- Date:

- Author:

- Jaroslav Machalicky

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Following a decade-long rally, real estate assets came under intense scrutiny in 2022. In this edition of Infocus, real estate specialist Jaroslav Machalicky analyses the prospects for the asset class and finds long term potential amid short term headwinds.

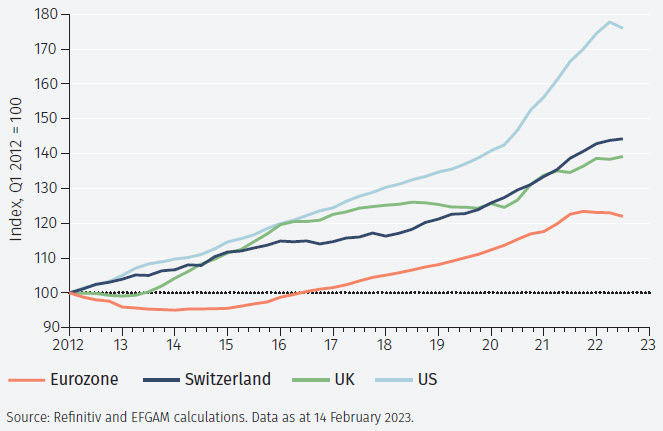

Real estate has been a popular asset class for many years, with commercial real estate (CRE) seen as offering stable and attractive returns.1 Over the past decade, land scarcity, demographic trends, low interest rates and attractive yields have driven up property values across a range of economies (see Figure 1).

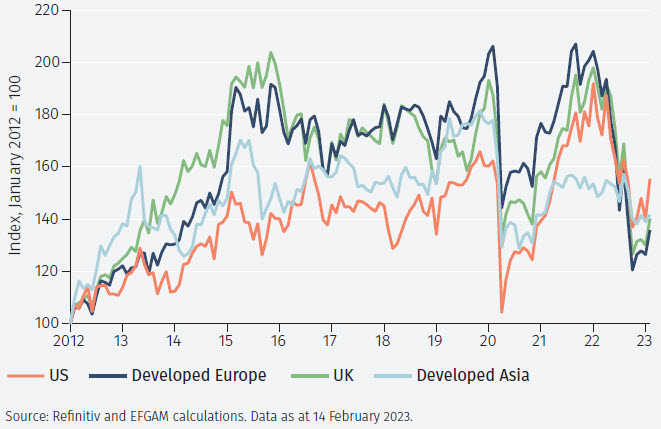

In 2022, however, a combination of rising inflation and rising interest rates led to a widespread fall in asset values, including real estate (see Figure 2).

Short term headwinds

Over the past 12 months, the average drop in property values in Europe and the US was 13%.2 Office, industrial and residential sectors suffered the most, though significant falls were also observed in the retail sector, which has struggled to recover from the impact of the pandemic. Over the same period, publicly traded real estate investment trusts (REITs), which are more volatile vehicles than their private counterparts, fell by at least 25%.3

CRE has for many years generated returns in excess of investment grade or high yield bonds of around 100-400 basis points per annum. Recent interest rate increases have left many CRE assets yielding less than an average high yield bond or resulted in an unattractive yield spread over investment grade bonds on a risk-adjusted basis. Spreads between US CRE yields and high yield bonds turned negative from the second quarter of 2022.

