- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the August edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

After a strong June, markets enjoyed another positive month in July with the MSCI World index rising around 2% over the month. Global equities have now returned more than 16% year-to-date and are close to recouping the losses experienced in 2022. Fixed income markets also mostly registered positive returns in July. The Bloomberg Barclays Global Aggregate index was up about 1% for the month, though the year-to-date returns are significantly more muted than equities at just over 2%.

The strong performance in July reflects a macroeconomic environment in which activity has remained stronger than expected and recession fears have abated. The IMF’s World Economic Outlook update pointed to near-term resilience as it upgraded its GDP growth forecasts for 2023. Furthermore, headline inflation has rolled over, reflecting the mechanical impact of base effects due to high inflation in 2022, as well as declines in energy prices. However, core inflation has remained more persistent.

Markets have also taken note of favourable developments on the policy side. Despite core inflation’s persistence, central banks appear to be close to the end of monetary policy tightening cycles. In addition, China’s Politburo meeting concluded with recognition of the need to support domestic demand, though no specific measures were announced to do so.

The implications for the asset allocation of a diversified portfolio are that, in our view, maintaining moderate overweights in both equities and fixed income assets remains justified. Within equities, a preference remains for emerging markets and, in particular, Asia and Latin America. Japanese equities are also favoured and an underweight allocation to the US is retained to offset the overweights.

Within fixed income assets, longer-dated government bond yields continue to be attractive given monetary policy cycles are drawing to a conclusion and the diversification benefits. With the potential for the lagged impact of interest rate increases to cause a deterioration in the macroeconomic environment, a preference for high quality fixed income assets continues to be appropriate. This means that overweight allocations to investment grade and sovereign bonds remain funded by an underweight allocation to high yield bonds.

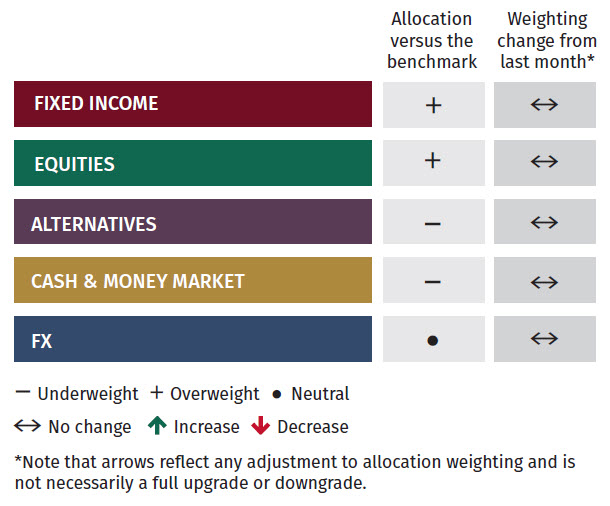

Asset Allocation

Global Allocation

The general macroeconomic environment continues to show disparities between leading and lagging indicators. Backward looking data continues to appear strong while forward looking data is weaker, with this juxtaposition helping explain market behaviour. One of the main risks of the coming months would be if core inflation remains too high, something which could lead to more volatile markets.

No changes were made to our allocations to the broad asset classes apart from adjustments taking into account the new neutral benchmark and market drift. We maintain a slight overweight allocation to equities and also a small overweight in fixed income. Underweights to alternatives and cash also remain. Hedging using put spreads is currently cheap relative to history although we would wait for the VIX volatility index to move a point or two lower before considering implementing outright hedges on portfolios. The potential rewards from implementing a hedge need to be weighed carefully against the premium cost.

