- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the April edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

Central banks tend to tighten monetary policy until something breaks. Often that break has revealed itself as a failure of a financial institution following which the central bank, at least in the US, has stopped raising interest rates.

The month of March saw the bankruptcy of two medium-sized US banks and the merger between the two largest Swiss banks orchestrated by the federal authorities in the face of the liquidity crisis faced by Credit Suisse. Major central banks, including the Federal Reserve, the European Central Bank, the Bank of England, and the Swiss National Bank, continued with interest rate increases despite the instability that erupted in the financial sector. However, for the coming months it seems clear that recent events point to less restrictive monetary policy than central bankers had previously signalled they were considering and that the time for an expansive reversal of policy is now drawing closer.

This expectation is based on the historical observation that, after prior episodes of financial instability, the banking system has made access to credit more difficult for households and businesses even beyond what was induced by the actions of central banks. The lower availability of financing penalises GDP growth and slows inflation. Historically, a decline in inflation has also been associated with a drop in commodity prices, a development that has occurred in recent weeks.

This means that, in terms of portfolio allocation, a moderate overweight in equities and bonds remains warranted in our view. Within equities, the preference remains for emerging markets, and in particular Asia considering the expected recovery of the Chinese economy, at the expense of the US, UK and Swiss markets. Within fixed income assets, in our view government bonds now offer a more attractive mix of risk and return than over the past few years. Furthermore, in the context of less favourable financial conditions, government bonds could offer greater protection within a portfolio against possible spikes in market volatility.

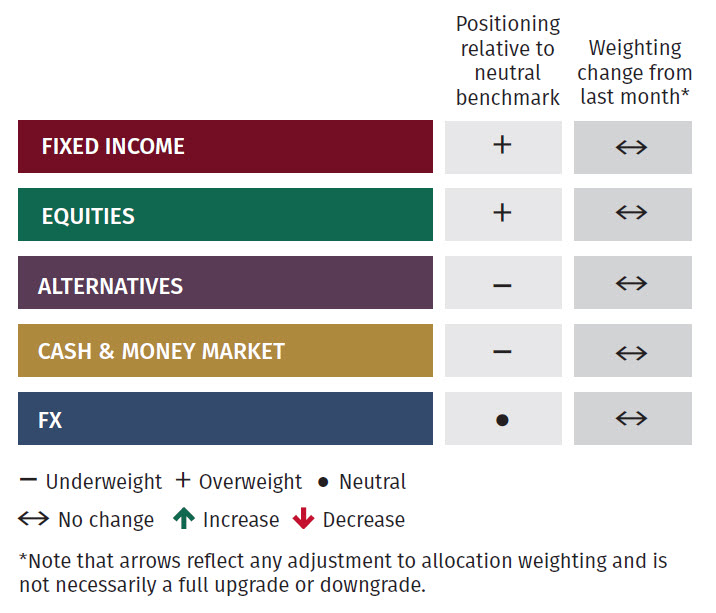

Asset Allocation

Global Allocation

Turmoil in the banking sector has caused a sharp reassessment of the outlook for interest rates around the world. This has contributed to a widening of high yield spreads, although they are not yet at levels that would represent an interesting buying opportunity. Government bonds have rallied across developed markets, with positive returns from US Treasuries, UK Gilts, German bunds and Swiss government bonds on the back of rising uncertainty.

These events have reaffirmed the weakening trend for the US dollar, as the euro, pound and yen rallied against it. Gold was the key beneficiary during the month. Volatility in equity markets has also increased over the month. Emerging markets continue to lag developed markets, driven by weakness in Emerging Europe and Brazil. On a style basis, growth stocks continue to outperform value stocks, consolidating a trend that started in February. Given the uncertain environment, no changes have been made to our allocation of broad asset classes, maintaining a slight overweight allocation to equities and fixed income.