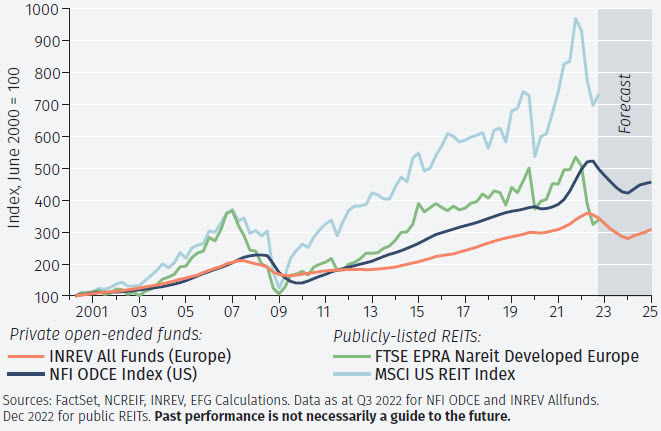

According to research, the entire CRE sector remains expensive relative to investment grade bond yields and public REITs.4 This provides room for further declines, with private CRE funds showing the most downside potential in our view (see Figure 3). We believe there is the possibility of a correction of 10-20% based on our assumptions, fund leverage and geographic and sector exposures.

Liquidity concerns

Just as financial markets in general are impacted by changes in interest rates and economic cycles, so too are real estate assets. This affects investors’ expectations and liquidity preferences.

The majority of CRE investments are made indirectly, by investing into public or private REITs, funds or companies. Easy transferability of ownership, stable income streams, inflation protection and portfolio diversification make indirect solutions popular.

Public real estate funds are more liquid than private funds and, consequently, more exposed to market volatility. Investors seeking liquidity favour public REITs over less liquid private transactions or private CRE funds.

2022 saw outflows from both public and private real estate vehicles. Withdrawal requests have been widespread, with USD 20 billion in requests from private core open-end CRE funds with USD 350 billion in assets by institutional investors at the end of 2022.5

In some private vehicles, there was a liquidity mismatch that resulted in difficulties meeting all redemption requests. As a result, some private CRE funds opted to put in place gates to limit investor outflows and avoid forced selling. For example, in November, an American private investment banking company limited withdrawals from its USD 69 billion net asset fund to USD 1.3 billion. As a result, only 43% of redemption requests were met during this period.6

Long-term sector views

As explained above, CRE faces short term headwinds. Despite this, there are many reasons to remain positive on the asset class over the longer run. Secular trends are providing asymmetric opportunities across sub-sectors with winners and losers set to emerge.

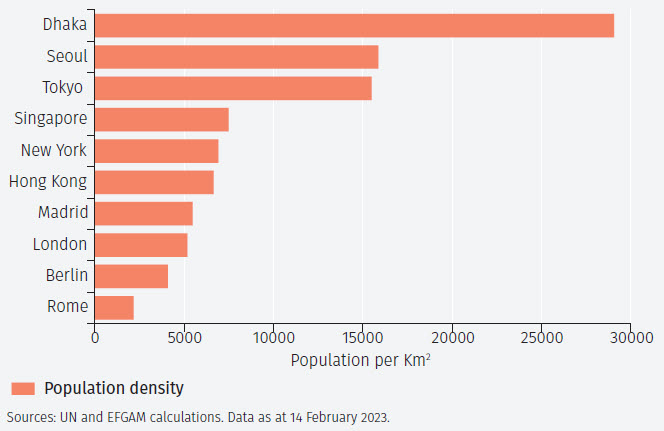

The largest sub-sector within CRE is office-related real estate. Hybrid working (a mix of office working and Working From Home – ‘WFH’) is the key challenge facing this sub-sector. This trend has been more pronounced in the US and Europe than in the Asia-Pacific region, where more densely populated cities and smaller apartment sizes support office work.7

Other challenges for the office sector include an ageing stock with large volumes of obsolete suburban office space and a high level of new supply. Furthermore the sub-sector faces high capital expenditure requirements compounded by the climate related spending needed to meet new emission standards.

The residential sector is better positioned for the medium to long term. While the WFH trend poses structural challenges to the office sector, the residential sector is a potential beneficiary, with growth expected in major urban centres, supported by accelerating urbanisation trends and lower capital expenditure requirements than for offices.

