- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

The past can normally provide some guidance regarding what to expect for the future. However, the highly unpredictable and far-reaching events of 2022 have created greater-than-normal uncertainty about developments in 2023.

Janus, the Roman god of beginnings and transitions, has two faces: one looking to the past, one to the future. January is the month named after him. As prospects for the global economy and financial markets are evaluated at the start of 2023, a look to the past can help us assess what the future may hold. However, with 2022 having been a year of highly unusual events – China’s zero-Covid approach, the Russia-Ukraine war and the rapid rise in interest rates – circumspection is in order.

China in the world

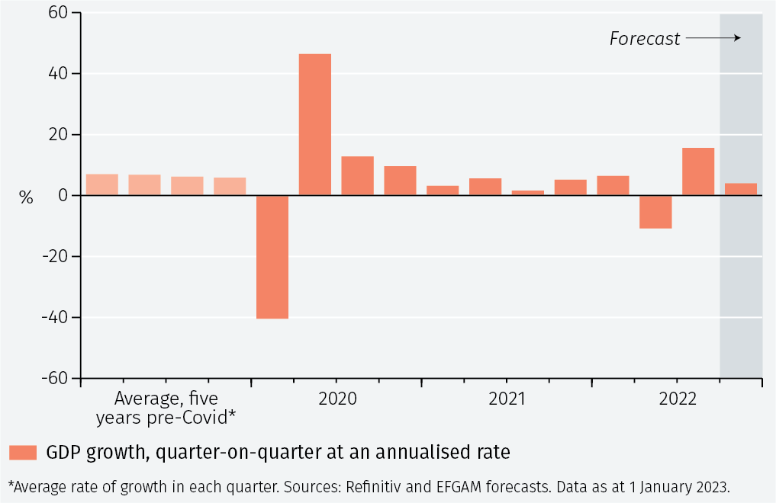

In China, the pre-Covid era was a strong and stable one. Economic growth ran at around 6-7% at an annualised rate (see Figure 1) between 2015 and 2019. Certainly, there were concerns about the veracity of that data and various measures sought to provide a more reliable indication. But even so, the gyrations of growth from 2020 to 2022 were particularly astonishing.

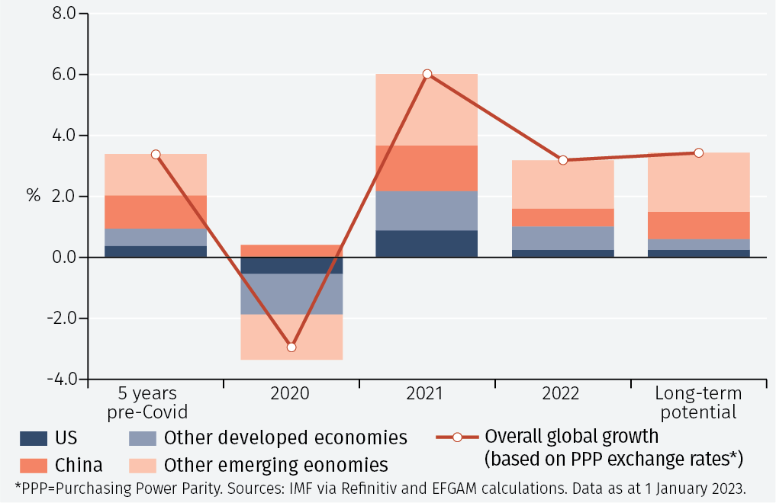

Looking forward, the issue is whether China can return to its former performance and once again provide a meaningful contribution to global growth (see Figure 2). A stronger contribution from China would indeed be welcome. Advanced economies are at varying degrees of recession risk, with the chances highest in Europe. China’s re-opening of its economy provides some grounds for optimism that it can return to its former role, although the limited efficacy of China’s home-produced vaccines and the absence of broad immunity pose the risk of renewed economic dislocation. Worker shortages due to sickness are already widely reported, with disruption to the global supply chain likely throughout 2023. In the short-term the mass travel associated with Chinese New Year, starting on 22 January, poses a significant risk.