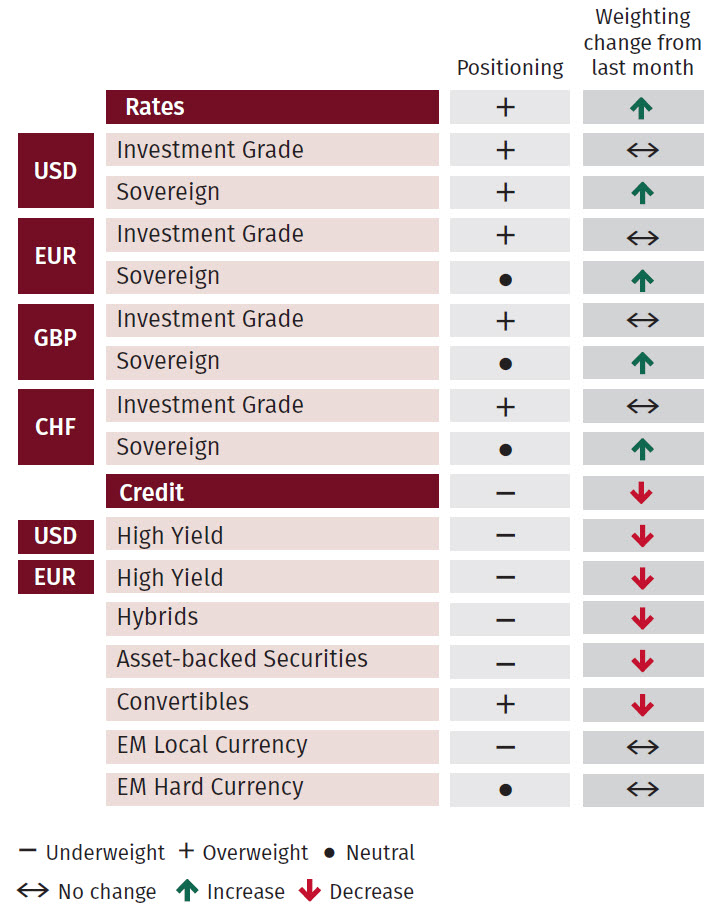

Fixed Income

One of the only changes to our sub-asset allocation this month has been to increase our exposure to sovereigns by 5% across all currencies, reducing the allocation to credit. This has meant that we are now overweight USD sovereigns and neutral for EUR, GBP and CHF rates. The deceleration of the global economy and uncertainty over the severity of the slowdown drives us to maintain a cautious stance.Additionally, given the increasing pressures that central banks will face to cut rates later in the year, we believe it is reasonable to be positioned with a bias towards sovereign and investment grade bonds. At this point, given the level of inversion of the US yield curve, we prefer to focus on gaining exposure to the 4-5 year part of the sovereign curve.

To make way for the increase in rates, we reduced our exposure to credit taking our positioning further underweight. This was done through a reduction in high yield, moving both euro and US dollar high yield to underweight from neutral. We also reduced our exposure to convertibles but still maintain an overweight position.

We are already heavily tilted to the rates part of fixed income versus credit. Therefore, once we have clear evidence of a slowdown in economic activity and more clarity on how the US yield curve will pivot, we could start adding additional duration to portfolios.

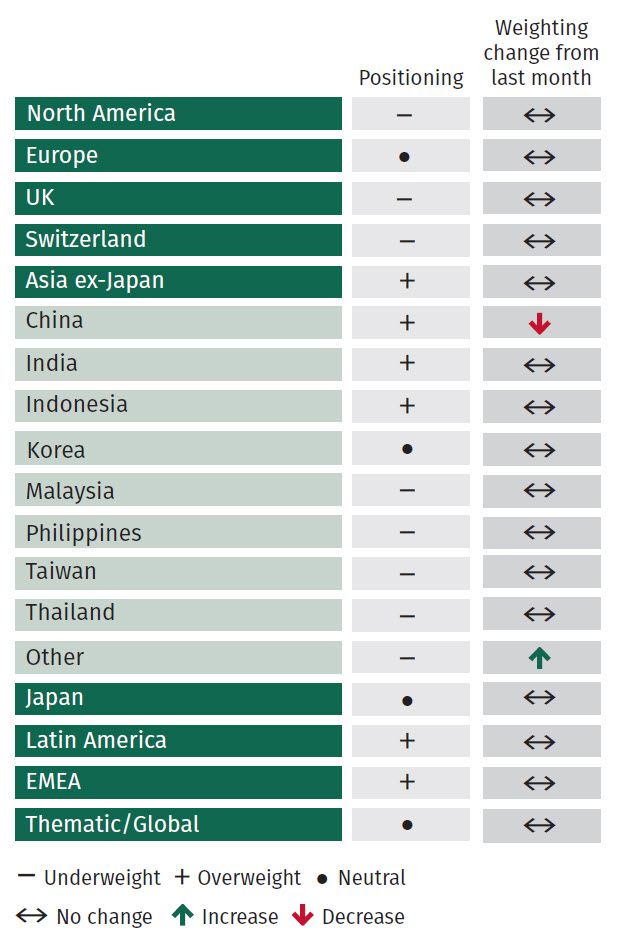

Equities

No changes were made to our regional equity positioning although there has been a slight adjustment to our benchmark neutral allocation resulting in some changes to positioning versus the benchmark. On the whole, technical factors still look good and momentum has turned positive, so in our view we maintain our view to have a slight overweight in equities despite market unease.

Technical factors in Europe remain strong, reinforcing our preference for European over US equities, while valuations in UK stocks have turned more neutral. We continue to prefer a bias to quality in portfolios given the current uncertain environment. The current exposure to equities should benefit from any potential rebound in markets, without taking excessive risk.

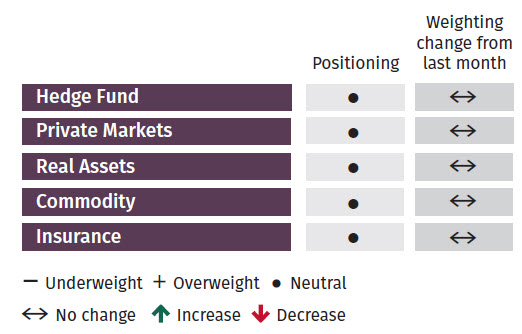

Alternatives

No changes were made to our alternatives exposure this month. We remain cautious on the real estate sector owing to liquidity concerns. Commodity positioning is neutral with our focus being on gold exposure. We note that oil continues to trend lower, as demand from China is still not yet reflected into the energy sector.

Within hedge funds, heightened volatility stemming from uncertainty in inflation and rates should be supportive for equity market neutral managers. Similarly, commodity trading advisor strategies are preferred in the context of more market volatility.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.