- Date:

With the war in Ukraine ongoing, Sam Jochim summarises recent military and political developments and their potential impacts on markets in this Macro Flash Note.

With the war in Ukraine ongoing, Sam Jochim summarises recent military and political developments and their potential impacts on markets in this Macro Flash Note.

- Russian forces continue to shell cities across Ukraine, with focus shifting to advancing on Kyiv. Ukraine’s capital city entered a state of curfew on the evening of Tuesday 16th and remained in this state until the morning of Thursday 17th March. According to a Ukrainian presidential adviser, almost 30,000 people were evacuated from cities on Tuesday. The UN is reporting that Russia has caused over USD 100 billion worth of damage so far in its invasion.

- Russia’s invasion forces are still struggling to make meaningful gains, with the exception of Mariupol. The Ukrainian force’s tactics have “adeptly exploited Russia’s lack of manoeuvre, frustrating the Russian advance and inflicting heavy losses on the invading forces”, according to an assessment by the UK Ministry of Defence. UK Foreign Secretary Liz Truss warned that Putin, who was branded a “war criminal” by US President Joe Biden for the first time on Wednesday, is resorting to extremer techniques and weaponry as a result.

- There are renewed hopes, this week, of a diplomatic breakthrough as Ukrainian President Zelensky said Russia is beginning to “sound more realistic” following a fourth round of talks. Russia’s foreign minister Lavrov was also quoted saying there is “hope for compromise”. The reason for this hope may be Ukraine’s apparent openness to adopting a neutral status. Zelensky has recognised that Ukraine cannot join NATO, which was one of Putin’s demands before the invasion took place. Despite this, it will take time for a breakthrough, with Ukrainian negotiator Podolyak speaking of “fundamental contradictions” during the talks.

- As fighting endures, Western leaders continue to support Ukraine, with the prime ministers of Poland, Czech Republic, and Slovenia travelling to meet President Zelensky in Kyiv. The US also announced a further USD 800 million in military support to Ukraine this week out of the USD 13.6 billion aid that Congress voted to give to Ukraine. This follows the address by Zelensky to US Congress requesting further backing in the war. The Ukraine President also asked for all US companies to exit the Russian market and repeated calls for a no-fly zone in Ukraine – something that NATO is unwilling to provide given the potential risk of escalation with Russia.

- The US raised concerns regarding China’s alignment with Russia in a meeting on Monday 14th. It also warned NATO allies that China had signalled its willingness to provide economic support to Russia following reports of a request for assistance from Moscow. Although China has denied these reports, the US warned China that it would face sanctions if it compensated Russia for losses from the economic sanctions. This is something that China will be keen to avoid, given that Beijing has already set the lowest economic growth target in three decades at 5.5% during China’s Two Sessions which concluded on 11th March. President Xi Jinping will be cautious of becoming too involved in a situation which could worsen the outlook in a year in which he is expected to secure a third term in power during the Communist Party’s 20th National Congress.

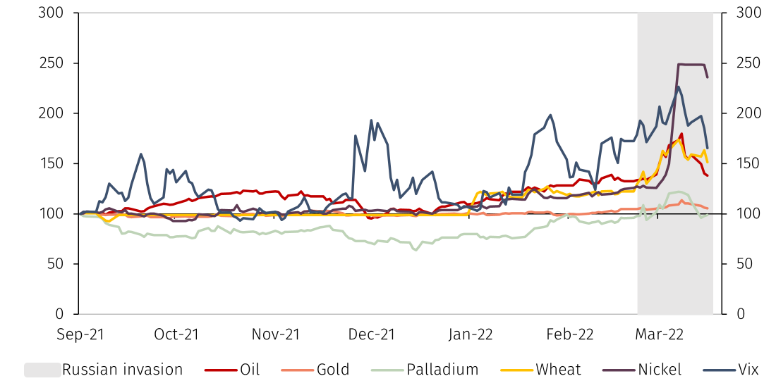

- Oil prices have fallen below USD 100 per barrel but remain 26.4% higher YTD. This may reflect a multitude of factors. China’s reaffirmation of its zero-Covid policy in the 2022 Government Work Report was followed by the implementation of lockdowns as cases spiked in multiple cities. Prices have fallen 13.1% so far this week however, which may go beyond the impact of the lockdowns and could suggest that the market is beginning to price in an end to the conflict given the optimism from Zelensky surrounding the talks with Russia.

- The easing of concerns over supply shortages has seen other commodities, which had also increased in price since the start of Russia’s invasion of Ukraine, fall this week. Palladium was up 14.2% since the start of the invasion. Following movements this week, it is now only 0.7% higher. Nickel remains 86.9% higher than at the start of the invasion but has fallen about 10% this week. There have also been movements out of gold this week as the VIX index of implied volatility has dropped below USD 30 for the first time this month, although it remains at a high level historically (see Chart 1). Wheat has also followed the commodity market trend and has fallen more than 10% from its peak, highlighting the hopes of a resolution.

Source: Refinitiv and EFGAM Calculations. Data as at 17.03.2022.

- Equity markets also show signs of hope regarding a military de-escalation. Markets were already moving higher this week, even before the Fed’s rate hike and China’s committal to overseas listing of its companies and to further stimulus for its economy. Most of the damage to the S&P 500 was done in January, with the index falling 9.2% from the start of the year to January 27th. From this date, it is now 0.7% higher and from the start of the invasion it is 1.6% higher. Despite this, it remains 8.6% lower YTD. European stocks have also bounced back this week, rising 5.5% but remaining 9.5% lower YTD.

- Other signs of hope for de-escalation include an increase in the US 10-year government bond yield from 1.84% at the end of February to 2.19% on March 16th. The Russian rouble has also recovered slightly. It would have depreciated 37.9% since the beginning of the invasion, however, a 21.4% appreciation this week leaves it 19.9% lower in value.1 We are continuing to assess the situation and adjusting our investment views accordingly.

1 Data as at 13:55 on March 17th , 2022

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.