- Date:

Infocus - The pros and cons of cryptocurrency investment

The price of one bitcoin in US dollars quadrupled last year, gaining over 160% in Q4 alone. This meteoric rise sparked widespread media and investor interest in bitcoin specifically and in cryptocurrencies more generally. Moreover, many payment platforms such as BitPay, Square and PayPal have started accepting payments in bitcoin and other cryptocurrencies. At the same time it is becoming easier to trade cryptocurrencies on established platforms. This Infocus by Daniel Murray and Joaquin Thul sets out the pros and cons for investing in cryptocurrencies to help investors make a more informed decision about its prospects.

There is a lot of terminology associated with cryptocurrencies. To avoid confusion, definitions of some common terms are included in the Appendix.

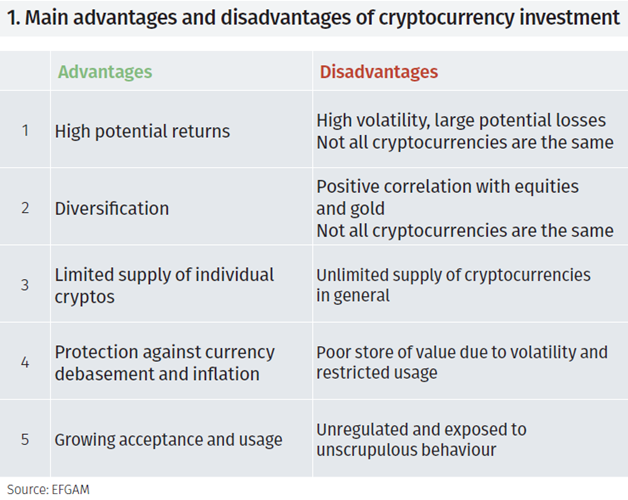

For convenience, Figure 1 sets out a summary of the main Advantages and Disadvantages of investing in cryptocurrencies as we see them. The main body of the text discusses each of these in more detail.

We start with some of the potential advantages.

Advantages

1. Potential for high returns

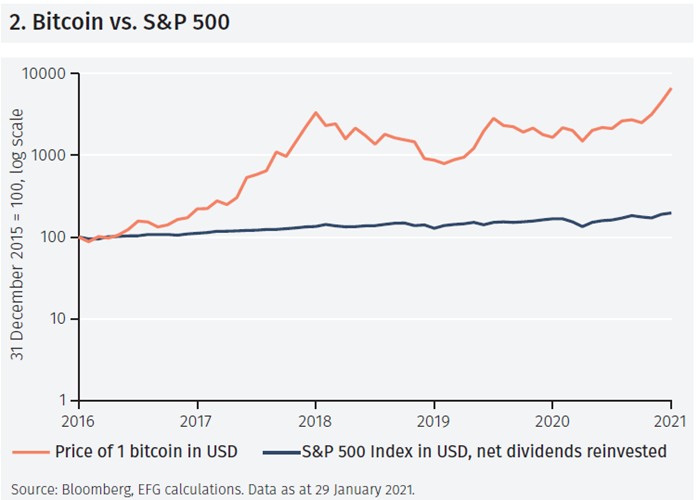

One of the main arguments in favour of cryptocurrencies is the potential for high returns. For example, in the five years to 31 December 2020, the S&P 500 index of large cap US equities has compounded at an annualised growth rate of 14.5% (in USD, net dividends reinvested); over the same time period the price of bitcoin in USD has compounded at an annualised growth rate of 131.5% (see Figure 2). The prospect of high returns becomes even more attractive in the context of very low government bond yields. Furthermore, high potential returns are appealing for those who believe equity returns will be lower for a while following strong performance last year.

2. Potential diversification

Diversification has also been mentioned as a potential benefit of investing in cryptocurrencies, with some saying it is an alternative to gold to use as a hedging tool in a portfolio context. For example, the S&P 500 declined in 17 out of the 60 months to end December 2020, of which the price of bitcoin rallied in seven. As noted above, a portfolio invested entirely in the S&P 500 (in USD, net dividends reinvested) would have generated compound annual returns of 14.5% in the five years to end 2020. A portfolio consisting of 10% invested in bitcoin and 90% in the S&P 500 would have generated compound annual returns of 26.8%. Moreover, the ratio of the compounded annual return to the annualised volatility– a simplified information ratio – rises from 0.95 for the S&P 500 on its own to 1.5 for the portfolio in which 10% was invested in bitcoin.

