- Date:

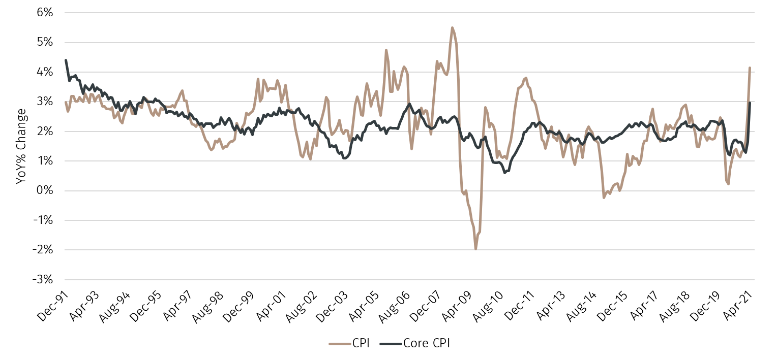

Yesterday’s US CPI release was much stronger than expected with headline inflation (measured as the year-on-year % change in the CPI) at its highest since September 2008 and core CPI inflation (ex food and energy) the highest since 1996. This has bolstered fears about a return to the stagflationary conditions of the 1970s which saw the unpalatable combination of high unemployment and high inflation coexist for a number of years. Rising commodity prices, supply chain problems (such as for semi-conductors), declining global trade and commercial rigidities resulting from Covid restrictions are all cited as reasons why we should be concerned about the rise in inflation being more than transitory.

There are a number of points to bear in mind with regard to this data release:

1. Inflation was expected to rise sharply anyway in April due to the much-publicised base effect: the year-on-year comparisons are easy for April and May because the CPI experienced a large dip this time last year. This effect will wash out in the months ahead.

2. The impact of the base effect will peak in May after which it will fade. Inflation may stay elevated for other reasons but the base effect will subside as the year progresses. The May CPI report will be released on 10th June so there is likely to be continued market nervousness about inflation for the next couple of months at least.

3. The data are often revised. Given the unusual circumstances of the past year it may be that the revisions are quite large. Yesterday’s shock may turn out to be smaller once the final data are released.

4. The June CPI report will be released on 13th July. Only then will it become clearer the extent to which higher inflation has been driven by the base effect or other factors. However, uncertainty will still remain. Only if inflation falls quickly and remains low thereafter will fears subside.

5. Whilst our core view is that inflation will indeed fall back to levels consistent with the Federal Reserve’s objectives, the upside risks have increased.

6. Central banks have for at least the past decade struggled to get CPI inflation higher despite exceptionally accommodative monetary policy. It is somewhat ironic then that now some inflation has returned nerves are running high. Whilst there may be some short term jitters, inflation that is structurally a bit higher over the next 10 years than it was over the last 10 years would be no bad thing. It would, for example, help to reduce the real burden of debt – government, household and corporate.

7. Various Federal Reserve governors and regional bank presidents have reiterated a consistently dovish message over the past couple of months. Even if inflation is above target for a bit that is of no great concern, especially given that there are now eight million fewer people employed than at the pre-Covid peak. Moreover, the Fed has emphasised the importance of the distribution of unemployment across different strata of US society, something that also affords a high degree of flexibility.

Overall then, the risks of persistently higher inflation have certainly risen recently and it is natural to be worried that the temporary factors lifting inflation do not subside as much as pure statistical models indicate. However, our core view remains that inflation will decline to more comfortable levels in the second half of the year. This will not become apparent until mid-July at the earliest; until then markets are likely to be sensitised to news flow perceived as supporting the high inflation hypothesis. If we are wrong and inflation is persistently higher, we expect the Federal Reserve to be patient in withdrawing stimulus.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.