- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The outcome of the upcoming European Central Bank (ECB) interest rate decision is unusually uncertain. The Governing Council will debate how much weight to put on backward and forward-looking data. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the factors that could shift the balance in favour of a new rate increase or a pause.

The outcome of the ECB’s meeting on 14 September will reflect the balance the Governing Council places on more hawkish backward-looking data versus more dovish forward-looking data.

Focusing on the hawkish case, it is clear that eurozone inflation is too high. In August, headline and core inflation both stood at 5.3% year-on-year (YoY), more than three percentage points above the ECB’s 2% objective (see Chart 1). Furthermore, the recent increase in fossil fuel prices raises the risk that inflation will consolidate at levels incompatible with the ECB's objective.

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 11 September 2023.

Eurozone 3-month interbank interest rates of around 3.85% are about 1.5 percentage points below the inflation rate of the past twelve months. Using a backward-looking approach, such negative real rates cannot be considered restrictive and do not guarantee that inflation will return to 2%. Another 0.25% rate increase would only bring real short-term interest rates closer to 0% and this should not cause an economic collapse despite the negative effect it would have on private sector cash flows. After the Governing Council’s dramatic failure to anticipate the surge in inflation, it may prefer to minimise the risk of repeating this mistake and proceed with rate increases.

An alternative approach considers the decline in inflation from the peak of 10.6% YoY in October 2022 and the moderation of the most recent monthly changes. In addition, in August producer prices fell by 7.6% from a year before, pointing to a further decrease in Harmonised Index of Consumer Prices (HICP) inflation towards the 2% objective (see Chart 1). If that were the case, real rates computed using expected inflation would already be significantly above zero exerting significant restriction on the economy.

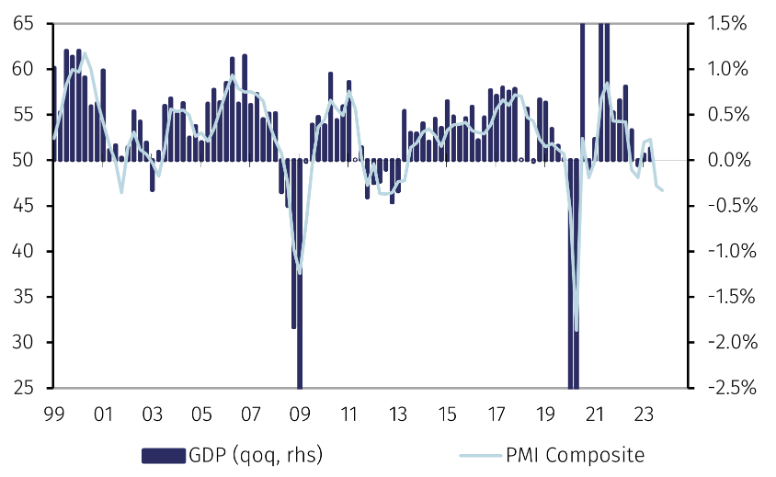

A decline in inflation will also be encouraged by a weakening of the economy. GDP growth was virtually zero between the last quarter of 2022 and the second quarter of 2023 (see Chart 2). In the three months to June, only the likely involuntary increase in inventories prevented a fall in GDP from the previous quarter but this bodes ill for growth in the coming months.

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 11 September 2023.

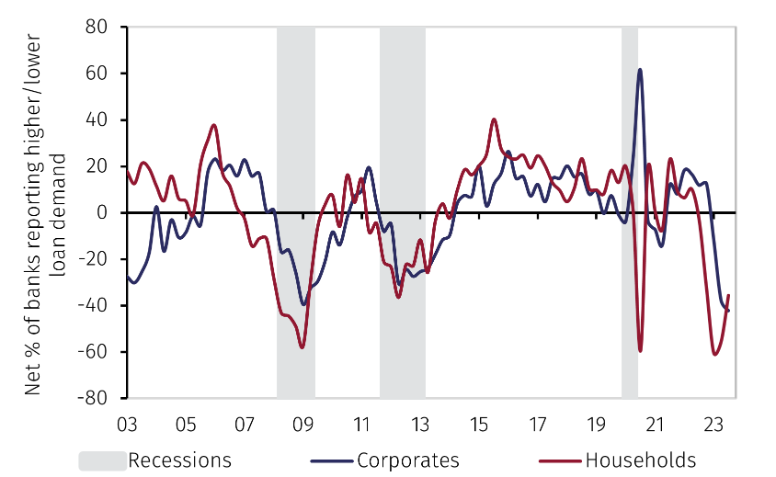

The weakness of the economy is evident in business surveys and bank lending data. The eurozone composite PMI index fell over the summer to levels that were only seen in past recessions (see Chart 2). Net flows of European bank lending to the private sector have been negligible over the last twelve months as reported credit demand has collapsed to levels not seen since the failure of Lehman Brothers (see Chart 3).

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 11 September 2023.

If concerns about economic growth and declining inflation prevail, it would be natural for the Governing Council to leave interest rates unchanged in September and take time to assess how to adjust monetary policy.

Markets appear to believe that the ECB will not raise interest rates much more, if at all. Futures contracts on 3-month interbank rates imply a probability of only around 40% of a 0.25% increase on 14 September. Barring new shocks, investors anticipate that the ECB overnight deposit rate will not exceed 4% in this cycle and that it will first be cut by mid-2024 (see Chart 4).

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 11 September 2023.

The market would therefore experience a negative shock if instead the ECB raises rates or signals that more rate increases are likely at future meetings. However, downside risks to growth, falling inflation and recent market volatility should prevent the ECB surprising markets with an overly hawkish stance. Refraining from raising rates in September while keeping all options open would be a market-friendly compromise between the hawks and the doves in the Governing Council.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.