- Date:

Infocus - The outlook for the Portuguese economy is good. With a low unemployment rate, political uncertainty resolved by the recent elections and with fiscal transfers from the EU, at the beginning of the year growth was forecast to be strong. That said, the underlying weaknesses of the Portuguese economy remain. Productivity is low, investment is low, there is an educational deficit and public debt is high. In this issue of Infocus, EFG chief economist Stefan Gerlach and senior economist GianLuigi Mandruzzato take a closer look.

The outlook for the Portuguese economy is good. With a low unemployment rate, political uncertainty resolved by the recent elections and with fiscal transfers from the EU, at the beginning of the year growth was forecast to be strong. While the effects of the Russian invasion of Ukraine and the associated economic sanctions will unavoidably lower growth, chances are that Portugal will not be severely affected. That said, the underlying weaknesses of the Portuguese economy remain. Productivity is low, investment is low, there is an educational deficit and public debt is high. In this issue of Infocus, EFG chief economist Stefan Gerlach and senior economist GianLuigi Mandruzzato take a closer look.

Portugal has returned to growth

After real GDP collapsed by 8.4% in 2020, growth rebounded strongly in 2021 when real GDP expanded by 4.9%, the highest rate in almost three decades. Before the eruption of the Ukraine crisis, the EU Commission had forecast that real GDP would exceed the pre-pandemic level later this year.

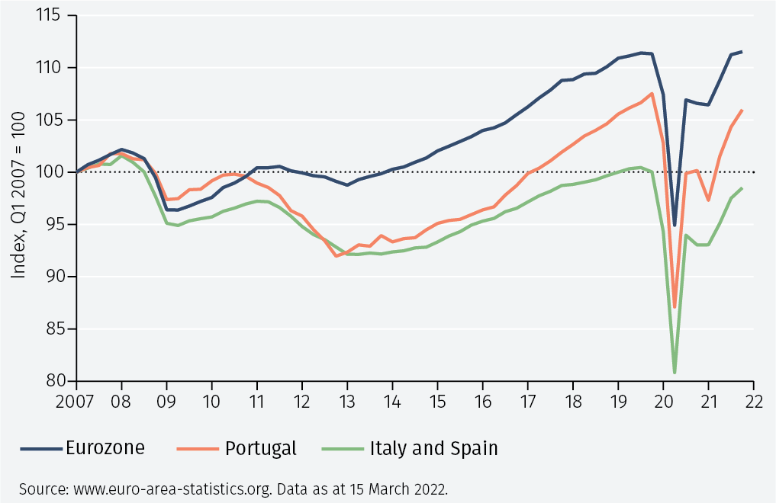

Looking at the longer period since 2007 provides a broader perspective of developments in the Portuguese economy. Real GDP evolved in broadly similar ways to the eurozone average until 2010. Between 2011 and 2015, during the eurozone sovereign debt crisis, GDP lagged the eurozone average but performed in a broadly similar way to the comparator countries Italy and Spain.1 Finally, between 2016 and the start of the Covid pandemic in early 2020, Portuguese GDP grew strongly.

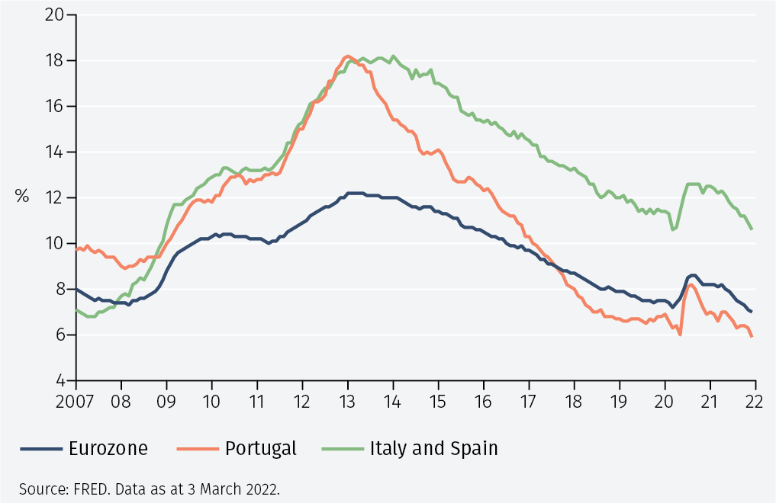

In turn, this has led to a sharp fall in the unemployment rate. Because of the Global Financial Crisis that started in 2008, the subsequent fiscal crisis and the ensuing austerity, the unemployment rate rose sharply in Portugal until the middle of 2013 in much the same way as in Italy and Spain. It then started to decline rapidly, falling first below the unemployment rate in Italy and Spain and then below the eurozone unemployment rate in 2017. The unemployment rate shot up during the Covid pandemic but remained below that of the eurozone and much below the elevated rates in Italy and Spain. With an unemployment rate of 5.9%, which is below the level before the pandemic, the outlook for Portugal looked good before the Russian attack on Ukraine.

