- Date:

Yield curve control

RISK FACTORS FOR EXCHANGE RATES

In this issue of Infocus, Stefan Gerlach looks at how a number of risk factors – capturing the state of the US economy; market participants’ views of risk and US monetary policy; and movements in oil and non-oil commodity prices – impact on the bilateral exchange rates of 36 countries to the US dollar.

Forecasting exchange rates is difficult. One important reason is that economic, financial and political news that influences exchange rates is itself difficult to forecast. For instance, unexpected political turbulence can mean that an expected appreciation of an exchange rate turns into an unexpected depreciation. Similarly, an unforeseen collapse of oil prices may mean that the currency of an oil importing country suddenly strengthens and that the currency of an oil exporting country weakens.

However, while forecasting exchange rates is difficult, investors often have views about how the global economy will develop. For instance, they may believe that oil prices will rise sharply, that the US term structure may flatten or that a recent increase in the VIX will be temporary. They may be interested in how these events will impact exchange rates. Forecasting of exchange rates conditional on such “risk factors” is much easier to undertake than traditional forecasting that makes no assumptions about future economic and financial conditions. Knowledge about how exchange rates are likely to respond to these drivers is also helpful in mitigating against an excessive accumulation of risk in a portfolio.

Preliminaries

Here the impact of eight such “risk factors” on 36 different bilateral exchange rates against the US dollar are studied. The selected risk factors are:

- The VIX (VIX).

- The spread between Moody’s Baa-Aaa corporate bond yields (Spread).

- The slope of US term structure as measured by the spread between 10-year yields and the federal funds rate (Slope).

- The US manufacturing ISM (ISM).

- Oil prices in US dollars (Oil).

- The prices of non-oil commodities in US dollars (Commodity).

- The US trade weighted exchange rate of the US dollar (USTW).

The exchange rates studied are those of Argentina, Australia, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Czechia, Denmark, Eurozone, Hong Kong,1 Hungary, Iceland, Indonesia, India, Israel, Japan, Korea, Malaysia, Mexico, Norway, Peru, Philippines, Poland, Romania, Russia, Serbia, Singapore, South Africa, Sweden, Switzerland, Thailand, Turkey and the UK.

While the exchange rates are all against the dollar, if the model suggests that currency A is expected to depreciate against the USD by 2% and some other currency B is expected to appreciate by 1% if some economic disturbance occurs, then currency A must be expected to depreciate by 3% against currency B. Thus, the estimates can be used to compute the effect on all exchange rate crosses.