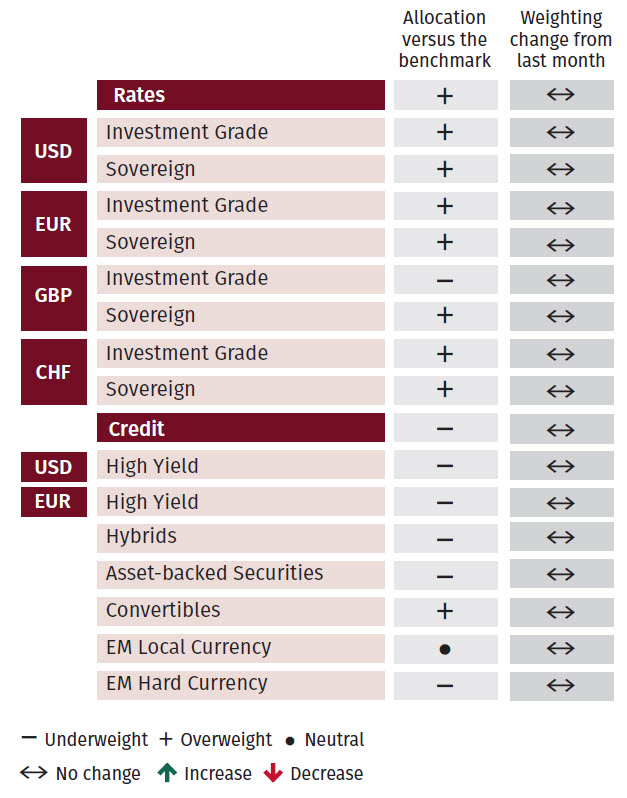

Fixed Income

Within the fixed income market, returns have been less pronounced than that of equities. Absent a sharp recession and dramatic unexpected improvement in the inflation outlook, it appears difficult for yields to rebound meaningfully. Nevertheless, year-to-date performance has been positive apart from for the UK.

Investment grade spreads appear relatively more attractive than high yield spreads in the US. The spread to worst of the ICE BofA US High Yield Index is close to its lower quartile while that of the Corporate Index appears in line with its median. The picture appears slightly better in terms of spreads for European and UK bonds.

Having duration exposure within fixed income provides a hedge against a deterioration in the macroeconomic environment. We maintain a bias to 5-7 years duration for the higher quality part of the market. Within high yield our preference would be at the shorter end of the curve which is less exposed to macro risks but could produce an attractive yield pick-up.

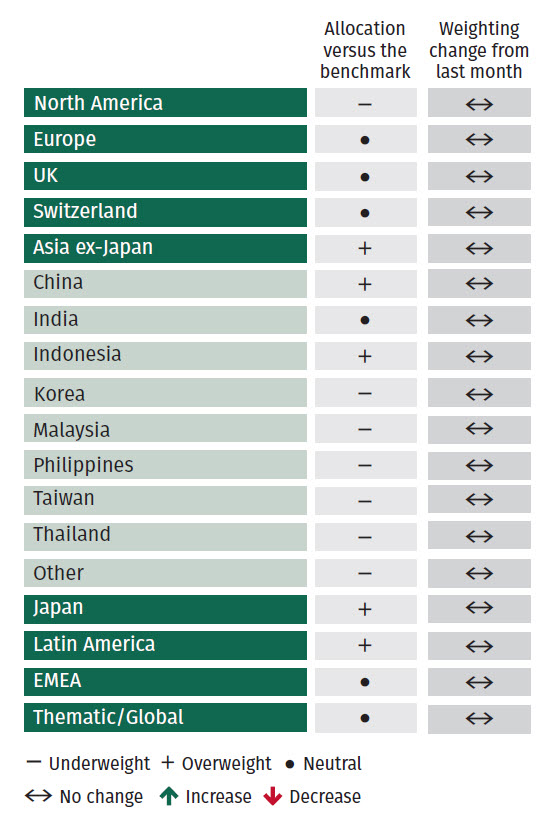

Equities

Absent any major market catalysts, we made no changes to our equity exposure. After their strong performance in the first half of the year, Japanese equities have seen a slower start to July. However, we continue to favour the market and expect a resumption of momentum. Our valuation models indicate that China has become relatively cheaper compared to June. We continue to have an overweight China allocation versus the benchmark, noting that any rebound in the market is likely to be front-loaded.

UK and Europe positioning continues to be in line with the neutral benchmark, supported by positive valuations and technicals offset by a more vulnerable macro situation. US positioning is underweight relative to the benchmark, although the absolute weighting dominates the equity exposure and we note growing odds of a soft landing scenario in the US.

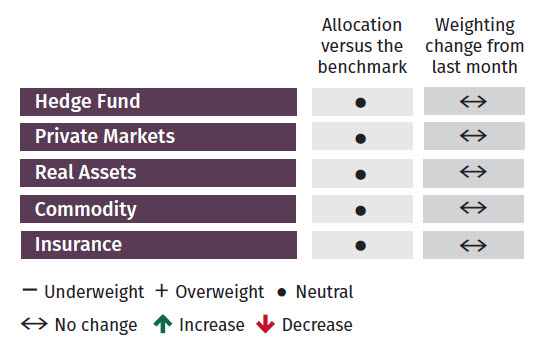

Alternatives

No changes were made to our alternatives exposure this month. Commodity positioning is neutral with a focus on gold. Indicators are currently pointing to a potential bottom for commodity prices although we will wait for confirmation of this trend in the second half of the year before adding exposure to industrial metals. We remain cautious on the real estate sector owing to liquidity concerns.

Within hedge funds, heightened volatility stemming from uncertainty in inflation and rates should be supportive for equity market neutral managers. Similarly, commodity trading advisor strategies are preferred in the context of more market volatility.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.