- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the September edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The equity market rally has continued, with the gain for the MSCI World All Countries index in US dollars around 15% for the year to end August. The equity advance was driven by developed markets, with the US leading the way, while emerging markets suffered due to weakness of the Chinese market, weighed down by government interventions in various sectors. Market participants remain optimistic about the evolution of the economy and corporate profits despite increases in coronavirus cases associated with the spread of the Delta variant.

What gives markets confidence is evidence that, at least so far, the increase in infections has not put a strain on healthcare systems in developed countries, where the percentage of the adult population that is vaccinated is higher than that of developing countries. If this continues to be the case, possibly with an administration of a new vaccine dose, the gradual reopening of the economy should continue. This will benefit both employment and the profits of listed companies, thus supporting share prices.

In this context, the expected start of the normalisation of the Federal Reserve’s monetary policy lends itself to a favourable interpretation by investors. Once again this year, the Jackson Hole symposium was framed as the occasion for important monetary policy announcements. Fed Chairman Powell emphasised the recovery of the economy and the labour market in recent months, suggesting it will be possible to taper government bond purchases by the end of the year. Powell signalled, however, that tapering should not be interpreted as a precursor to higher rates. In fact, the FOMC has defined more stringent requirements in terms of the progress of the economy and inflation that must be met before rate hikes will be discussed. Interest rates will remain at current levels for a long time to come, during which time monetary policy will still be supportive of the economy and financial markets.

Furthermore, Powell's message in Jackson Hole confirms that the economic and monetary policy cycle is more advanced in the US than in other major economies. These conditions are favourable for the US dollar, which is expected to remain relatively strong for the near term. This will be more evident against the euro as the ECB has indicated that it will not change its monetary policy until at least the end of the first quarter of next year.

The supportive policy mix continues to favour global equities. A diversified portfolio should see a moderate overweight in equities, with a preference for the US and Asian markets – the latter have recently cheapened. In contrast, government and corporate bond yields are not attractive at current low levels and the fixed income allocation should rather include convertible bonds and hybrids. The firming of the US dollar is normally a headwind for industrial metals and gold that, unsurprisingly, have recently been relatively weak; although they remain attractive on a longer-term, fundamental basis, their performance will likely be capped in the short-term.

Global Asset Allocation: Summary

Equities

- Following a strong second quarter US earnings season we feel that Growth stocks have beaten expectations, relative to Value stocks. We continue to hold our US overweight.

- There has been discussion around reducing our allocation to Asia equities to make way for an increased allocation to Europe. However, valuations in Asia are relatively cheap so we prefer to wait before making any changes.

- European equities performed well during August as concerns over the pace of economic recovery faded. Any seasonal pullback could provide a good opportunity to increase our allocation.

- We continue to gain confidence in Japanese equities as strong earnings and attractive valuations reinforce our overweight positioning.

- Inflation has picked up in Brazil and Mexico, prompting their central banks to take action and anchor expectations. There is still caution on Latin America equities, given political noise which could delay the economic recovery.

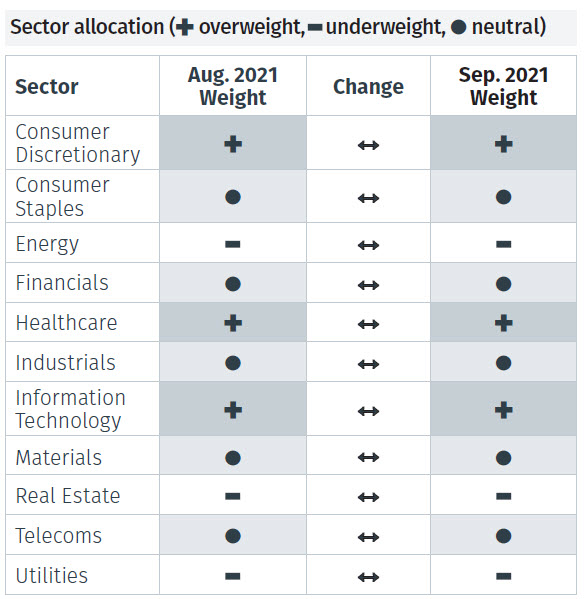

- No changes were made to our sector allocation for the month, although Consumer Discretionary is losing some of its strength while the Materials sector is now in an uptrend.

Fixed Income

- August proved a fairly quiet month for fixed income markets, with corporate bonds, high yield and emerging market bonds flat. With that in mind no changes were made to our fixed income allocation.

- Preferred & hybrid and convertible bonds continue to be our favoured areas of fixed income.

