- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Chinese financial markets have suffered this year against a background of slowing growth and ongoing Covid restrictions. In this edition of Infocus, GianLuigi Mandruzzato and Daniel Murray look at recent developments in China's economy and financial markets for clues about a possible turnaround.

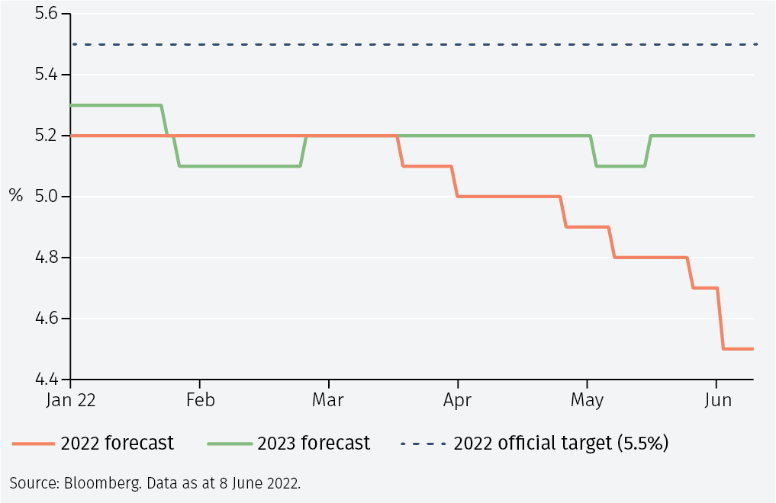

The Chinese economic outlook for 2022 has deteriorated as the year has progressed. Since the beginning of 2022, analysts have downgraded forecast GDP growth by around 0.5% and the expectation is now that the economy will expand at a rate nearly 1 percentage point below the government's official target of 5.5% (see Figure 1). In addition to the impact of the war in Ukraine and its influence on international trade and commodity prices, weak Chinese growth also reflects local factors.

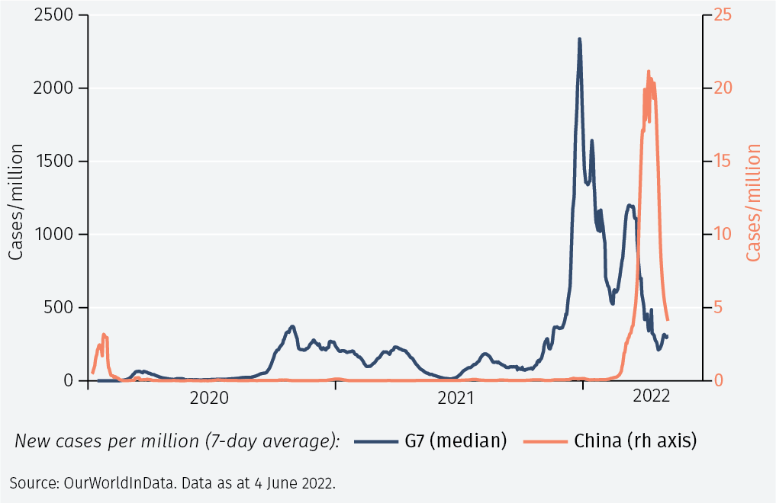

Since March, the rising number of Covid-19 cases prompted the Chinese government to impose strict lockdowns in many parts of the country, including Shanghai and the capital Beijing. This is despite the fact that the absolute numbers of infected people have remained relatively low, as shown in Figure 2. However, a concern for the Chinese authorities has been that vaccination rates are low amongst the elderly, hence the tight restrictions, which are thought to have affected about 400 million Chinese people. The measures taken have contained the number of new cases and allowed the authorities recently to announce some relaxation of restrictions in Shanghai and Beijing.