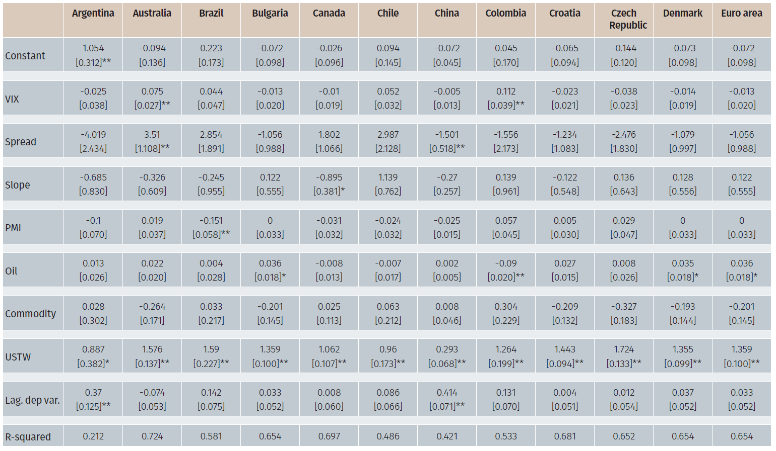

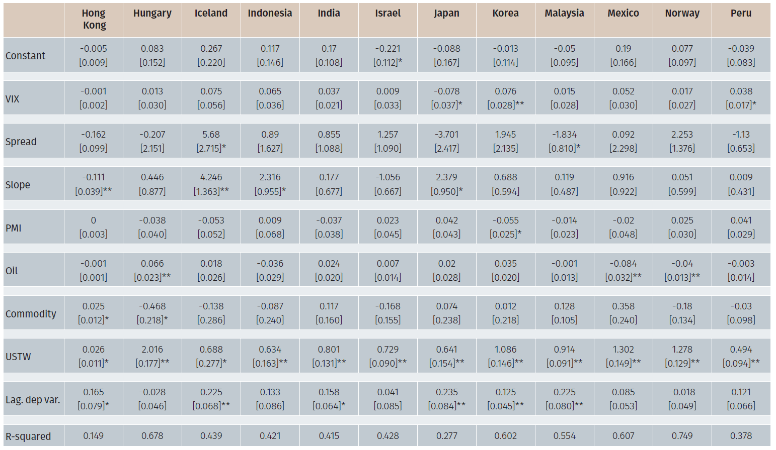

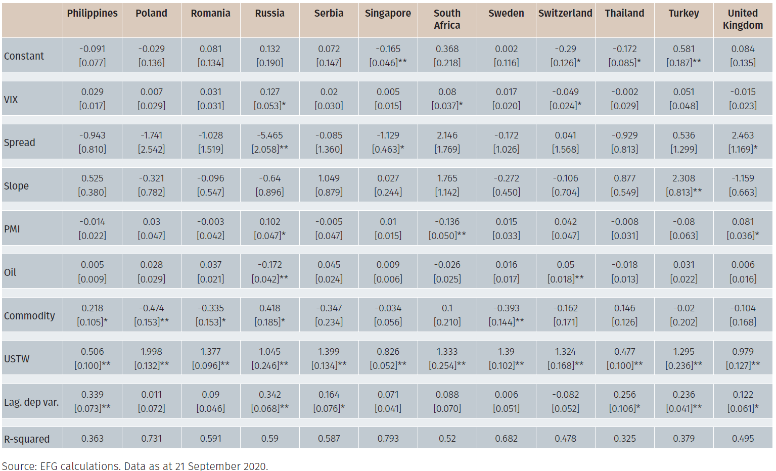

The impact of the risk factors on the exchange rates is obtained by regressing the change in the bilateral exchange rates on the changes in these risk factors using monthly data for the period February 2006 to June 2020.

Results

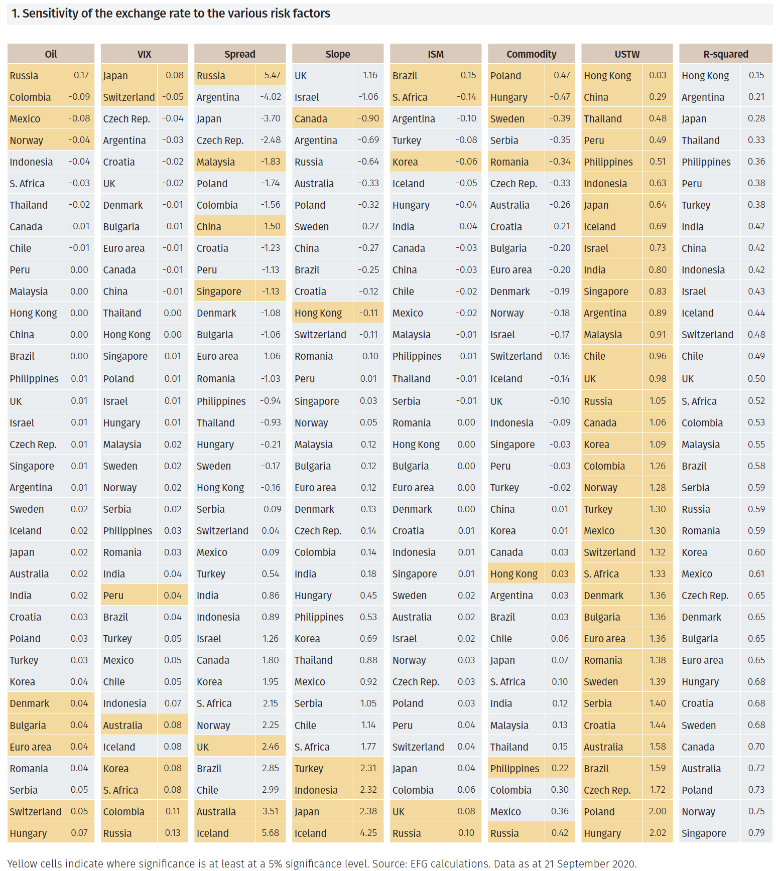

This section summarises the results (which are provided in detail in the Appendix) from the statistical analysis.2 In Table 2 the currencies are ordered according to how their exchange rate against the US dollar responds to a movement of the variable in question (a negative number shows that the currency appreciates against the USD).3 The yellow markings indicate that the effect is significant at least at a 5% significance level.

RISK FACTORS FOR EXCHANGE RATES

In interpreting the estimated parameters and the results below it should be kept in mind that these are partial effects, that is, they show the response of the exchange rate if only a single risk factor changes and the others are fixed. In practice, however, the various risk factors are strongly correlated. Indeed, the most important source of variation in these time series is an expansionary shock that simultaneously reduces the VIX, reduces the Baa-Aaa spread, leaves the slope of the term structure unaffected, raises the ISM, raises oil and commodity prices and appreciates the dollar.4

Furthermore, these relationships are best thought of as capturing the average correlation between the exchange rates and the risk factors in the sample period, February 2006 - June 2020. Such correlations are often unstable and sensitive to the occurrence of occasional extreme events.

The main results are:

⇒ Oil prices are significant for nine of the 36 currencies. The table shows that the Russian rouble appreciated by 0.17% in response to a 1 percentage increase in oil prices. The Colombian peso, the Mexican peso and the Norwegian krone all also appreciated sharply. Worst hit were the Hungarian forint, which depreciated by 0.07%, and the Swiss franc, which depreciated by 0.05%.

