- Date:

Infocus - Joaquin Thul analyses the prospects for inflation in

Latin America and why central banks are better prepared to deal with it than before.

Since the start of 2021 inflation has picked-up across both developed and emerging economies. In Latin America, central banks have turned increasingly hawkish, tightening policy rates. In this issue of Infocus, Joaquin Thul analyses the prospects for inflation in the region and why central banks are better prepared to deal with it than before.

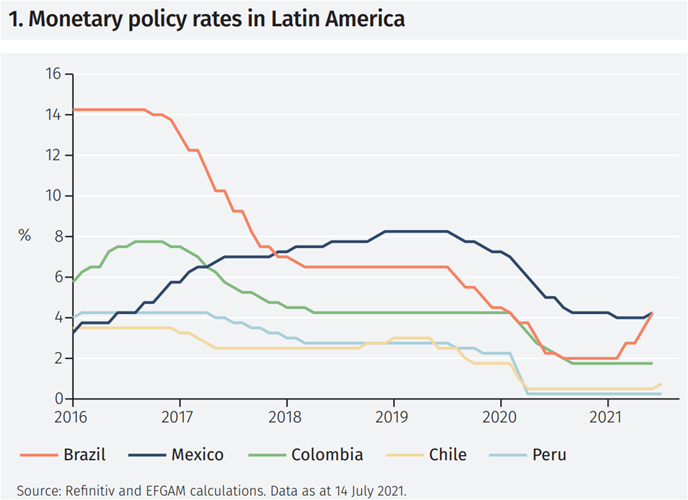

Inflationary pressures have risen across developed and emerging economies in recent months, triggering market concern. Although in the United States the CPI rose by 5.4% year-on-year in June, the highest rate since 2008, our analysis suggests US inflation will soften in the coming months.1 In Latin America, the resurgence of inflation has turned central banks increasingly hawkish, with tighter monetary policy in Brazil and Mexico from the historical lows observed during the Covid-19 crisis (see Figure 1).

However, the increase in inflation in Latin America is likely due to temporary factors and the weakness of aggregate demand suggests it will be short-lived. In addition, and in contrast with previous episodes of rising inflation in the region, the central banks are on this occasion better equipped to tackle it with more policy tools and higher credibility.

Temporary factors driving inflation

As the weak pandemic-hit data from last spring fall out of the calculations, inflation has naturally increased. The question is whether inflation is rising more than expected.