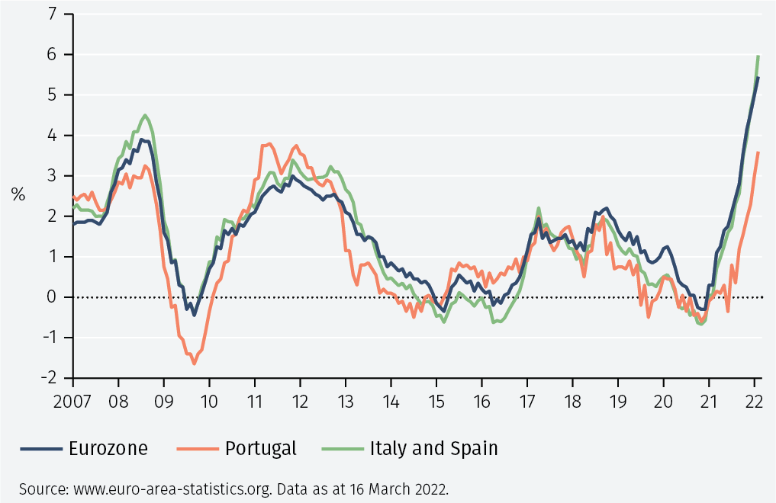

The behaviour of inflation also shows how much progress the Portuguese economy has made since 2013. While inflation in the eurozone has averaged 1.0% since the middle of 2013, it has averaged 0.6% in Portugal and 0.7% in Italy and Spain. Over the last 15 years, this has given Portugal a 6% improvement in relative prices. Nevertheless, there is a clear risk that in 2022 Portuguese inflation will exceed 4% and that it will be much closer to the rate in the eurozone than previously expected.

Vaccination and tourism

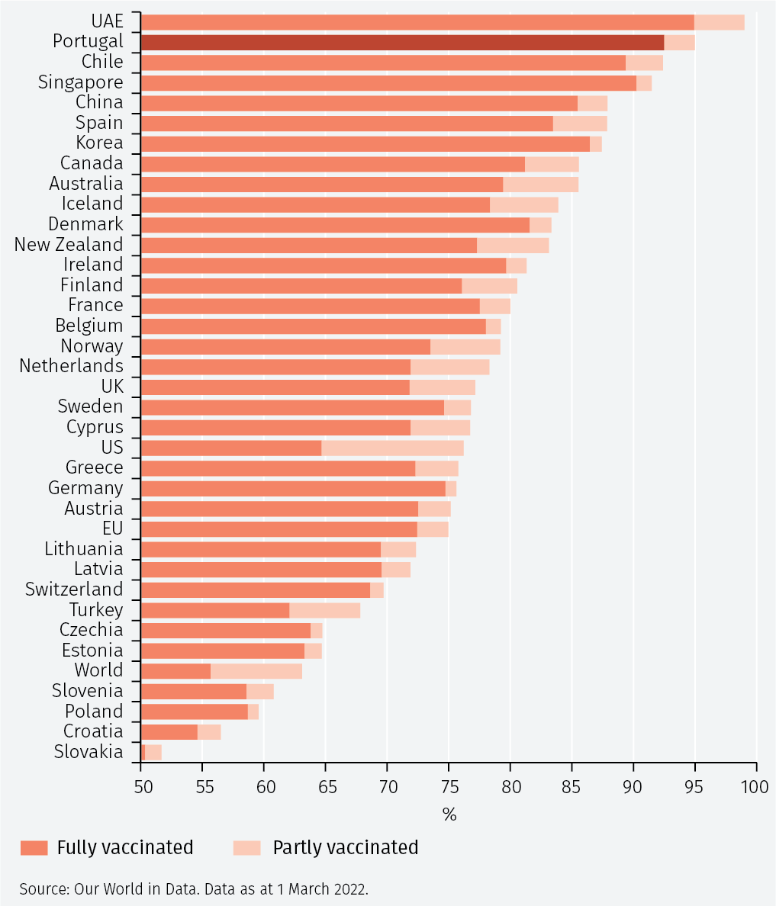

The strong recent performance of the Portuguese economy partially reflects the government’s extremely successful vaccination campaign, which has resulted in one of the world's highest rates (see Figure 4).