In addition, higher interest rates have reduced the affordability of home purchases, supporting rental demand. While there are signs of a stabilisation in rents, particularly in the US, demographic tailwinds continue to support demand for other areas of the residential sector, such as single-family, senior, affordable and student housing.9

The industrial sector, on the other hand, faces a high supply pipeline, lower demand through lower net absorption and an economic slowdown.10 However, ongoing urbanisation and changing consumer behaviour continue to support longer term trends such as the growth of e-commerce. This will boost demand for other segments of the sector such as warehouses, logistics and distribution centres.

We believe that the retail and hospitality sectors, which have not yet recovered from the pandemic, are facing similar headwinds. In general, retail centres in prime locations with strong grocery anchor tenants remain well supported for long term growth. The same is true for leisure-oriented hospitality in attractive locations.

Conclusions

Over the longer term, the historically stable and attractive returns profile of CRE means the asset class can play an important role in a balanced portfolio. Transformation of ageing CRE portfolios, capital expenditures to meet new ESG standards, secular trends, accelerating urbanisation and e-commerce growth provide structural support to the long term growth potential of certain CRE sectors.

The rise in inflation and tightening of monetary policy that occurred over the course of 2022 exposed some issues within the asset class. In the current context a further correction of interest-rate-sensitive assets such as CRE remains possible and the liquidity mis-match of the fund-based CRE market presents a headwind for investors. Therefore, the asset class may remain under scrutiny in the short-run over the gating of some vehicles and valuation concerns.

Exposure to structurally supported sectors through specific fund structures may still be appropriate for clients with a medium to long-term investment horizon. EFG has put in place a number of open-ended CRE vehicles that are actively managed and benefit from a dynamic allocation process. We believe that once the monetary policy tightening cycle is complete and the correction in the CRE market is over, allocation into CRE funds exposed to the right regions, sectors and themes, will resume. However, in the meantime investors should remain vigilant of current liquidity conditions.

1 Commercial real estate (CRE) refers to any large-scale real estate project or property. Sub-sectors include office, industrial, retail and residential. The main difference between the CRE residential sub-sector and residential properties is that CRE residential properties are primarily used to generate income whereas residential properties are primarily used as residences. For all CRE properties, the investment income is paramount.

2 Green Street (2023), CPPI index, https://www.greenstreet.com/insights/CPPI The index tracks individual property transactions.

3 FTSE EPRA Nareit Developed Europe index (-36.5%), MSCI US REIT index (-24.51%). A real estate investment trust (REIT) is a company that owns and, in most cases, operates income-producing real estate. Most REITs are traded on major stock exchanges and are referred to as public REITs. Public REITs are much larger in terms of assets than private REITs. Public REITs are mostly sector specific, while private REITs tend to be more sector diversified. Unlike direct property ownership, REITs are more diversified and generate greater economies of scale. Annualised volatility of European public REITs index (FTSE EPRA Nareit Developed Europe) was 21% and for the MSCI US REITs index it was 22%. The private European INREV ODCE index volatility annualised at 3.9% and the US counterpart, NFI ODCE, at 6.6%. All volatility was calculated from Q3 2000 to Q3 2022.

4 Time lag of valuations estimates: Green Street (2023), Janus Henderson (2022), Cohen & Steers (2011).

5 https://www.bloomberg.com/news/articles/2023-01-17/investors-seek-to-pull-20-billion-from-core-real-estate-funds#xj4y7vzkg

6 https://www.ft.com/content/e1ddc6f0-eb0a-4d52-8971-b1d9c2cb5c02

7 Hong Kong has a median per capita dwelling size of 172 square feet compared to 829 square feet in the US (Data from NIKKEI Asia and US census).

8 Cities are sorted by population and population densities are then calculated using data from the UN Demographic Yearbook 2021.

9 National Multifamily Housing Council, 2023 Rent Control Outlook 2023 (2022), Oxford Economics (10/2022), North American housing affordability takes a dive as mortgage rates spike; ECB, ECB Economic Bulletin, Issue 6/2022.

10 Net absorption is the sum of square feet that became physically occupied, minus the sum of square feet that became physically vacant during a specific period.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.