to our goals, the Fed has raised the benchmark interest rate rapidly this year, and projects additional increases will be needed. These are necessary and appropriate adjustments, taken to put the economy back on a solid footing.”

21 October - “We are starting to see slowing take hold, but more tightening is needed. However, we are now in a stage of policy where we need to be thoughtful and need to do everything in our power not to overtighten. We have to take account of synchronized global central bank tightening.”

Lael Brainard, Vice Chair

7 September - “We are in this for as long as it takes to get inflation down. So far, we have expeditiously raised the policy rate to the peak of the previous cycle, and the policy rate will need to rise further.”

10 October - “The moderation in demand due to monetary policy tightening is only partly realized so far. […] Against the backdrop of slower output growth, we are seeing some tentative signs of rebalancing in the labor market. […] The combined effect of concurrent global tightening is larger than the sum of its parts. […] In this environment, a sharp decrease in risk sentiment or other risk event that may be difficult to anticipate could be amplified, especially given fragile liquidity in core financial markets. […] In light of elevated global economic and financial uncertainty, moving forward deliberately and in a data-dependent manner will enable us to learn how economic activity, employment, and inflation are adjusting to cumulative tightening in order to inform our assessments about the path of the policy rate.”

John Williams, Federal Reserve Bank of New York

8 July - “Inflation is far too high, and price stability is absolutely essential for a strong economy. We have the tools to get the job done and are one hundred percent committed to achieving our goals.” 3 October - “Tighter monetary policy has begun to cool demand and reduce inflationary pressures, but our job is not yet done. It will take time, but I am fully confident we will return to a sustained period of price stability.”

Christopher Waller, Federal Reserve Governor

9 September - “All told, the FOMC has taken unprecedented and decisive policy actions this year to quickly increase the policy rate in response to high inflation. But where we stand now is not good enough. Though the labour market is strong, inflation is too elevated. So I support another significant hike in two weeks. After that, the tightening path will continue until we see clear and convincing evidence that inflation is moving meaningfully and persistently down to our 2 percent target.”

6 October - “So, as of today, I believe the stance of monetary policy is slightly restrictive, and we are starting to see some adjustment to excess demand in interest-sensitive sectors like housing. But more needs to be done to bring inflation down meaningfully and persistently. I anticipate additional rate hikes into early next year, and I will be watching the data carefully to decide the appropriate pace of tightening as we continue to move into more restrictive territory.”

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.