- Date:

- Author:

- Stefan Gerlach

With the crisis in Ukraine escalating, there is growing concern that European economies will be affected. GianLuigi Mandruzzato looks at the risks faced by the Swiss economy.

The New York Fed published earlier this year an index of global supply chain disruptions. Last week it updated the index for January and February 2022. EFG Chief economist Stefan Gerlach provides a summary.

The surge in inflation over the past 12 months is often attributed to supply chain disruptions arising from the Covid-19 pandemic. With workers staying home because of the risk of contracting Covid or because of the need to take care of children at home from school or sick relatives, firms have struggled to maintain employment and output. With spending shifting from services to goods, global transport capacity has been overwhelmed. The net effect has been strong demand colliding with a weakened supply capacity, leading to upward pressures on goods prices.

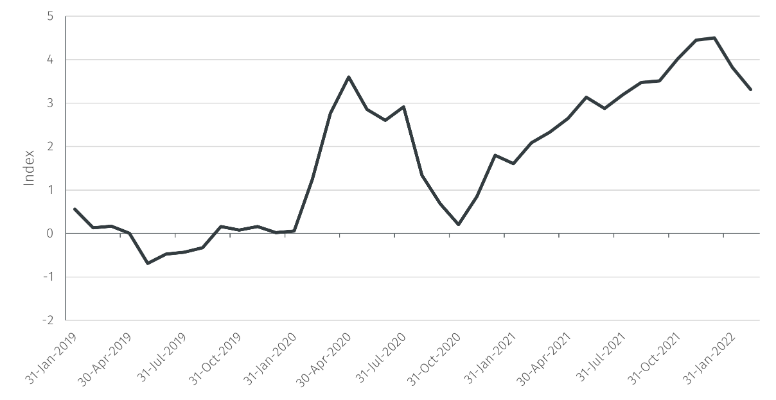

To gain a better understanding of this effect, the New York Fed published in January a study and data on supply chain disruptions (A New Barometer of Global Supply Chain Pressures by Gianluca Benigno, Julian di Giovanni, Jan J. J. Groen, and Adam I. Noble).1 On 3 March it published new data and an update by the same authors (Global Supply Chain Pressure Index: March 2022 Update).2

The new data for the global measure suggests that the supply chain disruptions have on balance become less severe in recent months. Thus, the global index fell from 4.50 in December 2021, to 3.82 in January and 3.31 in February.3 While this is an improvement, it remains the case that supply constraints are much greater than normal and that much more progress must be made before they have been fully resolved.

Source: NY Fed.

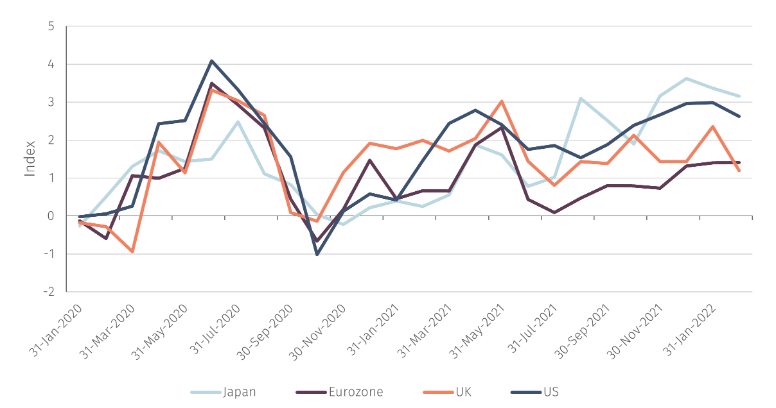

The new NY Fed study goes further than the earlier analysis in that it provides data for individual countries. This confirms that some countries have been worse affected than others. While the data point to supply chain tensions having declined since December 2021 in Japan, the UK and the US, they appear to have increased marginally in the eurozone. Furthermore, supply chain tensions are more severe in Japan and the US than in the eurozone or the UK.

Source: NY Fed.

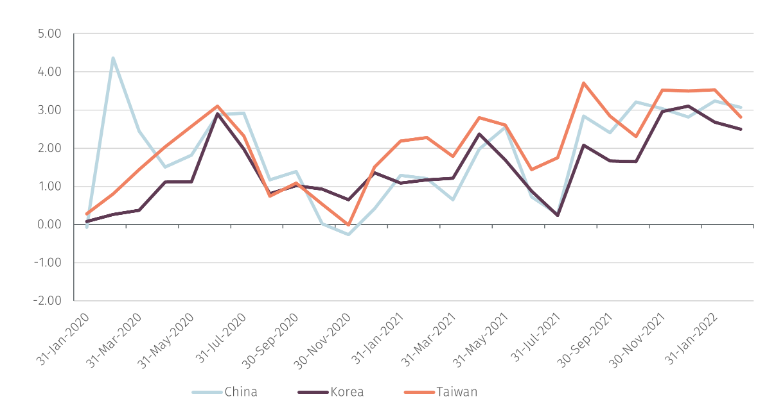

Supply chain tensions have also abated in Korea and Taiwan but have become marginally tighter in China. Nevertheless, in all three economies they remain severe.

Source: NY Fed.

Looking forward, the war in Ukraine is likely to tighten some of these supply chain constraints. For instance, Reuters reported on 2 March that the German carmakers association VDA had said that the invasion was disrupting transport routes as well as financial transactions and that it was bracing for shortages in a range of raw materials.4 The significance of these disruptions will depend on the length and severity of the war and on the sanctions imposed on Russia by the western powers. The full impact will become apparent over time although is not expected to diminish meaningfully in the short run.

1 See https://libertystreeteconomics.newyorkfed.org/2022/01/a-new-barometer-of-global-supply-chain-pressures/

2 See https://libertystreeteconomics.newyorkfed.org/2022/03/global-supply-chain-pressure-index-march-2022-update/

3 The index is constructed to have zero mean and a standard deviation of unity. A normally distributed random variable, “a bell curve”, is more than two standard deviations away from its mean in 5% of the observations. The index being 3 standard deviations away from its mean is thus an exceptional event.

4 See https://www.reuters.com/business/autos-transportation/german-carmakers-warn-fallout-ukraine-invasion-production-get-worse-2022-03-02/

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.