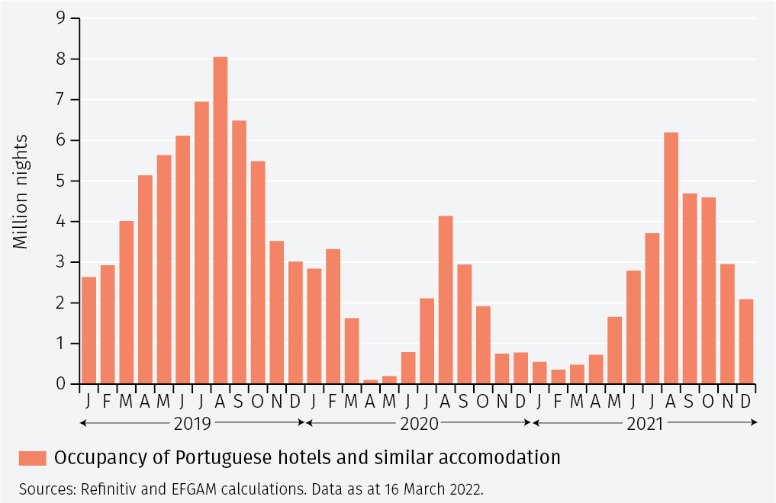

The favourable growth outlook is also linked to the expected recovery in tourism, a sector that in 2019 represented 17% of Portugal’s GDP according to the World Travel and Tourism Council. The gradual loosening of Covid restrictions will attract an increasing number of tourists, further supporting recovery from the depressed levels of the last two years (see Figure 5). Despite the recovery that began in the spring of 2021, the second half of that year saw occupancy rates some 25% lower than in the same period of 2019.

Activity will also benefit from the large inflows of EU funds in coming years. Portugal has requested grants and loans under the Recovery and Resilience Plan (RRP) worth 8.2% of 2020 GDP. After receiving a disbursement of €2.2 billion last summer, it is estimated that GDP growth will be raised by between 0.5% and 1% per annum until 2025. Furthermore, the full implementation of structural reform projects under the Recovery and Resilience Plan will raise the economic growth potential, boosting public debt sustainability.

The likelihood of a swift implementation of the structural reform plan was improved by the unexpected result of January’s snap elections. The Socialist Party of the incumbent Prime Minister, António Costa, won an outright majority in the Assembly of the Republic with 118 seats out of 230. The prospect of a stable government for the four years of the legislative term is another positive factor underpinning the outlook for the Portuguese economy.

Fiscal policy and energy policy

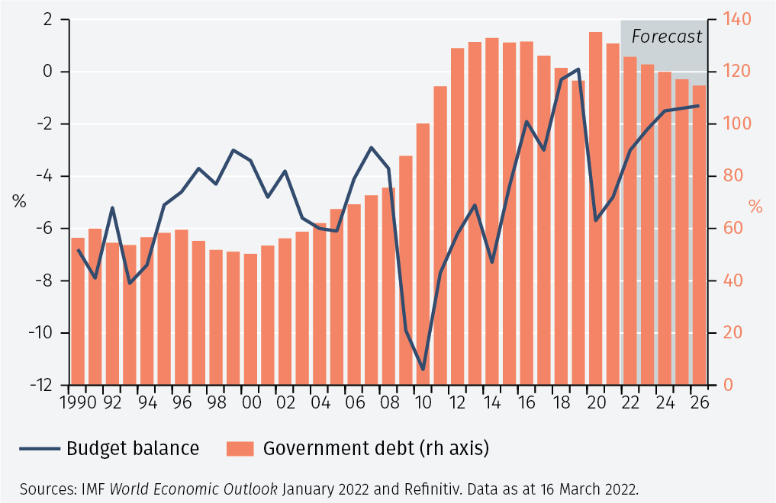

An unfortunate legacy of the pandemic is the high public debt burden, which rose to 135% of GDP at the end of 2020, almost 20 percentage points higher than a year before (see Figure 6).

