- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The summer rally that began in mid-June and ended in mid-August provided welcome relief for investors. However, since mid-August markets have once again turned downwards, with concerns focusing on the traditional party-poopers of slowing growth, rising inflation and tighter monetary policy. This edition of Infocus looks both back and forth for expectations as we head towards the end of 2022.

The summer rally that began in mid-June and ended in mid- August provided welcome relief for investors. However, since mid-August markets have once again turned downwards, with concerns focusing on the traditional party-poopers of slowing growth, rising inflation and tighter monetary policy.

The past two weeks have been particularly troubling, with the MSCI World equity index down over 10% and the MSCI Emerging Market equity index down 9% (unhedged in US dollars). There have been few places to hide with the FTSE World Government Bond index having declined by nearly 5% (unhedged in US dollars) over this period. From a recent intraday low of 2.5% in early August, the ten-year Treasury yield has backed up nearly 1.5% at the time of writing. The US dollar has been strong throughout.

Many analysts have been humbled by the highly unusual events of 2022 yet it is also important to remove emotion from the analysis in thinking about the prospects for the remainder of this year and the start of next year. We consider three factors as central to the prognosis:

- The prospects for interest rates and inflation

- The outlook for growth and corporate profitability

- Positioning and sentiment

Policy rate

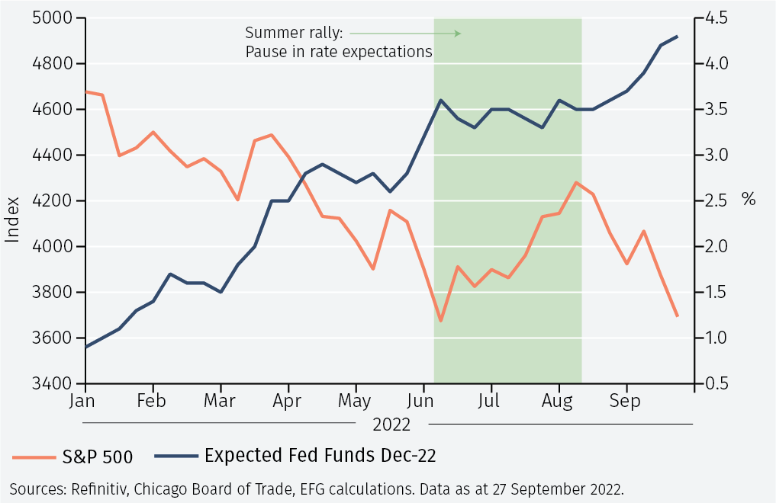

As Figure 1 shows, market moves this year have been closely associated with shifting rate expectations. The downward move in the first six months of the year occurred as market participants sequentially revised up their expectations for where the Fed funds rate would finish the year. The summer rally coincided with a pause in that upward trajectory while the recent move lower in equities and higher bond yields has corresponded to another leg up in monetary policy expectations.

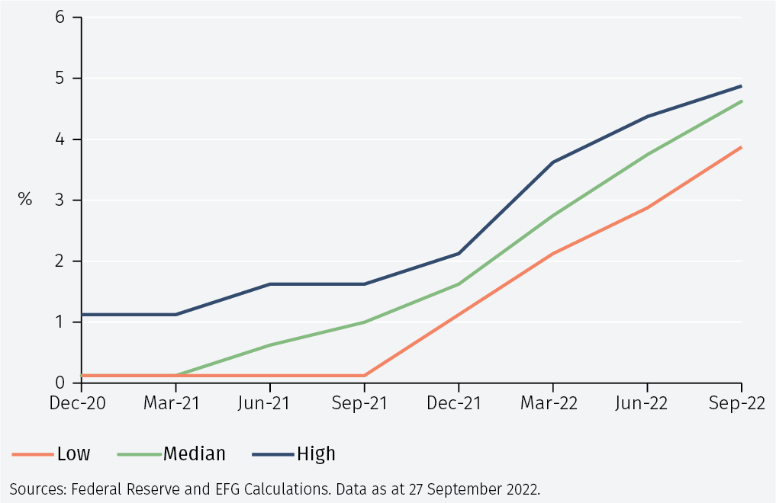

A further challenge for markets has been an unusual degree of uncertainty regarding rate expectations. This has been reflected in the behaviour of fixed income markets as seen in the steady move higher this year in the MOVE index, the fixed income equivalent of the better-known VIX index. Not only have rate expectations been moving higher but there has been ongoing confusion about where and when rates will peak and for how long they will stay there. This is evident in the Fed’s own Summary of Economic Projections (SEP), as shown in Figure 2.

