- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

- Many investors think that by increasing concentration you increase the potential upside of an investment. This is true to an extent in equity investing as the theoretical upside is unlimited.

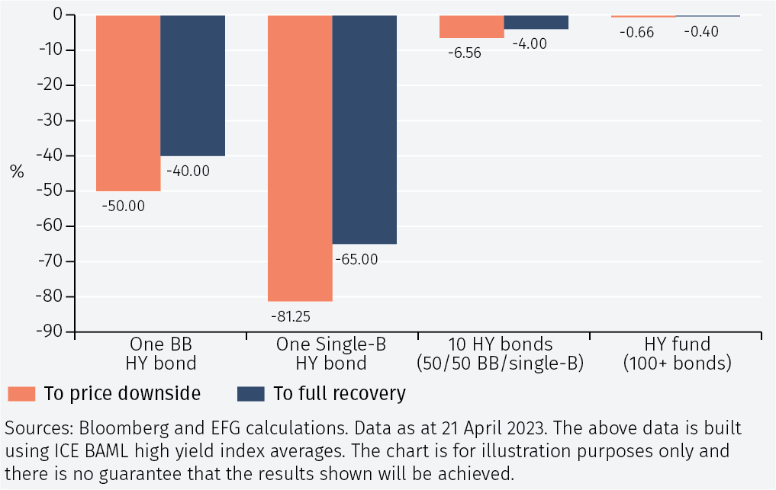

- However, this does not apply to fixed income as the upside of any one bond is limited to the yield and the downside is 100%.

- This is even more true in high yield as the risk of a default is elevated.

- Below, through illustrative examples, we will show that high yield concentration does not add any further upside return, increases downside risk and leads to much weaker liquidity.

- However, there is a sweet spot for diversification, that is you want to have enough to manage downside risk, but not too much to dilute the best ideas in the portfolio.

- An effective way to achieve this optimal level of diversification is through a fund.

Why diversification is essential in high yield

Even if the high yield positions are only a small part of a wider portfolio, by using a diversified portfolio or fund the long term return will likely be higher than owning a concentrated number of high yield positions as the negative impact of defaults on the wider portfolio can be minimised without giving up yield.

Many investors own high yield bonds to maturity with the goal of clipping the coupon (i.e. buying the bond to maturity with the goal of achieving a pre-specified yield). However the dangerous assumption here is that the company won’t get into trouble and have to restructure causing a permanent loss of capital. We like to say the strategy of clipping coupons in high yield is like picking up coins in front of a steam roller. Investors can still benefit from the attractive coupons in high yield, but one way to do this in a sophisticated manner is through the use of a fund that diversifies, takes an active approach, which aims to avoid problem companies, and pays out income.

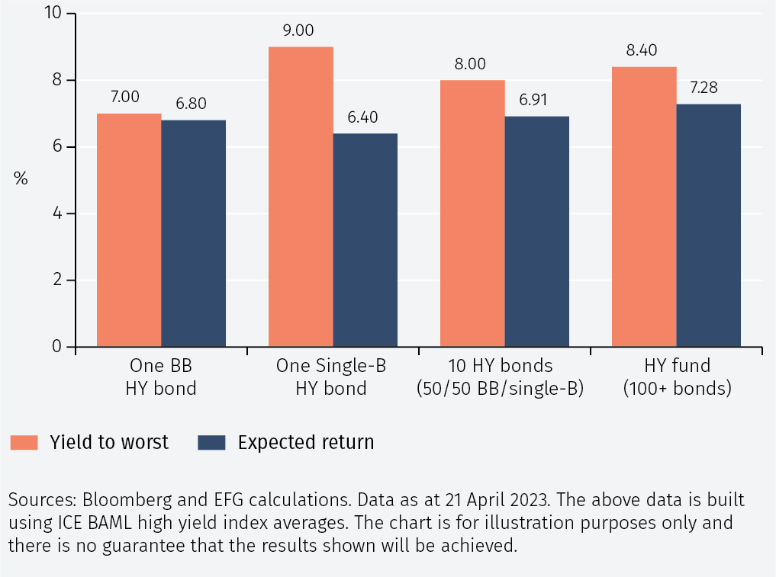

- The upside of any bond is limited (capped) to the yield.

- The expected return of any bonds will be lower due to the expected probability of a default event.

- A fund can add extra yield through investing in subordinated CCC bonds where the higher risk of these bonds can be managed.

- Bottom line: There is marginal to no difference in a concentrated bet within high yield versus a portfolio of high yield bonds.

- As the upside is limited and the downside is significant, by diversifying across more positions the risk/reward profile becomes increasingly attractive.

- Expected returns remain within a tight range, but the risk significantly falls as you diversify with more bonds (less weight per bond).

- Bottom line: With the improving risk/reward profile, when investing in high yield bonds it makes sense to invest in a diversified portfolio or fund of at least 100 bonds. As the minimum tradable amount of any bond purchase is usually greater than 100k, for an investor to build a diversified portfolio on their own they will typically need a portfolio of more than $10-15mn.

- In high yield, liquidity of any one bond varies over time due to a number of factors such as upcoming earnings and news events. By investing in high yield through a diversified portfolio or fund, short term liquidity needs are usually improved by spreading sales across a wider number of bonds.

- Typically, the lower the rating, the higher the cost to trade.

- If the bond becomes distressed the cost to trade can be as high as 5% and may take a number of weeks.

- Bottom line: A diversified portfolio or fund reduces the liquidity cost given closer market access, ability to time sales and ability to spread sales across bonds.

In summary, we think that it is essential to diversify in high yield as it a) increases risk/reward, b) minimises the negative impact of a default, c) allows for cheaper and faster market access/liquidity. An effective way to diversify is through a fund.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.