3. Limited supply

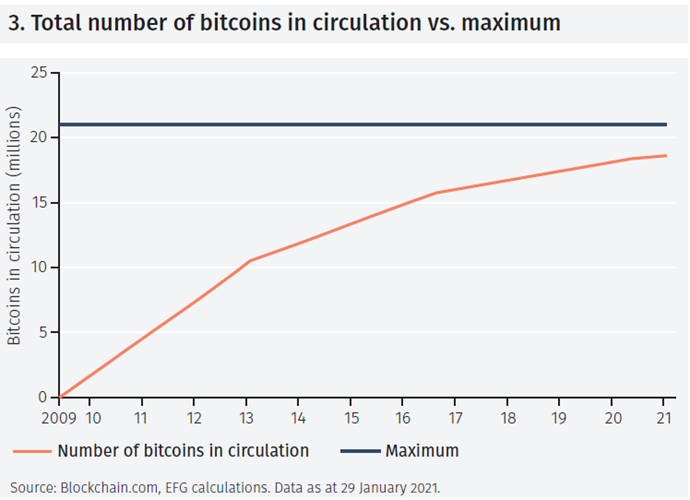

A particular feature of bitcoin is that there is a maximum of 21 million coins that can be created or “mined”. At the moment around 18.5 million bitcoins have been mined (see Figure 3), leaving less than three million still to come into existence. A related feature is that the rate of production of bitcoins slows over time via a process known as halving – every so often according to pre-determined conditions the number of bitcoins paid for mining a block halves. Whereas in 2009 each block mined was worth 50 bitcoins, the value is now 6.25 bitcoins per block following the latest halving in May 2020. Additionally, it is thought that around 20% of existing bitcoin supply has been lost or is inaccessible as a result of lost or forgotten passwords.1 The scarcity of bitcoin adds to its appeal for some investors – if demand for bitcoin increases further and supply is capped that would potentially drive the price higher. More generally, this supply-cap is a feature of many cryptocurrencies.

4. Protection from debased currencies and the threat of rising inflation

The Global Financial Crisis (GFC) of 2008/09 was a catalyst for central banks around the world to engage in unorthodox monetary policies, notably large scale asset purchases. For example, since the GFC began, the balance sheets of the US Federal Reserve and the ECB have each expanded by over US$6 trillion while the Bank of Japan’s balance sheet has expanded by a little less than US$6 trillion. Proportionately the Fed’s balance sheet has expanded by 8x, the ECB’s by a little under 4x and the BoJ’s by nearly 7x.

Some people are concerned this will result in a massive debasing of national currencies, as happened in the Weimar Republic in the 1920s when the mark became worthless.

According to people holding these views, bitcoin and other cryptocurrencies offer alternatives that cannot be debased in the same way, partly because supply is capped and partly because cryptos are not subject to the same political and economic pressures as national central banks e.g. central banks intervening in currency markets (such as the Bank of Japan and Swiss National Bank), central banks being obliged to support the economy during times of stress by purchasing government bonds. A corollary is that proponents of this view believe cryptocurrencies will provide much better protection against rising inflation. Such individuals find cryptocurrencies attractive precisely because they are insulated from government interference.