It is therefore our view that the outlook for markets depends critically on the outlook for rate expectations. As the old saying goes: “Don’t fight the Fed”. In turn this is critically connected to the outlook for inflation; policy makers around the world have made it clear that they are prioritising the fight against inflation over the need to support the economy. Once inflation is perceived as being under control, policy makers will turn their attention to supporting the economy.

For many years, policymakers did not have to worry about inflation, which was persistently low almost regardless of economic conditions, and instead focused single-mindedly on supporting activity when necessary. But that has all changed. With labour markets around the world so far remarkably unscathed from events this year, policymakers are concentrating instead on containing price pressures.

The Inflation Outlook

Inflation this year has surprised most analysts including ourselves, having peaked at a higher level and been more persistent than anticipated. Taking stock of these unexpected developments, the more important task today is to think about the outlook for inflation in the months ahead. This depends on many factors, including:

- The base effect i.e., the mathematics of inflation that is already in the system

- Energy prices

- Food prices

- House prices and rents

- Supply chain pressures

- Wage dynamics

It is helpful to note that:

- The cumulative base effect in Q4 2022 amounts to a headwind of around 2.3 percentage points on the year-on-year change in US CPI i.e., if prices don’t change at all over Q4, the year-on-year change in the US CPI will decline by 2.3 percentage points.

- Energy prices have rolled over significantly with the price of a barrel of WTI oil down over one third from the high earlier this year.

- The year-on-year percentage change in the UN Food and Agriculture World Food Price index is down from a peak of 34.0% in March of this year to 7.9% as at end August.

- The US housing market has weakened significantly. The year-on-year percentage change in the Zillow US home rental index is down from 17.2% in February to 12.5% in August.

- The Federal Reserve Bank of New York Global Supply Chain Pressure index is down from a high of 4.31 at end December 2021 to 1.47 at end August 2021, the lowest since January 2021 and in a declining trend.

- Against these forces putting downward pressure on inflation, it is sensible to note that labour markets remain tight and wage inflation has picked up.

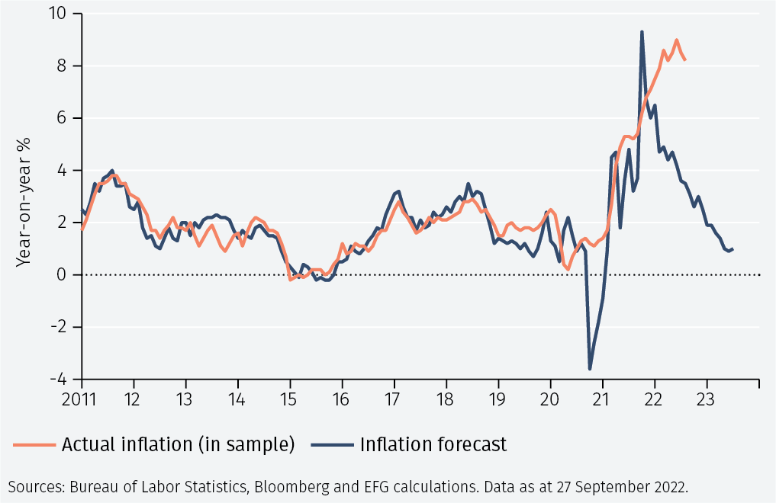

It is hard to encapsulate all this information into a single point forecast, but we have found it instructive historically to use an econometric model that is shown in Figure 3.