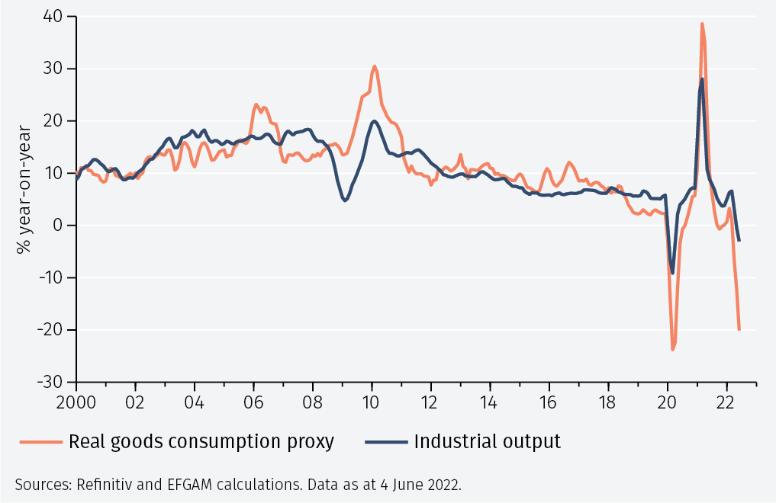

Many commentators do not expect any significant change to the zero-Covid policy before the Communist Party Congress in November when President Xi Jinping will seek a third term. If so, the impact on the economy will be prolonged. Economic data for April, the first period fully affected by the new anti-Covid measures, were weak. PMI indices, retail sales and new car registrations plummeted (see Figure 3). The 20% year-on-year drop in goods purchases was the steepest since early 2020 when the pandemic began. Furthermore, industrial production shrank from a year before. However, recently released PMI data for May showed a marked improvement, especially for the nonmanufacturing (services) sector.

PMI indices are comprised of various sub-indices. The new orders component is often viewed as the one that has the best short term forecasting properties. The weakness in new orders within China’s PMIs – shown in Figure 4 - suggests that, without new stimulus measures, Chinese GDP growth looks vulnerable in the coming months.

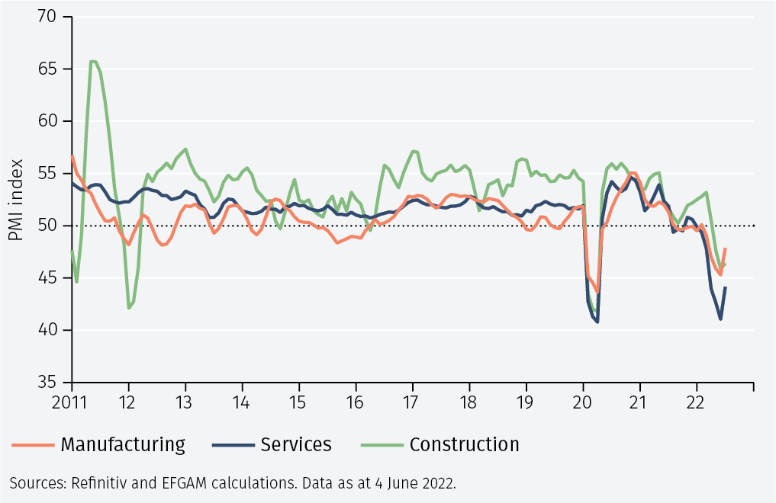

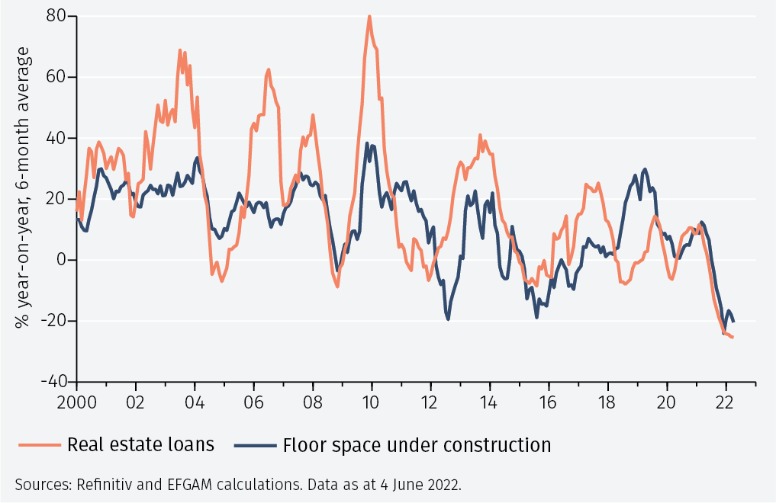

The construction sector has historically been a major driver of activity within the Chinese economy, fuelled by leverage, but that too is now facing headwinds. Policies designed to reduce the excesses of past years were adopted as early as 2021 and have weighed on the construction sector since then - see Figure 5. However, the government recently announced new infrastructure spending plans, something that could help to reinvigorate construction activity within the Chinese economy. Furthermore, Chinese banks have been officially urged to increase lending to the sector.

