- Date:

Global house view & investment perspectives

Editorial

Welcome to the September edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

There is a continued focus in financial markets on the economic consequences of the coronavirus pandemic. The fact that the crisis is not yet fully over suggests that the economic costs are accumulating. At the same time, it seems increasingly likely that the initial contraction of economic activity was less bad than the forecasts made earlier this year. Economic surprise indices have risen strongly, reflecting the fact that economic data releases have been better than expected over the past few weeks. This trend encompasses both survey based data, like PMIs, and hard data, like consumer expenditure, industrial output and durable goods orders. Positive surprises have been most evident in the US, while European data have been more mixed; it would not be surprising if 2020 GDP forecasts, while still deeply negative, will be revised upward.

A second factor impacting market sentiment is the outlook for the US election. With both main parties having held their conventions and with about two months to the election, the campaigns have now moved into high gear. It appears that President Trump has been gaining support in recent days and has narrowed the lead of Democrat candidate former Vice-President Joe Biden. Several factors are relevant. Normally candidates poll better in the immediate aftermath of their conventions. If so, the rise in support may be temporary. However, President Trump’s support started to evaporate when the Covid crisis struck the US. The fact that the second wave of infections appears to be flattening out, coupled with the marked decline in mortality, may be enhancing President Trump’s support. So might the growing likelihood that there will be a vaccine in the not too distant future.

A third factor impacting asset markets is the recently announced outcome of the Fed’s review of its policy framework. This entails two main changes. First, a reduction in the importance the Fed attaches to tightening monetary policy pre-emptively, for example, because unemployment has declined to a low level even as inflation is below or at the objective. The Fed noted that a tight labour market is beneficial, in particular to low income communities.

Second, the Fed introduced “flexible average inflation targeting,” which implies that it will take past misses of its 2% inflation objective into account in setting policy. Since inflation has averaged 1.6% over the last decade, it appears that the Fed will not be quick to reign it in if and when inflation rises above the objective.

Under these circumstances, and bearing in mind the risk of increased volatility until the US elections, a slight preference for equities over bonds in a diversified portfolio remains warranted. The markets that offer the most attractive risk reward are the US and Asia. When a rotation towards value sectors occurs, European equities will also benefit. Finally, gold will continue to be supported by the expectation of a very accommodative policy mix. The yellow metal offers a natural hedge against the risks stemming from both market volatility and longer-term inflation.

Global Asset Allocation: Summary

Equities

- The US continues to be the best performing developed market and we maintain our overweight to US equities. We maintain an emphasis on growth stocks which have outpaced value, particularly on a year-to-date basis.

- We upgraded European stocks in previous months, but conditions do not yet warrant an overweight position, preferring to wait until there is a greater shift into value.

- We are neutral on the Swiss market which has been relatively stable over the year, moving more into mid-caps given improvements in economic growth.

- Emerging markets are still playing catch up, although China is an exception. Being one of the strongest performing markets this year we stick with our overweight to Chinese equities and indeed for North Asia as a whole.

- Latin America and Eastern Europe are our least favoured equity regions, contending with oil price weakness, the economic impact of coronavirus and political noise.

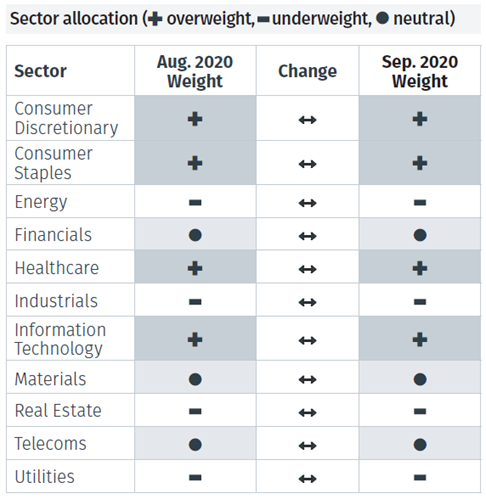

- No sector changes were made this month as we wait for relative momentum shifts. Industrials are an upgrade target with financials being a downgrade target.

Fixed Income

- While right now investment grade bonds look relatively expensive, we still need to manage risk and so we keep our overweight positioning. They could become a candidate to be downgraded to neutral if spreads continue to narrow.

- No major changes were made this month to our fixed income positioning. Dependent on market conditions, we are considering moving back into emerging market bonds and high yield bonds in the future which we are currently neutral on.

- Once again convertible bonds have had a good month. We stay overweight and look for equity sensitivity with a floor.