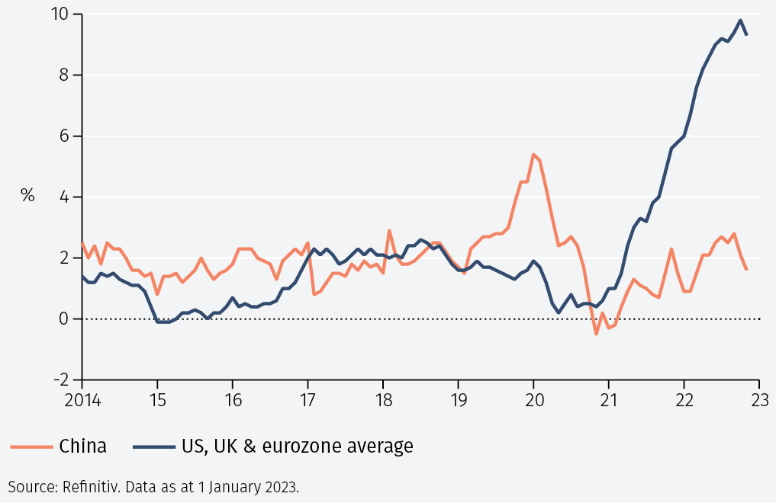

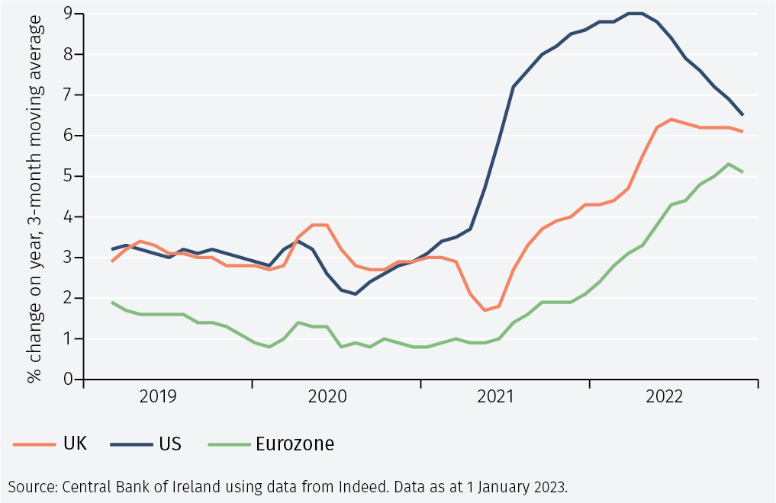

To help support growth, China can ease policy further, especially as inflation has remained subdued (see Figure 3). That is in sharp contrast to the advanced economies where inflation rates are still close to 10%. The good news for advanced economies is that there is some evidence, especially in the US, of wage growth moderating (see Figure 4). The risks of a wage-price spiral may well have been exaggerated.

China’s three constraints

Yet reducing interest rates in China is no guarantee of economic recovery and it faces three major structural challenges.

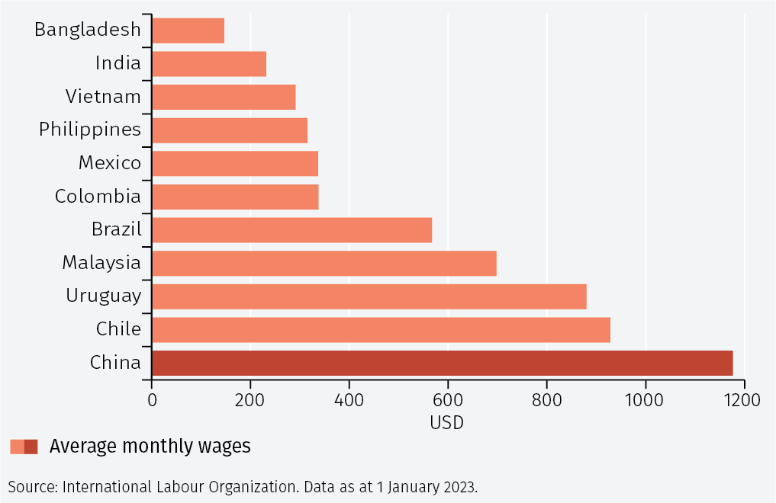

First, it is no longer an obviously cheap location for manufacturing. The days of the ‘China price’ when it could undercut manufacturing costs almost anywhere in the world are over. In Asia, many countries now have much lower labour costs. In Vietnam, monthly wages are a quarter of those in China (see Figure 5) and the economy is rapidly becoming a viable alternative (or, perhaps more accurately, a complement) to Chinese production. And, for the US, geographic proximity (‘near-shoring’) adds to the advantages of the low costs of Latin American labour. This is an important reason why we think other emerging economies (ex-China) are now in a stronger relative position to drive growth.