It is interesting to note that the model anticipated well the increase in inflation earlier this year although it has been premature in forecasting a decline. According to the model, US CPI inflation is expected to end 2022 at 2.6% and to continue to decline sharply into 2023. However, the model was six to eight months early in anticipating the inflation peak so perhaps the forecast for year end is six to eight months ahead of time. Adjusting the model accordingly would suggest a year end inflation rate of around 4.5%. This is low relative to market expectations and it may well prove too optimistic but it nonetheless indicates the significant downward forces on US inflation that are already present in the economy.

Despite the stronger-than-expected US CPI reading for August, there is growing evidence that inflation in the US has peaked. The high of 9.1% year-on-year in July was followed by readings of 8.5% and 8.3% in July and August respectively. The trend is therefore lower although the level is still too high for comfort. However, if the Fed were to observe larger-than- forecast declines over the next couple of months this may well be sufficient for adjustment to their guidance and a favourable shift in market rate expectations. For reference,the November US CPI will be released on 13 December. If, at the same time, there is evidence of a weakening of labour markets and declining activity, the shift in rate sentiment could be quite quick and profound. This conveniently leads onto the second factor that is important in terms of the big picture outlook over coming months: economic growth.

The growth outlook

It is undeniable that the global growth situation has deteriorated sharply this year and continues to worsen. The lagged benefit of Covid stimulus has waned whilst events in Ukraine have resulted in higher commodity prices that act like a tax on consumption and caused a huge increase in geopolitical uncertainty. Growth estimates have been revised lower as the year has progressed: in September last year the OECD forecast world growth of 4.5% in 2022 but by September 2022 that forecast had dropped to 3.0%. The European economy has been particularly hard hit given its dependence on Russian energy and its geographical proximity to Ukraine.

However, the US is much less vulnerable. Not only is the US economy physically more distant from (and therefore less economically integrated with) Ukraine but the US is a net energy exporter. Overall, the US is a relatively closed economy with trade (exports plus imports) accounting for around 25% of GDP compared to about 90% for the European Union.1 Nonetheless the US economy is not immune from global events and will increasingly feel the impact of the monetary tightening that has so far been enacted.

The properties of the US yield curve as a forecaster of recessions are well known. In short, when the 3-month Treasury yield trades above the 10-year Treasury yield that signals a US recession in around 12 months’ time. According to current expectations about the path of Fed tightening, yield curve inversion might happen over the next few months. If historical relationships hold, that in turn would suggest a US recession in the second half of next year. However, it is important to remember that the relationship provides only a rough guide to the timing. Previous episodes of US yield curve inversion have preceded recession by as little as five months (as was the case in 1973). If that were the case on this occasion, then the US economy might experience recession as early as the second quarter of 2023.

Regardless, given the underlying strength in the US labour market, low real interest rates despite higher nominal rates, some insulation to events in the rest of the world, US energy self-sufficiency, a healthy financial system and flexibility in US monetary policy, we would not anticipate a deep recession.

A useful analogy might be the 2001 recession which was very mild in economic terms even if the market fall out was much more painful.

In terms of the potential impact on corporate profits there are two major and conflicting forces. Higher inflation feeds through to higher revenues which is typically good for earnings, although the impact on profitability for individual companies will depend on the mix between input price inflation and output price inflation. Against this we must balance the slowdown in activity that acts as a brake on corporate profits.

Again, an econometric model is instructive. Using as inputs current forecasts for US CPI inflation and GDP growth suggests that corporate profit growth will slow a bit as the year progresses but that there is a risk of a more meaningful slowdown next year, possibly with EPS growth declining to low single digits. Such forecasts are recursive to some extent: if inflation and GDP growth slow as much as anticipated then the path of Fed policy will change and EPS estimates will be revised higher. However, the situation would have to deteriorate before it gets better.