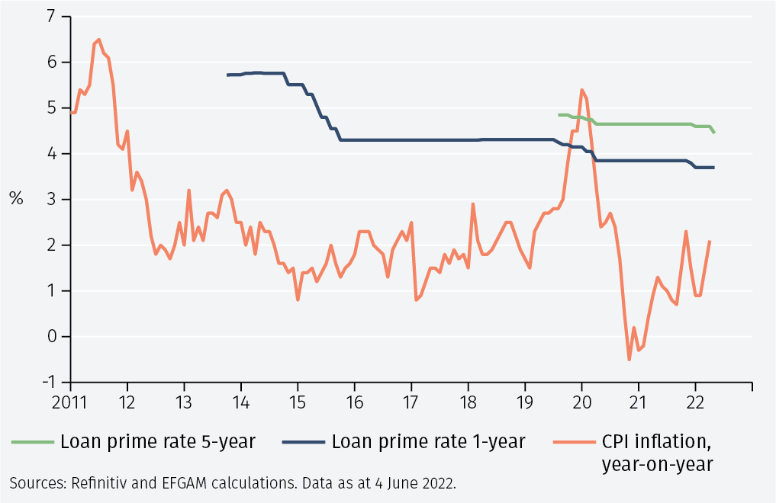

In contrast with the US and Europe, Chinese inflation remains well contained at only 2.1% year-on-year in April, below the official target of 3%. This gives the People’s Bank of China (PBoC) and the Chinese government flexibility to provide additional support to the economy. As part of official measures to support the housing sector and the economy more broadly, on 20 May the PBoC reduced the rate on long-term loans by 0.15 per cent to 4.45 per cent (see Figure 6), immediately benefiting the mortgage market. Expectations are that monetary policy will be loosened further. Additionally, Premier Li Keqiang recently stressed the importance of supporting growth, raising the expectation that more measures will be announced soon.

In fact, the Chinese authorities have announced a whole series of measures to support the economy over the past few months, including 33 that were announced by the State Council on 23 May alone and an CNY 800bn line of credit to support infrastructure projects announced on 1 June. A list of those that we have tracked is included in the Appendix.

In announcing these measures, the authorities are trying to achieve a delicate balance between enforcing the zerotolerance Covid policy whilst ensuring the economy is sufficiently strong to keep people employed and without causing further problems in the housing sector, which is already suffering from problems of excess leverage. This is not easy to achieve and perhaps helps explain why there has been a lot of talk from the authorities but relatively little implemented so far. For example, the tax rebates included as part of the 33 measures announced on 23 May sound impressive but amount to only 0.1% of GDP.