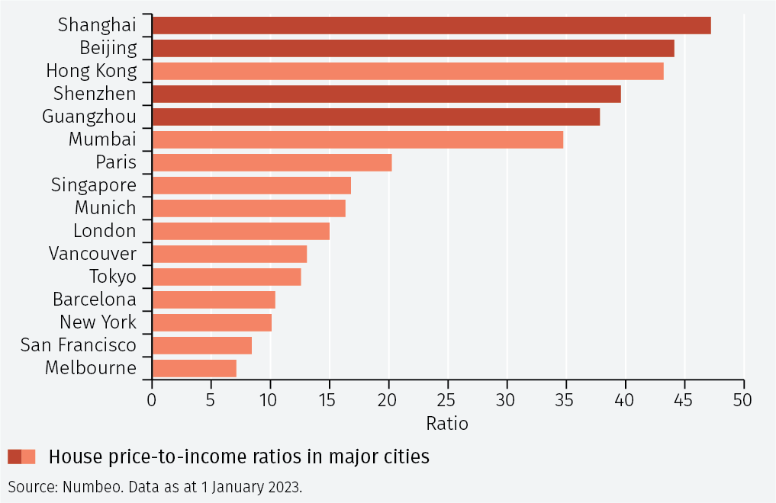

The second challenge relates to the housing market. China’s credit boom has fuelled house prices, which are now very high relative to incomes (see Figure 6) – much higher than in well-known expensive locations such as London, Vancouver and San Francisco. The boom and bust cycle in China’s property market may well take many years to evolve, although recent government actions will certainly be helpful in this regard.

Third, China’s demographics – a shrinking and ageing population – will seriously constrain long-term growth. India will overtake China as the country with the largest population in 2023 and its workforce is much younger.

Reopening and the rest of the world

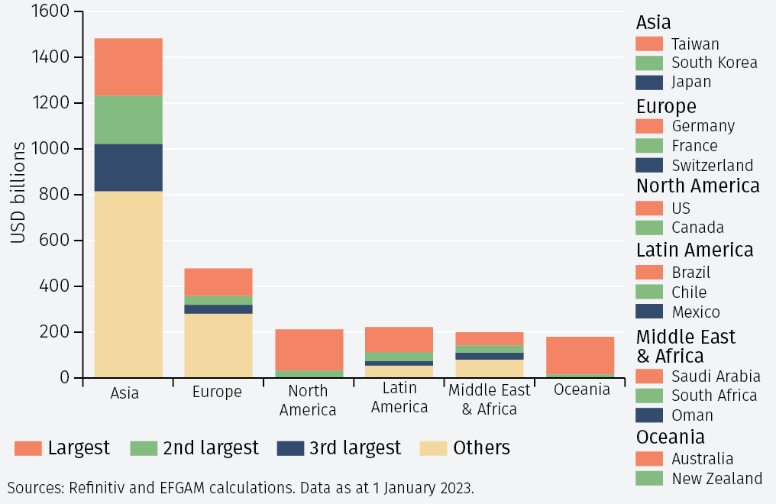

Even so, China’s reopening will provide some impetus to the rest of the world. In the past, China was characterised as an export-driven economy. That has not been an accurate description for some years: net trade – the balance between exports and imports – has provided only a small contribution to China’s growth for many years. What is often neglected is Chinese demand for the goods and services produced by other countries. Understandably, many of those come from China’s near neighbours. But European economies (Germany, Switzerland and France) and Latin America also benefit enormously from China’s demand (see Figure 7).

A longer look ahead

Although the focus at the start of the year is on the year ahead, longer-term prospects are important in helping to assess the economic outlook. A concern for the major advanced economies is that the shortage of workers will persist and constrain growth opportunities. Productivity trends may take up the slack but, realistically, that is more hope than well-founded expectation. The recent trend has been for weaker productivity. In emerging economies, we think that markets other than China can now play a much more important role in driving world growth. The countries in the MENA region are interesting in this respect.

To continue reading, please download the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.