- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

For Professional, Accredited and Institutional Investors only.

The boom in artificial intelligence (AI) has been difficult to ignore, and there has been significant infrastructure spending. While Nvidia is the current poster child, beyond the company, there is an intricate supply chain and adjacent products vying to take advantage of the AI revolution. Jonathan Rawicz, Senior Portfolio Manager, and Henry Walters, Equity Analyst, explore their key considerations surrounding the ongoing infrastructure buildout and how they identify opportunities in the space.

Capex surge and semiconductor opportunity

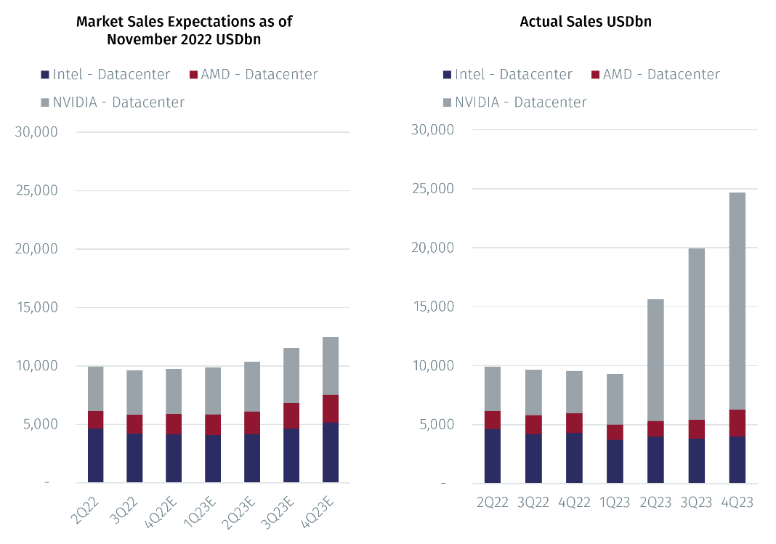

We are experiencing a significant capital expenditure boom in AI infrastructure, particularly on specialised AI chips. This surge has been fueled by the widespread adoption of tools like ChatGPT and growing optimism over the potential reach. Leading data centre chip providers have seen stellar sales growth, and AI spending has been a closely watched element of recent earnings reports. This boom comes amidst ongoing supply chain constraints, underlining the current imbalance between chip demand and production capacity.

Source: FactSet median sellside expectations.

Demand drivers: training and inference

Cloud service providers like AWS, Google Cloud, and Microsoft Azure are major consumers of AI chips, while the other half are accounted for by consumer internet businesses such as Meta and on-premise datacentres. These chips are primarily used for two purposes: training and inference. Training refers to the process of developing new AI models, which we see as an arms race where companies strive for larger and more powerful models. Inference involves using trained models for real-world applications, such as generating content with tools like ChatGPT or Dalle.

Identifying winners in the expanding value chain

The entire supply chain that feeds into AI chip production has seen a positive spillover effect. Furthest up the chain are silicon manufacturers, for example Shin Etsu Chemical and Entegris, producing and purifying silicon that goes into the chips. Foundries like TSMC, Samsung, and Intel, will then etch transistors onto the silicon. As competition intensifies, the question of whether TSMC will maintain leadership in the foundry space remains open. These foundries, in turn, rely on semiconductor equipment manufacturers such as ASML, Applied Materials, and Tokyo Electron to build the complex machinery needed for chip production.

Beyond the chain, adjacent products like server Original Design Manufacturers (ODMs) and networking companies have profited as data centres are built and equipped. Companies like Disco and BE Semiconductor Industries provide equipment for cutting silicon wafers and packaging finished chips, respectively. Testing equipment manufacturers such as Advantest and Teradyne ensure these chips function flawlessly.

Beyond Moore's Law

Pushing the boundaries of chip performance becomes increasingly challenging with each generation due to the limitations of physics. As Moore's Law (the prediction that the number of transistors on a microchip doubles roughly every two years) approaches its physical limits, the industry is exploring alternative solutions like advanced packaging techniques and the use of different compound materials to drive chip performance. A critical question for investors is the sustainability of this spending spree, drawing parallels with the huge overbuild of fiber networks during the dotcom bubble. Estimates vary widely, with AMD predicting a staggering $400 billion annual spend on AI chips alone by 2027. Others, like OpenAI chief executive Sam Altman, propose a range of $2-7 trillion to be invested in AI infrastructure. The question remains: how much will be invested and over what time horizon?

Investment scenarios: boom, plateau, or bust?

The future trajectory of this AI infrastructure buildout remains uncertain. Three potential scenarios exist:

1. AI usage explodes across various applications, driving continuous growth in AI chip demand.

2. Demand stabilises at a high level after an initial acceleration.

3. The application of AI fails to meet expectations, leading to a sharp decline in demand and a potential stock price correction.

A thriving ecosystem or winner-takes-all?

Irrespective of the outlook, currently, Nvidia dominates the AI chip market due to its unique capabilities. However, the question arises: can competitors like AMD or even tech giants like Google, Microsoft and Amazon successfully develop their own chips, potentially leading to commoditisation and price erosion? Nvidia's commitment to continuous innovation suggests a strong defence against the competition. However, a healthy competitive ecosystem could ultimately benefit the entire value chain, regardless of who emerges as the dominant player. The potential for significant market shifts and disruptions remains high in this rapidly evolving landscape.

Reference to securities is for illustration only and does not constitute a recommendation to buy, sell or take any other action. The above information should be viewed in a portfolio context.

New Capital Global Equity Conviction Fund

Learn moreImportant Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.