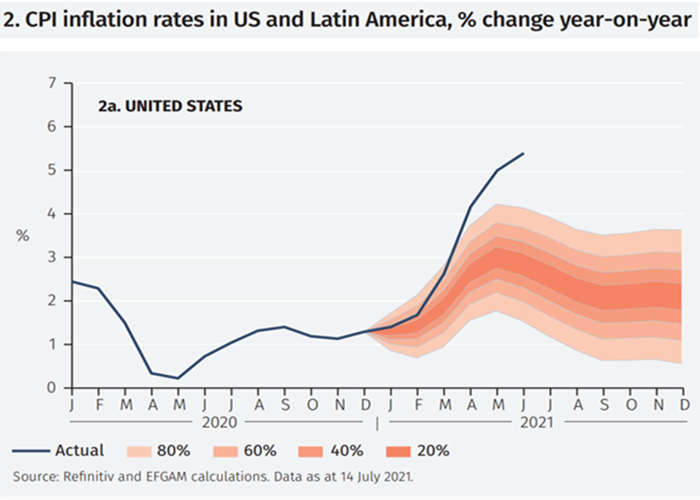

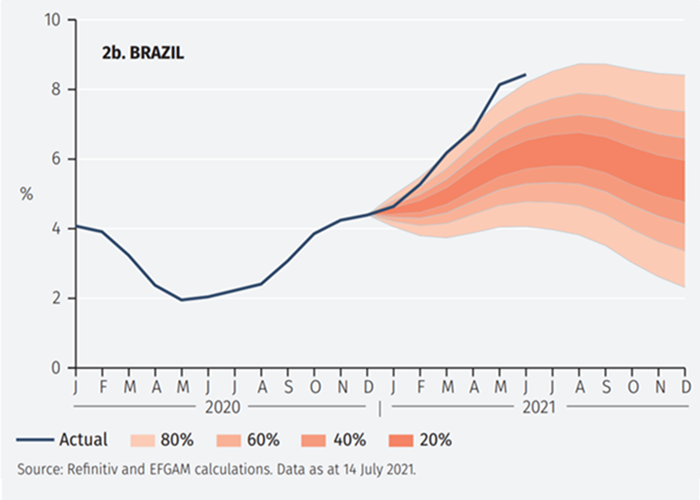

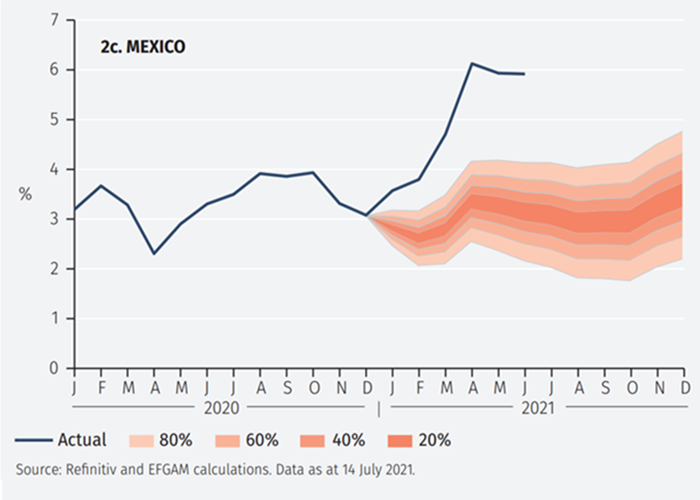

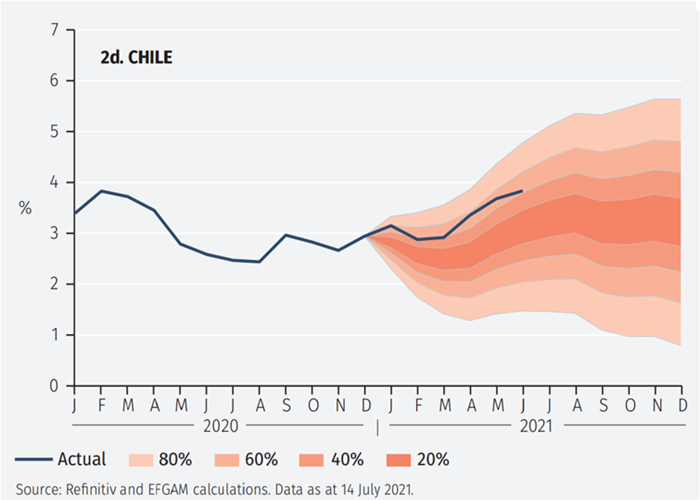

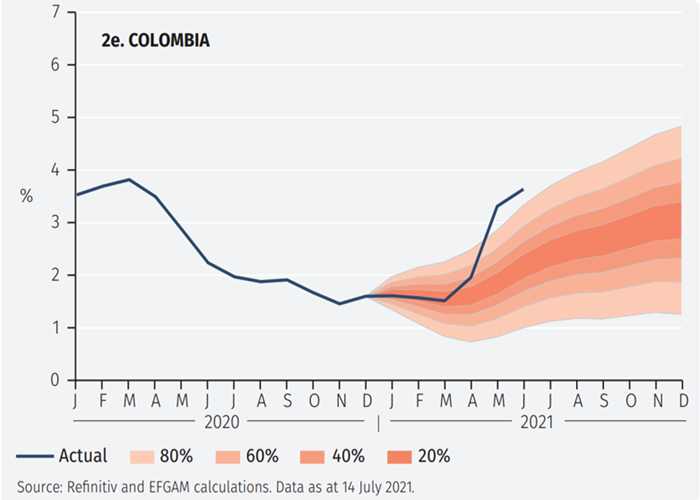

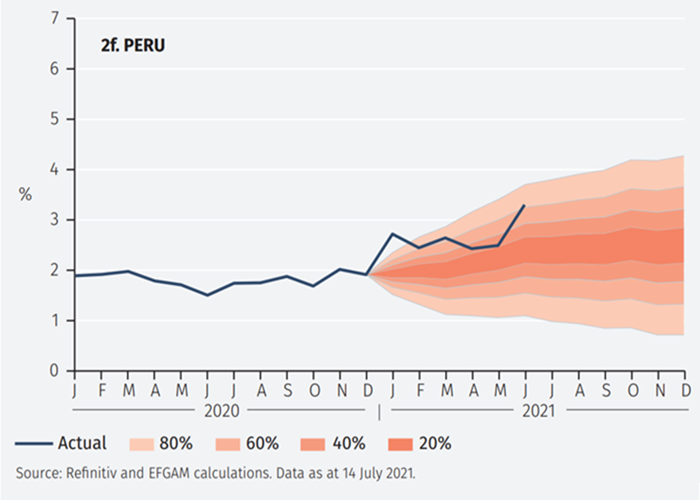

To determine whether inflation is unexpectedly strong, we estimate a model on data ending in December 2020 from Brazil, Mexico, Chile, Colombia and Peru and in the US, and use it to provide forecasts for 2021. The resultant ‘fan charts’ show the range of inflation outcomes that are compatible with the model (see Figure 2).2 The likelihood of being within the fan is 80%. Thus, if inflation stays in the fan, we conclude that it behaves as expected. If it is above the fan, however, then that is evidence that inflation pressures are unexpectedly strong.

The figures show that the rise in inflation in the US, Brazil, Mexico and Colombia is stronger than one would have expected, given its decline last year.

This rise in inflation has prompted central banks in Brazil and Mexico to take action to try to meet their targets and anchor inflation expectations. In Brazil, headline inflation exceeded 8% in May for the first time since 2016 driven by prices of industrial goods and electricity. Hence, the Brazilian central bank (BCB) increased the Selic rate three times bringing it to 4.25% from a historical-low of 2% at the start of 2021. The minutes of the last monetary policy meeting showed the BCB is committed to do “whatever it takes” to bring inflation down to the 3.50% target in 2022.