⇒ The VIX is significant in eight regressions. Table 2 shows that a 1 unit increase in the VIX led to an 0.08% appreciation of the yen and a 0.05% appreciation of the Swiss franc. This shows their importance as safe-haven currencies. Worst hit were the Russian rouble, which depreciated by 0.13%, and the Colombian peso, which depreciated by 0.11%. Large depreciations also occurred in the cases of the Icelandic krona, South African rand and South Korean won (all by about 0.08%).

⇒ The Moody’s Baa-Aaa spread is significant in seven cases. A 1 percentage point increase in it led, surprisingly, to an appreciation of the Russian rouble by 5.5% and the Argentine peso by 4.0%. By contrast, the Icelandic krona and the Australian dollar depreciated by 5.7% and 3.5%, respectively.

⇒ The slope of the US term structure is significant in six of 36 regressions. A 1 percentage point steepening of the term structure led to a 1.2% appreciation of sterling and a 1.1% appreciation of the Israeli shekel. Worst hit is the Icelandic krona, which depreciated by 4.2%, and the Japanese, Indonesian and Turkish currencies, which depreciated by a little more than 2%.

⇒ The US manufacturing ISM is significant in five regressions. A 1-point increase led to a 0.2% appreciation of the Brazilian real and a 0.1% appreciation of the South African rand but a 0.1% depreciation of UK sterling and the Russian rouble. A stronger US economy has two offsetting effects: raises the prospect of greater exports to the US but also higher interest rates as the Fed may decide to tighten monetary policy. Overall, emerging market currencies often appreciate – and developed market exchange rates often depreciate – against the dollar as the ISM increases.

⇒ Non-energy commodity prices are significant in seven regressions. A 1 percentage increase leads to 0.5% appreciation of the Polish zloty and Hungarian forint but a 0.4% depreciation of the Russian rouble and a 0.2% depreciation of the Philippine peso.

⇒ Finally, the last column shows the explanatory power of the models (as measured by the R-squared). While only 15% of the movements in the Hong Kong dollar (which is linked, but not rigidly so, to the US dollar by a currency board) are explained by the model, almost 80% of the movements in the exchange rate of the Singaporean dollar and 75% of the movements in the Norwegian krone are explained.

It must be emphasised that these estimates are not suitable for use as hedge ratios. First, they pertain to an historical time period and may be poor predictors of risk factors on the exchange rate in the future. Second, the estimates are subject to considerable uncertainty, implying that hedge ratios constructed from them are also imprecise. (Furthermore, in many instances the changes in the exchange rates in response to the risk factors are too small to be tradable.)

To see, consider an investor who would like to hold an fx position, but does not want it to be sensitive to a change in oil prices. Since the Norwegian krone appreciates by 4% in response to 1% increase in oil prices, and the Swiss franc depreciates by 5%, a position consisting of 1 Norwegian krone and –(4/5) Swiss francs or -0.8 Swiss francs would not change in value if oil prices changed by the amounts predicted by the analysis. Thus, it would be tempting to combine the currencies in a portfolio in this way. However, a 95% confidence band for the hedge ratio ranges from 0.01 to -1.58; assuming that it is precisely 0.8 is therefore risky.

Conclusions

Exchange rates tend to react in systematic ways to economic developments in the global and the US economies. Often these reactions are as one would expect. For instance, the yen and the Swiss franc both appreciate against the US dollar when the VIX rises; the Russian rouble appreciates when oil prices rise. Other reactions are perhaps less obvious: emerging market currencies generally appreciate – and developed market exchange rates generally depreciate – against the dollar as economic conditions, as captured by the ISM, improve.

While the estimates cannot directly be used for portfolio allocation, knowledge about the factors that drive exchange rates may be helpful in mitigating against an excessive accumulation of risk in a portfolio.

APPENDIX

Regression results, monthly data; February 2006 - June 2020

Standard errors in brackets; */** denotes significance at the 5%/1% level

Footnotes

1 The Hong Kong dollar is included since it can fluctuate within the band of 7.75-7.85 HKD per USD.

2 Since the prices of oil and commodities are denominated in US dollars, a nominal effective exchange rate index for the dollar is also incorporated in the regression, as is a lagged dependent variable to capture any dynamics.

3 To emphasise that an exchange rate is a price (but for one unit of foreign currency and not for a good), economists often quote exchange rates in the same way as other prices. Thus, this convention, which differs from market practice, is used here. (To illustrate, the exchange rate for the Swiss franc is 0.90 CHF for 1 USD and for the UK sterling it is 0.76 £ for 1 USD).

4 This may explain the surprising results for the Russian rouble, for which the full estimates suggest that it will appreciate in response to a higher Baa-Aaa spread but depreciate in response to higher commodity prices. The bivariate correlations suggest that a stronger rouble is associate with a smaller spread and higher commodity prices.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

Please use the button below to download the full article.