Alternative Investments

- Our call to upgrade industrial metals a few months ago has worked well as prices have picked up and leading indicators have shown signs of improvement.

- Oil prices are recovering but it will likely take a while for them to move back into their historic range. Given high oil inventory levels, we hold an underweight view but if prices continue their recovery we could look to add to exposure.

- We remain underweight on infrastructure as budgets will be constrained and liquidity is poor. However, once there is greater evidence of sustained economic recovery, infrastructure could be an interesting alternative to some fixed income plays.

Currencies

- Following last month’s downgrade, we hold our weaker dollar view, looking for PPP valuation levels to be the driver to currency moves going forward.

- There has been some consolidation of the euro following its strong run, but we continue to favour the currency on a tactical basis.

- While the UK pound has also shown strength against the dollar, we still hold a tactically underweight view on the currency given uncertainties, including the lack of clarity on Brexit trade talks.

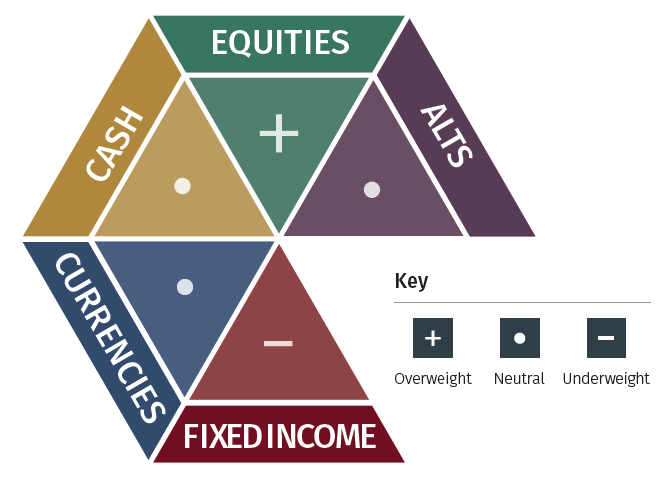

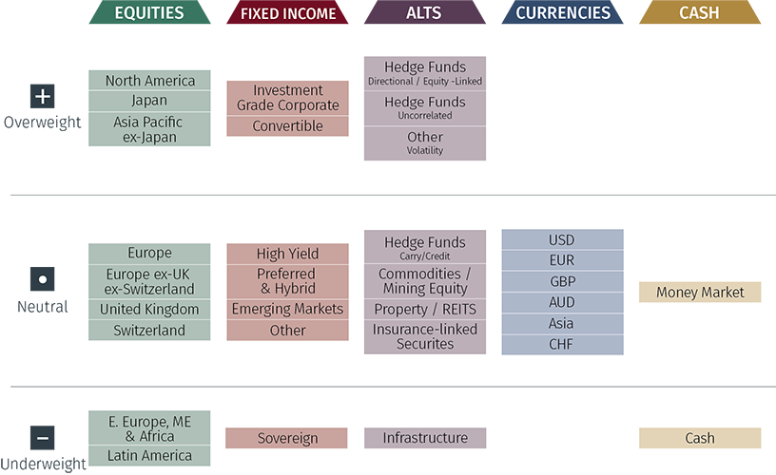

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Asset Class Breakdown

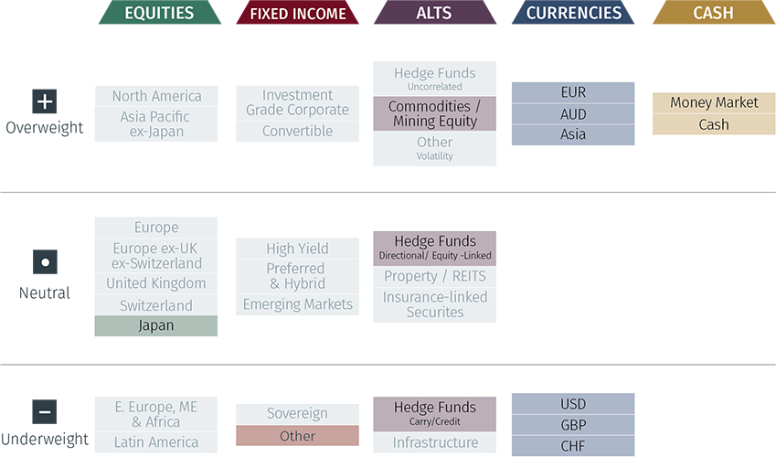

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.