- Investment grade corporate bond spreads have stabilised over the last month, following a decline earlier this year, encouraged by widespread central bank support. We maintain a neutral position on a risk management basis.

Alternative Investments

- We are downgrading Commodities and Mining Equity to neutral on a tactical basis. Valuations on mining equities look expensive in our view and an expected slowdown in China will weigh on the sector. We maintain our neutral positioning on gold and underweight in energy.

- Property/REITS are being upgraded to overweight on a tactical basis, while we remain strategically neutral. Interest rates are low and improvements in employment and economic activity provide a positive backdrop for the sector.

Currencies

- The US dollar was recently upgraded to neutral on a tactical basis, as it continues to strengthen against most major currencies.

- In the previous month we downgraded the euro to neutral and it has further weakened.

- Commitments on the Australian dollar have fallen sharply, which is consistent with ongoing issues in the country as it continues to deal with the spread of the Delta variant, preventing a reopening of the economy. Also, the currency has been impacted by developments in commodity prices, which have had a weak month. Despite this we remain tactically overweight.

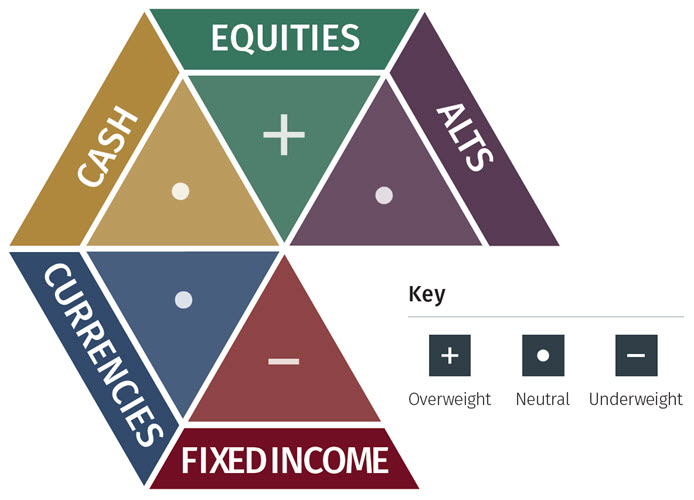

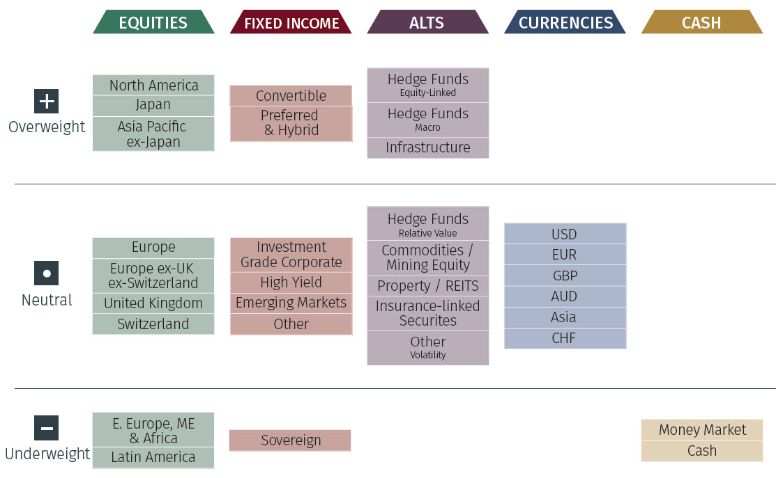

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breakdown

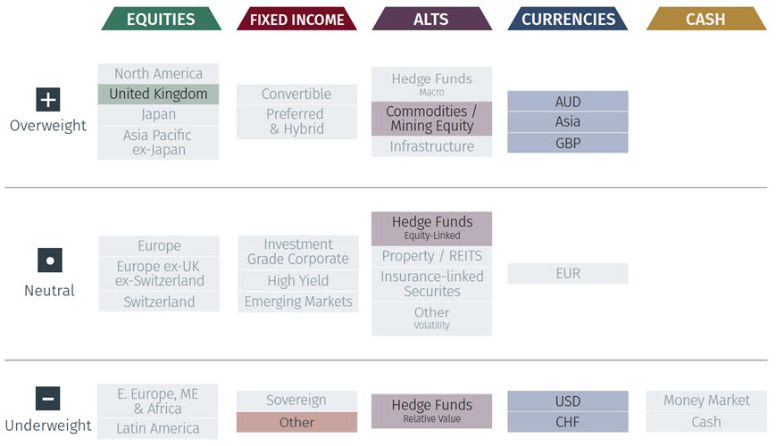

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.