- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Many commentators are concerned about the centre-right victory in the Italian elections. Investors have subsequently sold Italian government bonds, resulting in an increase in the yield spread over Germany. In this edition of Infocus, GianLuigi Mandruzzato looks at the challenges facing the new government in establishing its credibility.

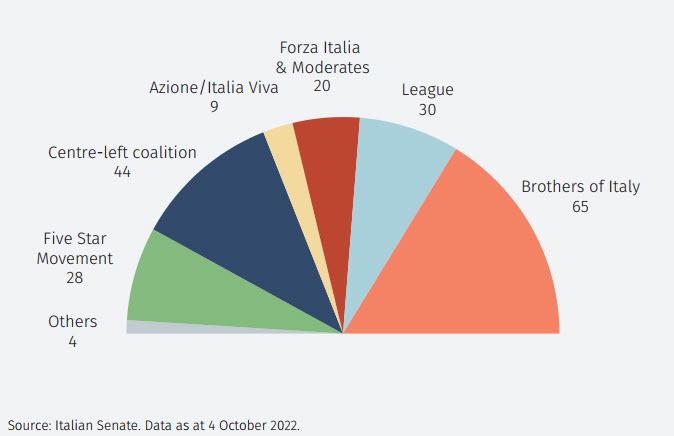

The centre-right coalition won the Italian general election on 25 September by a large margin. Right wing Fratelli d’Italia (FdI, or Brothers of Italy) and its leader Giorgia Meloni were the clear winners, collecting 26% of the votes. However, even if the other two major parties of the coalition, the League and Forza Italia (FI), obtained less than 9% each, their seats are decisive for the majority in Parliament and guaranteeing stability for the government (see Figure 1).

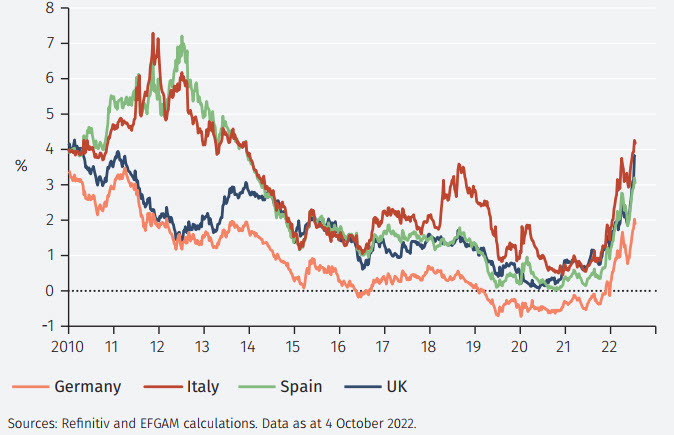

Markets reacted negatively to the outcome. The yield spread between Italian and German government bonds rose to almost 260 basis points the day after the vote (see Figure 2). Subsequently, the spread has fallen but, at the time of writing, remains above the levels prevailing in July before the collapse of the Draghi government led to early elections.

Many commentators fear that the next government will clash again with the European Union on fiscal policy as in 2018, during the coalition government of the Five Star Movement and the League. Reference is also made to the well-known pro-Russian positions of the League, to the personal friendship between Berlusconi, leader of FI, and Russian President Putin. It has also been noted that FdI and the League opposed the European Parliament’s request to block European funds to Hungary, something that will further add to tensions.

The new government will only take office in the second half of October. So far, would-be Prime Minster Meloni has made very cautious comments on fiscal policy, aligned with the position of Mario Draghi’s caretaker government. Nonetheless, investors fear for Italy’s reliability. To prevent spreads from increasing as in 2011 and 2018, the priority of the new cabinet must be to reassure international partners and financial markets.

In the coming weeks, three issues will be in the spotlight:

1. The composition of the government, in which highly respected personalities with an international profile should be included while excluding politicians responsible for past tensions with the EU;

2. The position on Russia, for which Meloni must confirm Italy’s alignment with the EU political line, including on sanctions;

3. The 2023 budget, which must balance managing the energy crisis, the economic slowdown, and the increase in borrowing costs following the ECB’s monetary policy tightening. It is encouraging that Meloni has maintained the constant dialogue with the Draghi government, which has already started the 2023 budget process, and has awareness of the need to act in continuity with the outgoing government.

In the medium term, high Italian public debt, now around 145% of the GDP, will keep markets focused on its sustainability. During the election campaign, the parties of the centre-right coalition indicated that reforming income tax and the pension system are priorities.

Regarding income taxes for households and corporates, the centre-right parties propose replacing the current system of progressive tax rates, as required by the Constitution, with a flat tax rate, although there is disagreement on its level among the three coalition partners.

FdI wants to increase minimum pensions while the League proposes the possibility of retiring with 41 years of contributions. This would stop the progressive increase in the retirement age that was implemented in line with the demographic trends envisaged by the 2011 pension reform. This was necessary to secure the public pension system’s long-term sustainability.

According to the Italian Public Accounts Observatory, the cost of these measures could reach EUR 90bn per year, about 4.7% of the GDP.1 In the centre-right program, part of these costs would be covered by the revision of citizenship income and the 110% super bonus for buildings renovations that improve their energy efficiency.2 These two measures cost around EUR30bn each year: halving this amount would save only around 0.8% of the GDP.3<.sup>

In the absence of further cuts in public spending, the centre-right flagship measures would jeopardize the sustainability of public debt. Furthermore, if as suggested by the market reaction to the UK government’s announcement of unfunded tax cuts, Italian government bond yields increased, the ECB could not activate the Transmission Protection Instrument as Italy would not be compliant with the EU Commission’s recommendations.

Finally, the respect of the rule of law and civil rights for minorities is another possible area of tension between the new Italian government and European institutions. As the clashes with Hungary and Poland show, the EU Parliament and Commission ensure that member countries respect the founding principles the European Union. If Italy were also found breaching those principles, EU funds may be blocked, including those of the Recovery and Resilience Plan, of which Italy is one of the main beneficiaries.

Conclusion

In conclusion, the reaction of the markets after the victory of the centre-right coalition in the Italian general elections reveals concern about the stability of the public accounts. Recent events in the UK offer Italian would-be Prime Minister Meloni a useful lesson: the markets will punish policies that undermine the reduction of public debt. To establish its credibility, it is important that the new cabinet includes individuals with high international standing and that it adopts policies in continuity with the outgoing Draghi government both on fiscal policy and on sanctions against Russia.

1 See https://osservatoriocpi.unicatt.it/ocpi-pubblicazioni-la-spesa-del-centrodestra

2 The citizenship income provides for the payment of a monthly allowance to the unemployed who actively undertake to look for a job, but the application of the measure has been characterized by frequent fraud and is held responsible for having exacerbated the shortages of personnel reported by companies after the end of the pandemic. The superbonus for building renovations provides for the granting of a tax credit of 110% of the expenditure if certain requirements, including that of improving the energy efficiency of buildings, are met.

3 See https://www.cgiamestre.com/110-spesi-20-mld-per-lo-09-degli-edifici-presenti-in-italia/ and https://www.open.online/2022/01/25/inps-dati-osservatorio-reddito-di-cittadinanza/#:~:text=Reddito%20di%20cittadinanza-,Inps%2C%20nel%202021%20il%20Reddito%20di%20cittadinanza%20%C3%A8,quasi%209%20miliardi%20di%20euro&text=Sono%20stati%20oltre%201%2C76,93%20milioni%20di%20persone%20coinvolte.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.