However, strong GDP growth and prudent fiscal policies implemented by the government before the election have helped the debt-to-GDP ratio to fall below 130%. According to international institutions, including the EU Commission, the IMF and rating agencies, by 2024 the debt-to-GDP ratio will have returned to its level before the pandemic.

The Russian invasion of Ukraine has led the favourable forecasts made at the beginning of the year to be revised down. There is particular concern that large increases in energy and food prices will curb household purchasing power, slowing growth. These two items account for more than 30% of the total expenditure of Portuguese households, which is substantially higher than the median of the other eurozone countries.

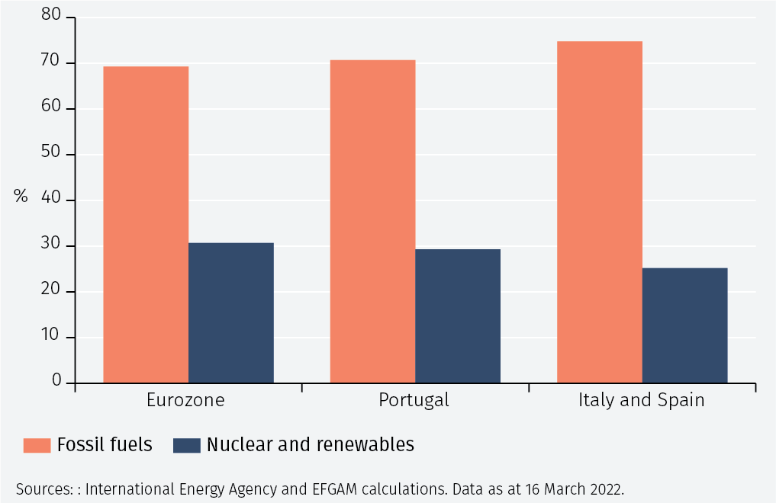

With a mix of energy sources still biased towards fossil fuels (Figure 7), Portugal depends on imports for more than 70% of its energy needs. The events of the last few weeks have highlighted the importance of the security and affordability of energy supplies to protect the economy. It is therefore important that the recently launched reforms of the energy sector are fully implemented. Between 2010 and 2020, national energy consumption was reduced by 15% and the share produced from renewable sources increased by 5 percentage points. The resources of the RRP will support investments aimed at achieving carbon neutrality, targeting the manufacturing, transport and building sectors.

Productivity, education and investment

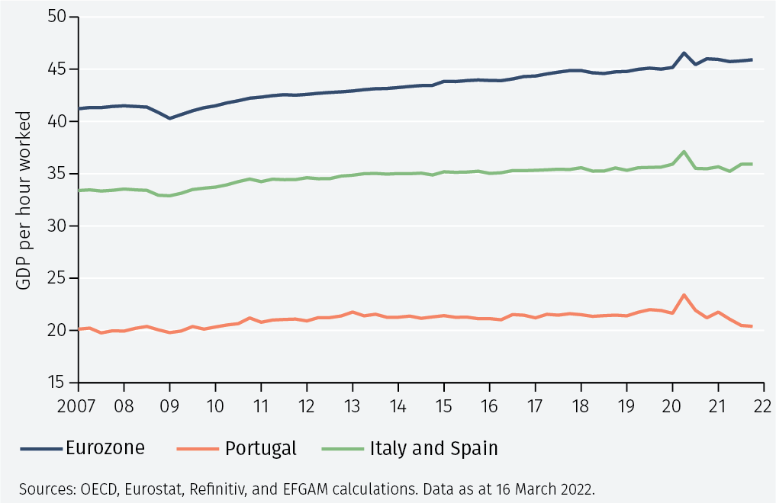

While the Portuguese economy is doing well, from a long-term perspective it is threatened by three factors. The first of these is the low level of productivity. Figure 8 shows that GDP per hour worked is only 40% of that in the eurozone and about 60% of that in Italy and Spain.

Productivity translates over time to higher real wages and stronger economic activity and, therefore, to healthier public finances. Seeking to boost productivity and raise Portugal’s economic potential must therefore be high on the policy agenda.