5. Growing acceptance and usage

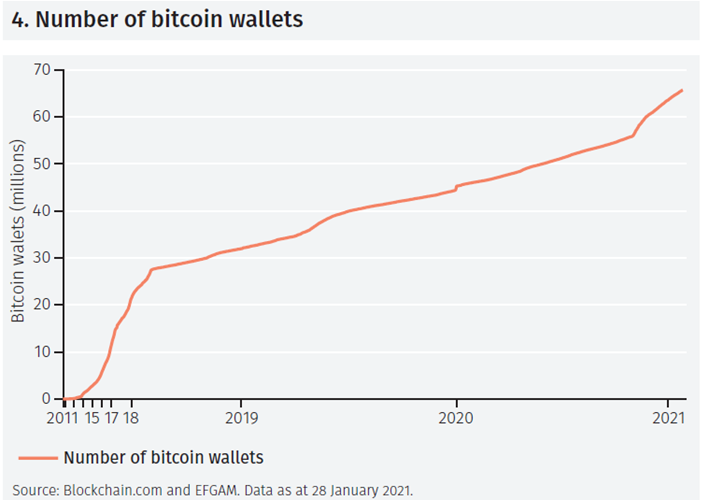

As noted in the introduction, a growing number of payment platforms are now allowing transactions to take place in bitcoin and other cryptocurrencies. An article from last year claimed that Coinbase had seen $135 billion in cryptocurrency merchant transactions in 2019, a 600% increase over 2018. That same article cites a Chainalysis report that alleges payment processors saw approximately $4 billion worth of bitcoin activity in 2019.2 Furthermore, another article quotes survey data that suggests at least a third of US small businesses accept cryptocurrencies as a means of payment.3 Separately, it is notable that there has been a significant increase in the number of bitcoin electronic wallets created over the past few years (see Figure 4) although it is impossible to know for what purposes they are being used. And there are an increasing number of institutional investors who are looking to invest in cryptocurrencies, the latest being Blackrock and Bridgewater. Grayscale Investments, a self-proclaimed “trusted authority in digital currency investing”, reported that in 2020, 86% of the $5.7 billion in inflows received into their products came from institutional investors, mostly asset managers.4

We now look at the disadvantages of cryptocurrency investment, many of which directly counter the advantages.

Disadvantages

1. High volatility and potential for large losses

The annualised volatility of the monthly percent change in the price of bitcoin in US dollars is about 90% as measured over the past five years. This compares to annualised volatility of the monthly percent changes in the S&P 500 and the gold price of 15.3% and 13.4% respectively. To give some idea of what this volatility might mean for an investor it is useful to consider the range of returns: the maximum monthly bitcoin return over the 60 months to end December 2020 was 76.1% and the minimum -37.6%. In addition it is worth noting that in 12 of those 60 months – 20% of the time – the monthly bitcoin return was worse than -10%. Whereas the S&P 500 generated negative returns in 17 of those months, the price of bitcoin fell in 25.

So investors need to be aware that the potential for large gains is offset to some extent by the possibility of large losses – the timing of an investment in bitcoin or other cryptocurrencies will have a significant bearing on the returns achieved. Indeed, on 11 January 2021, the UK’s Financial Conduct Authority issued a statement warning investors in cryptocurrencies that they should be prepared to lose all their money given the highly speculative characteristics of the asset class.5 Days later, ECB President Christine Lagarde also labelled bitcoin as a speculative asset, calling for central banks to regulate the cryptocurrency to prevent its use for money laundering activities.6 And India recently announced a plan to ban all private cryptocurrencies.

We further note that not all cryptocurrencies are the same. Whilst bitcoin and some other cryptocurrencies did indeed perform strongly last year, others did less well. For example, the cryptocurrency EOS is less well known and less widely traded than bitcoin but it is relatively large and well established, being one of the five cryptocurrencies that make up the Bloomberg Galaxy Crypto Index. In 2019 the USD value of EOS fell by 1.5% and in 2020 it declined by 0.2%. Crypto performance can and does vary significantly dependent on which version is selected.

2. Correlations

It was previously noted that of the 17 months the S&P 500 fell over the five years to end 2021, the price of bitcoin went up in seven. An alternative way of saying the same thing is that of the 17 months the S&P 500 declined, bitcoin also went down in 10 of them, which is slightly less flattering.7 Of the five worst months for the S&P 500 the price of bitcoin declined in four of them – one could argue that bitcoin has a poor record of providing diversification benefits when they are most needed.

