- Date:

- Author:

- Stefan Gerlach

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Has the dramatic tightening of monetary policy across world raised the risk of recession? That is the key question many investors are facing. In this Macro Flash Note, EFG Chief Economist Stefan Gerlach looks at the information contained in the OECD’s leading indicators and what it tells us about the prospects for the global economy over the next 12 months.

With inflation surging across the world – even above 10% in many countries – central banks have had little choice but to tighten monetary policy sharply. By raising interest rates by several hundred basis points in 12 months, the tightening so far has been dramatic, if not unprecedented, by the standards of modern economic history.

Higher interest rates are intended to slow demand growth to achieve a better balance between the supply and demand for goods and services. Since the peak effect of monetary tightening on demand is felt with a lag of perhaps three to six quarters, it is inherently difficult for central banks to calibrate how much to raise interest rates. Given the massive increases in interest rates, the risk that central banks have tightened too much, causing a deep recession, is obvious.

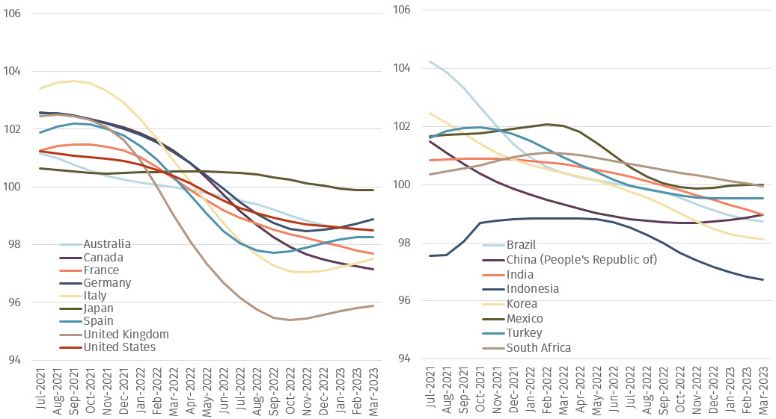

To assess that risk, it is useful to look at the behaviour of Leading Indicators (LI). The OECD computes leading indicators for a number of advanced and emerging economies (see below). These leading indicators average 100 and anticipate year-over-year GDP growth in 6-9 months’ time; values above 100 indicate expected expansion and values below 100 indicate expected contraction.

Source: OECD, data as of 6 April 2023.

The graphs show that in late 2021, economies were still expanding after the reopening after the Covid-19 pandemic. From early 2022, however, the rate of expansion slowed and by the summer of 2022 many leading indicators were well below 100, pointing to expected contraction.

In many advanced economies – with the notable exception of the US – the leading indicators have risen toward 100 in the second half of 2022. Among emerging economies, the situation is the reverse: with the exception of China, which benefits from the boost coming from its recent reopening after Covid-19, the leading indicators have fallen further below 100.

In drawing conclusions from these graphs, it should be recalled that in many cases the bulk of the monetary tightening took place in the second half of 2022. According to the OECD’s leading indicators, most countries are expected to experience a slowdown in economic growth as 2023 progresses and there is heightened risk of recession. However, the indicators suggest that any such slowdown will be much less pronounced than during the Global Financial Crisis. Furthermore, the recent uptick in the LIs of many advanced economies indicates that any macro-economic deterioration is expected to be short-lived.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.