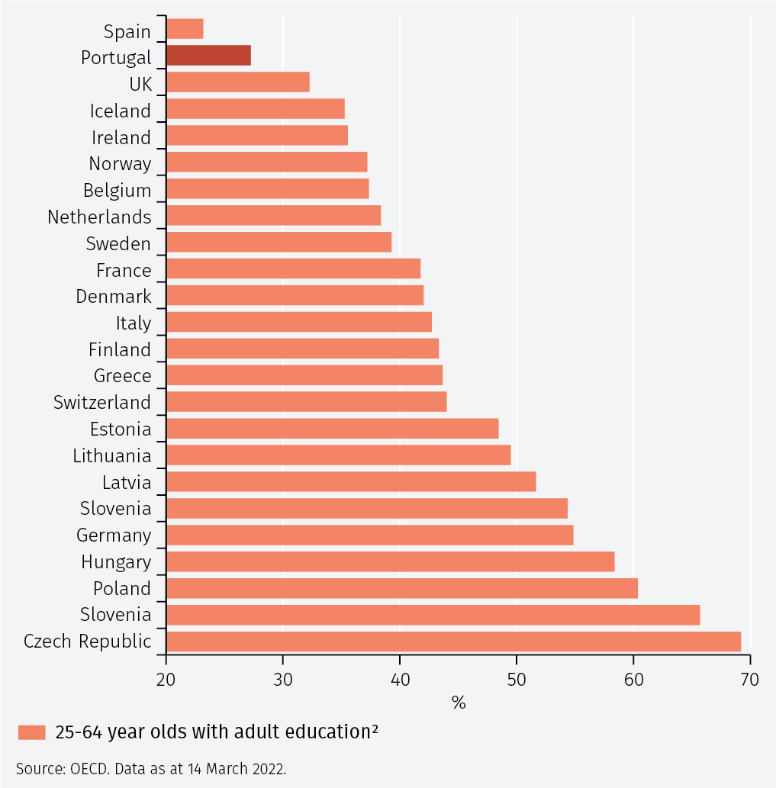

One factor that helps explain the productivity deficit is the average level of education of the labour force, which is low in Portugal. Figure 9 shows the fraction of the labour force that has completed upper secondary education for Portugal and other European countries. This is another area in which policy interventions will be important to raise incomes and economic activity.

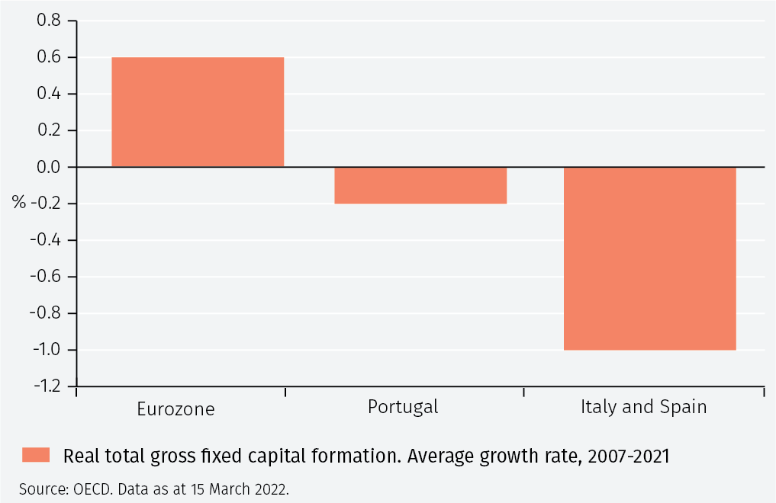

A second factor that affects productivity is investment. Figure 10 shows that while eurozone fixed capital formation grew by an average of 0.6% p.a. over the period 2007-2021, it contracted by 0.2% p.a. in Portugal and by 1.0% p.a. in Italy and Spain.

While this shows again that economic developments in Portugal have been stronger than in Italy and Spain, plainly a contracting capital stock is not compatible with growth and a rising standard of living.

Conclusion

While being severely hit by the Global Financial Crisis and the subsequent fiscal crisis in the eurozone, Portugal has made excellent progress in returning to growth. However, challenges remain. The short-term outlook is clouded by the uncertainty stemming from the global macroeconomic repercussions of the Russian attack on Ukraine. In the longer-run, the economy faces serious structural long-term issues related to low productivity, low educational attainment and too little investment. Overcoming these difficulties should be on top of the government’s policy agenda.

1 To avoid cluttering the figures, a weighted average of Italy and Spain is used, with the weights given by their relative ECB capital key (59% weight on Italy and 41% on Spain).

2 Percentage of 25-64 years olds that have completed upper secondary education. Upper secondary education typically follows completion of lower secondary schooling.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.