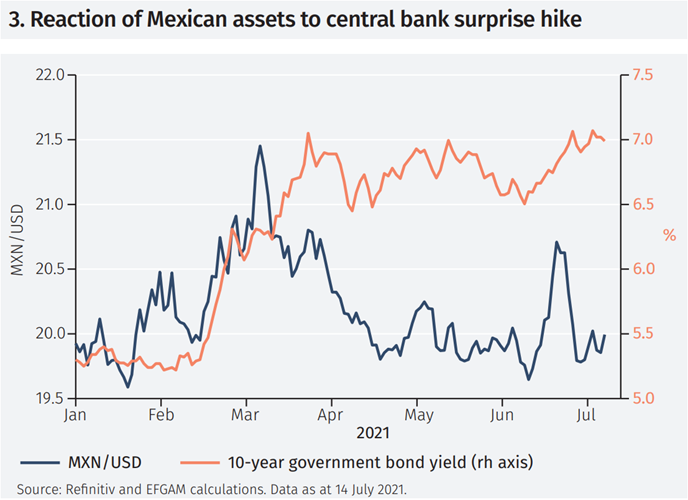

In Mexico, Banxico, the central bank, issued a hawkish statement after a surprise 25bps rate increase in June after annual CPI data climbed to 6% in May. In its last Quarterly Inflation Report, Banxico acknowledged inflation was running ahead of their forecast, but that they expect it to slow towards their target. However, in June the monetary policy committee decided to raise rates for the first time since 2018, sending a mixed message to the market due to the uncertainty over Banxico’s reaction function for the coming months. Markets in Mexico reacted swiftly, with 10-year government local currency bond yields rising above 7% and a strengthening of the Mexican peso against the US dollar (Figure 3). Our model suggests inflation in Brazil and Mexico will decline over the coming months as a result of their swift policy actions (see (Figures 2a, 2b and 2c).

In the Andean region, inflation has risen but remains below pre-pandemic levels; nonetheless, central banks have become more hawkish.

To continue reading, please use the button below to download the full article.

Footnotes

1 For more information see EFG Infocus, ‘How worried should we be about US inflation?, June 2021.

2 Fan charts are constructed to show the likelihood that actual inflation falls within the different coloured areas with a probability of 80%, 60%, 40% and 20%.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.