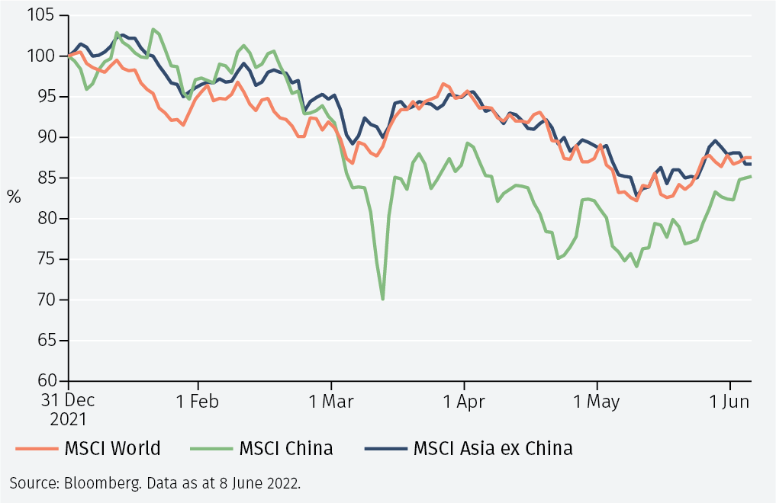

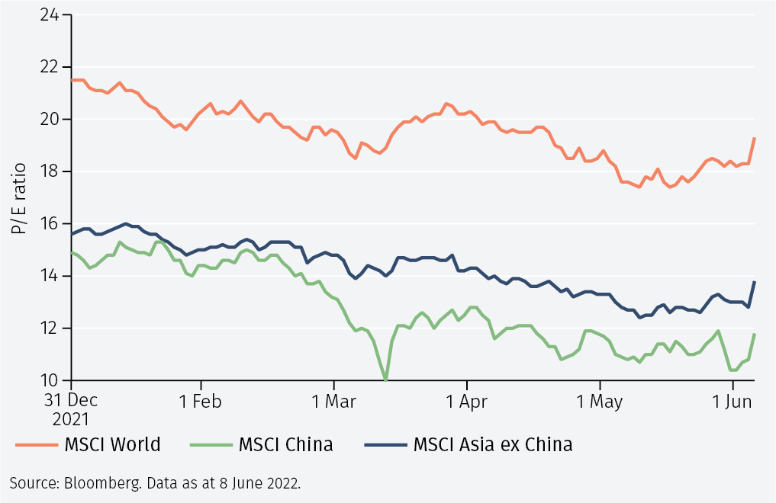

This is one reason why Chinese equity markets have performed poorly in 2022: the economy has been weak and markets have been disappointed by the lack of action, despite all the pronouncements. For the year to 2 June, the net total return from the MSCI China index in US dollar terms is -17.6%, compared to -12.2% and -12.1%, respectively, from the MSCI World and MSCI Asia ex China indices (see Figure 7 overleaf). As illustrated in the chart, much of the underperformance came in early March, since when Chinese equities have performed broadly in line with the rest of the world although in more volatile fashion.

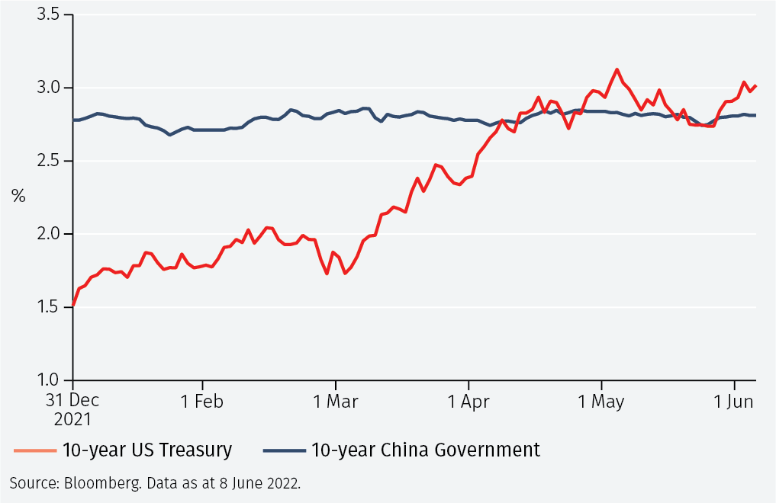

A part of the year-to-date underperformance of the MSCI China index in US dollars can be attributed currency weakness: the renminbi fell by 4.5% against the US dollar in the year to 2 June. In turn, this is associated with the observation that the yield gap between US and Chinese rates has disappeared since the start of the year – see Figure 8.

Chinese equities began the year already trading at a valuation discount to the rest of the world. A consequence of ongoing underperformance this year is that the valuation discount has widened, as shown in Figure 9. Moreover, with a trailing P/E ratio of around 11 and earnings cyclically depressed, valuations look cheap in absolute terms.

In summary, the Chinese economy has been unequivocally weak this year against a background of ongoing Covid lockdowns and problems in the rest of the world. It is not so surprising that Chinese equity markets have underperformed weak global equity markets in this context but what has been disappointing is that the implemented policy response has been so feeble, in contrast with previous periods of crisis. Chinese equity markets look cheap, although valuation by itself is rarely a sufficient catalyst for a market rally. What is now needed is for the authorities to follow through on their promises of supporting the economy. If that were to happen in a credible and sizeable way, the prospects for Chinese equities would improve quickly and meaningfully.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.