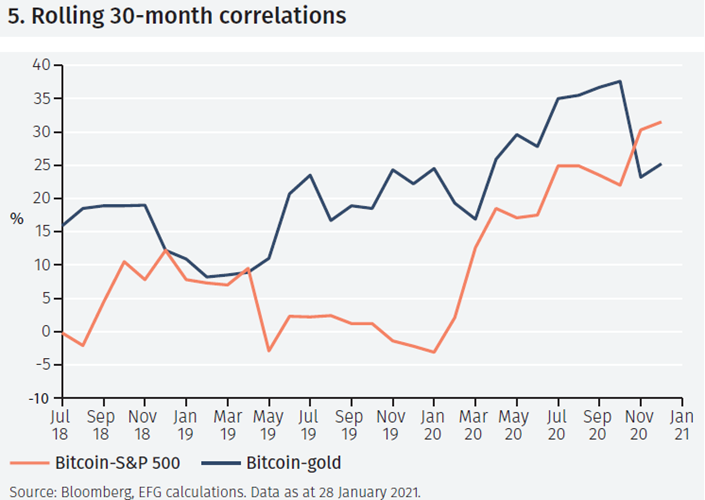

Moreover, changes in the price of bitcoin are positively correlated with changes in the S&P 500 index and to a greater extent than gold; the correlation coefficient between monthly % changes in the price of bitcoin and the S&P 500 index is 20.4% over the five years to end December 2020 whereas the correlation between monthly % changes in gold and the S&P 500 is 17.5%. And on a rolling basis there are times when the correlations between bitcoin and the S&P are even higher (see Figure 5). A final point to highlight in this regard is that, as with the returns achieved, the impact of owning a cryptocurrency in a portfolio will vary enormously dependent on which one is chosen.

3. Endless potential supply

Whilst it is true that the number of bitcoins produced will eventually be capped at 21 million and many other cryptocurrencies also have limited supply built into their protocols, there is currently nothing to stop an ever-growing number of new cryptocurrencies from being launched. Therefore, cryptocurrency supply is potentially limitless. Bitcoin is currently the favoured cryptocurrency but over time fashions and tastes may change, possibly very quickly and for no apparent reason. It is possible that once the bitcoin supply limit has been reached this will encourage flows into other cryptocurrencies, precipitating a fall from favour for bitcoin. This is not a prediction but merely identification of one way in which cryptocurrency market dynamics might change. It is also worth noting that several central banks are exploring the possibility of launching their own digital currencies, another potential catatlyst that may take the shine off privately managed versions.8

4. Poor store of value and limited acceptance

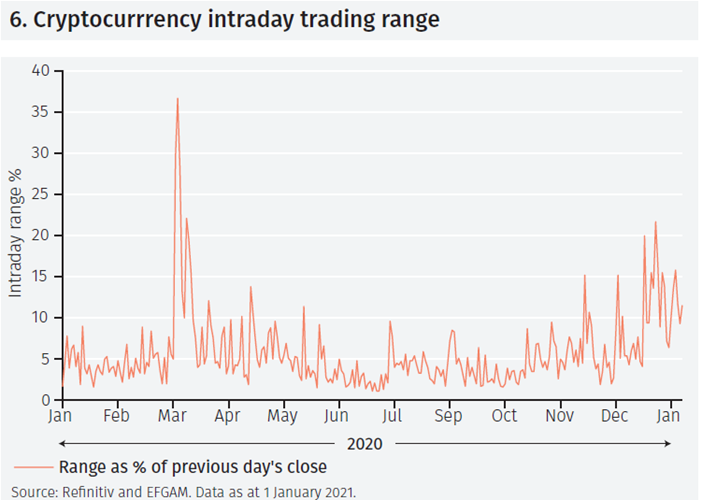

Whilst bitcoin and some other cryptocurrencies are now accepted across a growing number of payment platforms, the number of places where one can exchange cryptocurrencies for real goods or services is very limited. Other perhaps than in Venezuela, one cannot generally go into a coffee shop or restaurant (lockdown rules permitting) or other store and pay using a cryptocurrency – most places would not accept it. This is not least because cryptocurrencies are so volatile the revenue will vary wildly when converted back into a currency in which the merchant usually conducts business. The challenges here are compounded by the huge amount of intraday variation (see Figure 6). If a lot of people pay using cryptocurrency this may result in a large mismatch with the merchant’s cost structure.

For similar reasons the volatility inherent in cryptocurrencies makes them a poor store of value. The value of cryptocurrency savings when converted back into an individual’s base currency – that in which they conduct most of their transactions and in which their assets and liablities are expressed – will swing about wildly even on an intraday basis. This lack of stability reduces the attractiveness of cryptocurrencies as a store of wealth.

5. Unregulated and unbacked

Cryptocurrencies are a construct of the private sector with no official oversight or regulation. This means that cryptocurrencies are wide open to being exploited by criminals who in turn are able to use cryptos as a means to scam unwary investors. This is no doubt one reason why central banks and regulators are keen to get involved. There are of course perfectly legitimate ways and means of investing in cryptos but the lack of regulation makes them an attractive playground for less law-abiding members of society. A 2019 academic study found that 25% of bitcoin users are involved in illegal activity and that 46% of bitcoin transactions are associated with illegal activity.9

Whilst traditional financial systems and the currencies they use are certainly not faultless, they are at least heavily regulated. This not only deters criminal activity but it means that if there is a problem there are a set of rules (often embedded in law) and organisations in place to help deal with it. For example, most modern banking systems have some sort of deposit insurance in place, while credit and debit cards also typically provide a degree of insurance against fraudulent activity.

