- Date:

Inview June 2021

Editorial

Welcome to the June edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

With equity markets rising to new highs, investors seem increasingly confident the pandemic is on the way to being defeated by vaccination programs of growing size and geographic reach. It is easy to lose sight of the fact that while plenty of progress has been made in the OECD economies, the situation is different – in some countries radically different – for many emerging economies. The resurgence of new cases in South-East Asia and the still high number of new cases in South America suggest that the downside risks remain, and that it is too early to conclude that the pandemic is slowly fading.

A second issue that is coming increasingly to the fore is the Fed’s decision about when to taper bond purchases. This is an issue that will have huge repercussions for the global economy since economic conditions in the US are stronger than those elsewhere, particularly in the euro zone. An announcement that tapering will start in 6- or 12-months’ time is likely to lead to rising long term bond yields in the US and a strengthening of the US dollar, which will have implications for inflation, economic activity, and monetary policy outside of the US.

The Fed appears to believe that the current uptick in inflation is likely to be temporary and largely reflects the outright falls in the price level that occurred as Covid struck last spring. However, the monthly inflation rates for both March and April, which are not affected by last year’s developments, were both surprisingly strong. This raises the risk that inflation may be rising more rapidly than the Fed has anticipated. Investors worry that the Fed may be underestimating the strength of inflation and that it at some stage will recognise that this is the case and engage in a dramatic policy tightening. If so, it could have a disproportionate effect on the pricing of a range of financial assets.

Government bonds seem most at risk. Their yields could rise, and their price fall, also because of the increase in government debt that will follow from Biden’s fiscal plans. The recently announced budget for 2022, together with other large spending packages presented in the first months of the new Administration, is expected to push US public debt to almost 120% of GDP in the next ten years. Bond vigilantes do not seem worried by this perspective, judging from the low level of US bond yields, but it would be surprising if the latter fell further.

On this account, in our view, a diversified portfolio should favour equities over bonds, with a preference for US and UK markets where the vaccination plans are more advanced. With respect to styles, large caps exposure should be reduced in favour of smaller capitalisations and value stocks. Within fixed income, the low level of yields advises for seeking returns in hybrids and convertible bonds, accepting some additional volatility. Finally, to hedge against the risk of inflation at least partially, exposure to real assets, including infrastructure, gold and industrial metals looks appropriate.

Global Asset Allocation: Summary

Equities

- Fears over a potential break-up in Europe after Brexit have faded, strength in the auto sector and the region’s leadership in renewable energy policies bolster the case for European equities. The region has continued its bounce and we could look to adjust our current neutral positioning over the coming months.

- Recently we upgraded our tactical UK equity positioning to overweight as the vaccination campaign continues and more restrictions are lifted, setting the economy up for a rebound.

- Maintaining our overweight in Japan has been costly recently but we remain optimistic on the country’s long term prospects.

- The outbreak of Covid in India has paused the market's ascent, but this looks to be a consolidation. The ASEAN markets remain underweight for us, while we are still positive on China where we are seeing upward revisions of earnings.

- There continues to be political tensions within Latin America, making any meaningful policy changes more difficult to pass. Relative caution is warranted within the region.

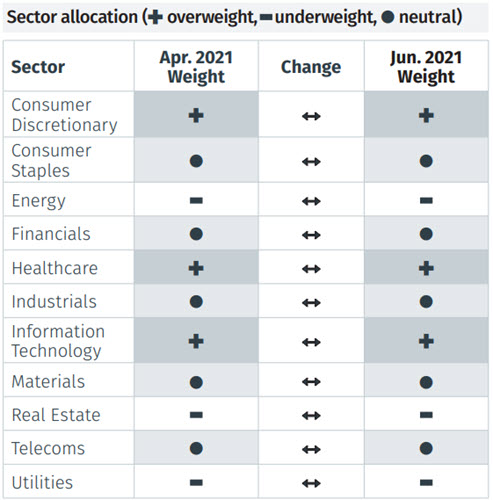

- There are no changes this month to our sector preferences. One notable point is that despite the big move in energy the sector has not shown relative momentum just yet.

Fixed Income

- We have strong bias for China renminbi bonds as yields are higher with a strengthening currency. We are neutral on emerging markets overall, given the balance of macro conditions, left wing political bias and tight spreads.

- Convertible bonds have lost some ground recently but are still performing well year-to-date relative to other areas of fixed income, so we continue to have an overweight position.

- During the last month Treasury yields and corporate spreads have stabilised, consistent with our view that the recent rally was a normalisation of previous conditions.