Positioning and sentiment

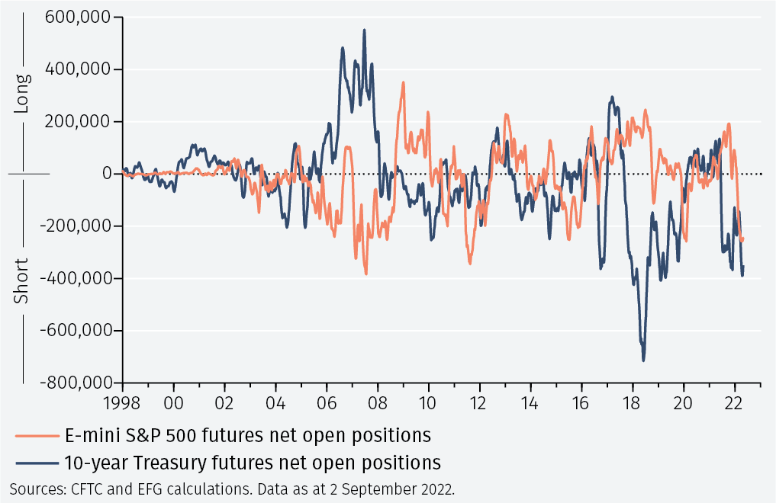

There have been few periods that have seen investor sentiment more depressed. For example, the Bank of America Fund Manager Survey shows cash positions close to their highest since 2001 while that same survey shows the most bearish global equity positioning since records began. This can also be seen in futures positioning, as shown in Figure 4. Furthermore, not only is positioning very negative against equities, but it is also very negative against bonds.

From a contrarian perspective this is a good thing as it is hard for investors to get more pessimistic. For example, thelast time futures markets were positioned this negatively, the S&P500 returned 70% over the following 12 months. However, by itself negative positioning is not sufficient to guarantee good returns. During the Global Financial Crisis investors stayed cautiously positioned for a prolonged period over which equity market returns were mostly negative. What is required is a catalyst to convince investors to cover their shorts. Per the above discussion, it is our view that the most likely catalyst is a shift in US rate expectations. Such a move would also likely be accompanied by a sell off in the US dollar given that the market is also positioned unusually long against the greenback.

Market implications

Putting all the above together suggests the following outlook:

i. Against a background of ongoing uncertainty regarding growth, inflation, earnings, rates and geopolitics, markets are expected to remain difficult over the next couple of months. This also fits with traditional seasonal patterns in which September and October are typically more challenging months for equities.

ii. Given the extent to which investors and policy makers were wrongfooted earlier this year, greater-than-normal confidence will be required before there is comfort that inflation is truly rolling over. In turn this would be a precursor to softening rate expectations. That might happen towards late November or early December, perhaps coinciding with the US CPI release on 13 December.

iii. With equity markets around the world down sharply this year and bond yields having risen significantly, the three-year view on traditional asset returns is healthy. Whilst timing is always difficult, for investors willing to accept some short-term volatility and especially those who are currently underinvested, now is a good time to start using market conditions to increase exposure.

iv. Similarly, bond yields are much more attractive now than they were just a few months ago. If clients are nervous about equities then investment grade debt offers an alternative. If the economic situation holds up, then clients will receive an attractive yield. If the economic situation deteriorates one would expect yields to decline and clients may benefit from a capital gain as well as the yield, dependent on what happens to spreads.

v. On a top-down macro basis, we remain cautious on European equities given ongoing vulnerabilities associated with the war in Ukraine. However, we note that this is a consensus view. We like emerging market equities due to the greater policy flexibility and much lower debt-to-GDP ratios than most developed nations. It is notable that Japan - which is clearly not an emerging market but which is nonetheless influential in Asia – and China are two countries that are continuing to apply stimulus even as other countries are tightening policy.

vi. Slowing growth is normally associated with a rise in high yield defaults, which have risen a bit but remain low in an historical context. A spike in the default rate and accompanying increase in high yield spreads has historically been a good signal that markets are at or near a bottom This also suggests that the next few months will remain uncertain for the riskiest of assets until the peak in the default cycle is within sight.

vii. Our current expectation is that the US will experience a mild recession next year, possibly as early as Q2. Markets would typically anticipate recession 6 to 12 months ahead and that may partly help explain current investor malaise. Similarly, markets also anticipate recovery, the timing of which may also be consistent with a year end rally, especially if that coincides with greater clarity regarding the outlook for rates.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.