Furthermore, a country’s own currency has a special status as legal tender meaning that a creditor is legally obliged to accept it as payment for a debt. This fundamental characteristic underpins financial systems, augmented by monetary policy rules and trust in elected government. In contrast, because cryptocurrencies are not backed by anything other than faith in the system, damage to that faith will leave the cryptocurrency highly vulnerable.

There are already, according to Coinopsy, over 1,800 cryptocurrencies that have failed10 and there are other examples in history of private currencies having failed when trust was lost. In a 2019 presentation, St. Louis Fed President James Bullard noted that in the 1830s 90% of US money supply was represented by private currencies; he described it as “a state of affairs that has existed historically but was disliked and eventually replaced.”11 Markets also lose faith in traditional currencies when the monetary systems and governments stop functioning properly, such as recently occurred in Zimbabwe or Venezuela. However, this is highly unusual for countries with long established and stable monetary and political systems.

Conclusions

We have tried to identify the main advantages and disadvantages of investing in cryptocurrencies although we do not claim this list is exhaustive. Whilst we have no view on the direction of the price of bitcoin or any other cryptocurrency, we draw the reader’s attention in particular to the potential for large losses. Supporters of cryptocurrencies would argue that this downside risk is offset by the potential for large returns and that the risks can be managed by appropriately sizing a cryptocurrency position within a portfolio of other investments. The overall decision on whether or not to add cryptocurrency exposure to a portfolio is based on each individual’s assessment of the balance of advantages and disadvantages, the main ones of which we have tried to highlight in this note.

Separately and distinct from a discussion on the merits of investing in cryptocurrencies, we note that there are a number of potential advantages in utilising blockchain technology more broadly within the financial system. Perhaps paradoxically given the current lack of regulation of cryptos, blockchain could be a powerful regulatory tool, as noted in a recent BIS paper.12 Blockchain could also be used as a means of cost reduction to make the financial system more efficient. However, a broader discussion on the potential merits of blockchain is beyond the scope of this note.

Footnotes

1 ‘Lost passwords lock millionaires out of their bitcoin fortunes’, The New York Times, 14 January 2021. https://nyti.ms/3sgR63x

4 https://grayscale.co/insights/grayscale-q4-2020-digital-asset-investment-report/

7 This is an example of the behavioural framing bias in which the way information is presented has a significant bearing on how it is interpreted by the audience.

8 See EFG Infocus ‘The Surge of Central Bank Digital Currencies’, 7 January 2021.

9 ‘Sex, Drugs and Bitcoin: How Much Illegal Activity is Financed Through Cryptocurrencies?’ by Sean Foley, Joanthan R Karlsen and Tālis J Putniņš, Review of Financial Studies, vol 32(5), pages 1798-1853.

10 www.coinopsy.com/dead-coins

11 Public and private currency competition, James Bullard presentation, 19 July, 2019

https://www.stlouisfed.org/from-the-president/speeches-and-presentations/2019/public-and-private-currency-competition

12 ‘Stablecoins: risks, potential and regulation’ by Douglas Arner, Raphael Auer and Jon Frost, BIS Working Paper No. 905, Nov-20.

APPENDIX - DEFINITIONS

Digital currency is a loose term referring to electronic money that has no physical form. The definition is a bit woolly as many transactions and payments these days take place in electronic form, a trend that has been exacerbated by heightened concerns about physically handling cash in the midst of a pandemic. However, whereas it is possible to own notes and coins representing traditional currencies, a pure digital currency exists only electronically.

A cryptocurrency is a type of digital currency that is decentralised and operates on an independent platform – you don’t need to go through traditional intermediaries such as banks to trade or transact in a crypto. Cryptos are stored in a digital wallet (or similar) accessible only through electronic devices.

A digital token is a digital asset the value of which is tied explicitly to the value of another asset. A stablecoin is a particular type of token, the value of which is directly linked to a currency or a basket of currencies.

DLT is an acronym for Distributed Ledger Technology. In traditional models there are a small number of record keeping systems that are regularly reconciled and that serve as the official log of transactions and ownership. In an environment that uses DLT there is a decentralised system of records with no single authority over it. Blockchain is a type of DLT that verifies transaction and ownership information via a series of encrypted data blocks.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.