Alternative Investments

- We are upgrading infrastructure to overweight both strategically and tactically. Developing infrastructure plans in the US and Europe as well as the defensive nature of this asset class against inflation gives us confidence to upgrade.

- There is positivity on event-driven merger arbitrage and relative value convertible arbitrage strategies which could benefit from strong corporate activity. Equity and macro managers have benefitted from higher dispersion of markets across regions, sectors and factors, creating alpha opportunities.

Currencies

- We are upgrading the pound on a tactical basis from neutral to overweight, while holding a neutral strategic view. In our view the pound looks strong and short-term technicals show it might break higher from the range versus the US dollar

- The US dollar has weakened in line with rate differentials. We expect this trend to continue for the time being and remain tactically underweight. At the same time Europe is catching up on vaccine roll-outs and economic confidence is returning

- Strategically we are neutral on Asia currencies overall but remain cautious on the Japanese yen and maintain our preference for the Chinese renminbi.

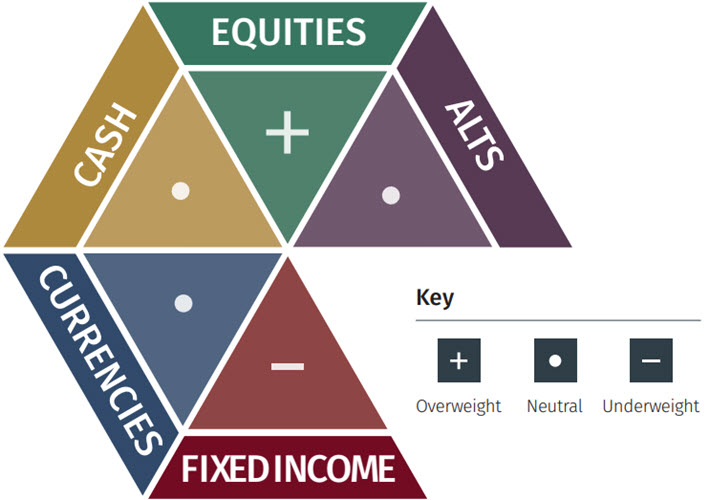

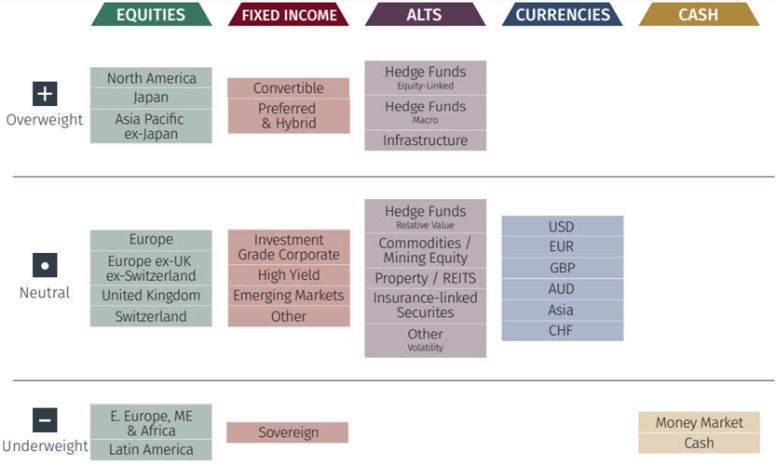

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breakdown

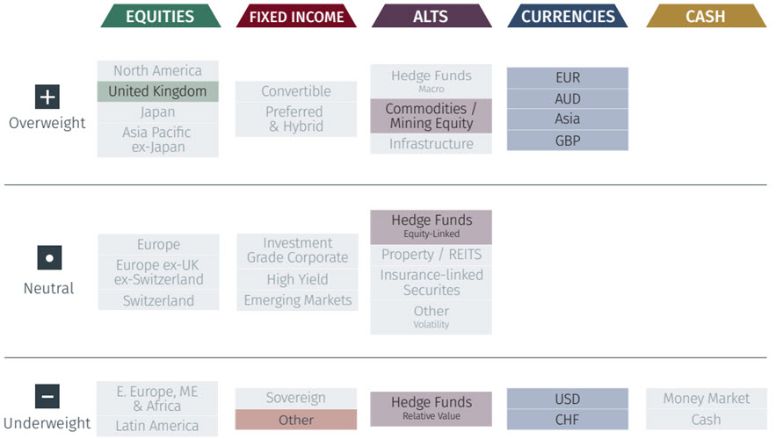

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.