- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

The search for a new equilibrium will, we think, be a key theme for the remainder of 2023. In economies, that search relates to growth and inflation. In financial markets, it entails finding sustainable bond yields.

Growth: the search for stability

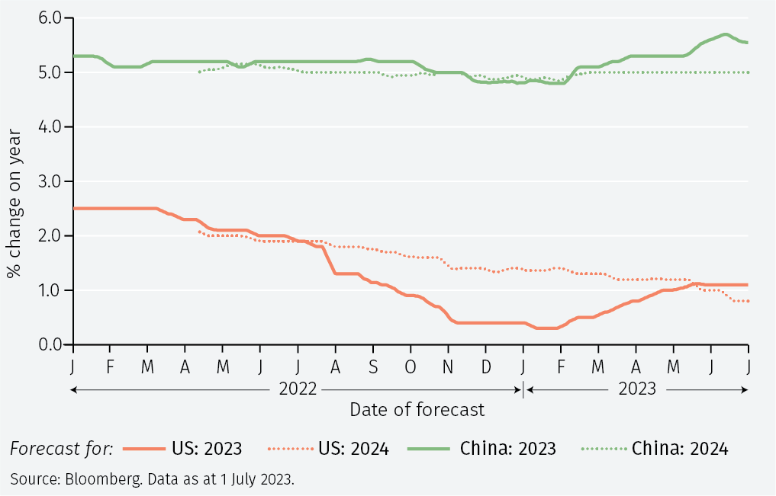

Pre-Covid, the pattern of global growth was relatively stable. Certainly, after the Covid-era gyrations, that is how it seems in retrospect. In the five years 2015-2019, global growth was around 4% p.a. China (with a rate around 6-6.5% p.a.) led the developing economies; the US (around 2-2.5% p.a.) led the advanced economies. In both, however, demographic and productivity trends argued for some steady slowing of growth in the future. If that is a reasonable view of the long-term picture, consensus forecasts for this year and next (see Figure 1) suggest we may be close to those equilibrium levels.

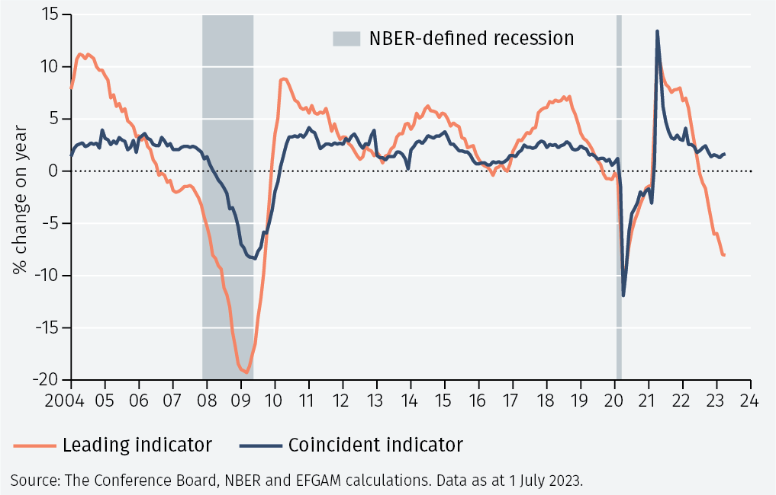

But there are reasons for doubt. In the US, coincident indicators still show strength in the economy but leading indicators (see Figure 2) suggest weakness. In particular, the inverted yield curve signals a recession may well materialise later this year. Across all advanced economies, core inflation remains sticky and the lagged effects of higher interest rates are yet to be fully seen.

In China, doubts around growth surround the fact that short-term indicators – retail sales, industrial production and those relating to housing – are softer than hoped for earlier in the year. The youth unemployment rate has risen to 20% - a development redolent of the eurozone peripheral economies in their crises ten years ago. More policy stimulus in China will, we expect, be forthcoming. But if there is one lesson from the Global Financial Crisis that is relevant to China it is that cutting interest rates and easing monetary conditions are less effective when the banking system is not functioning properly and the private sector has borrowed heavily. That, unfortunately, seems to be the picture in the Chinese economy. Adding to those concerns are adverse demographics, poor relations with the US and questions over the conduct of policy (especially after the rapid retreat from zero Covid). Some see this combination as so adverse that China is ‘uninvestable’. The obvious corollary is that it is still a strongly growing economy, with undoubtedly high competitiveness in many sectors and an equity market that is not expensively valued. That tension between the key issues is not likely to be resolved this year or next.

US-China; advanced-developing worlds

The position of the US and China as leaders of their respective advanced and developing economy universes is also in question. Japan’s economic and corporate renaissance continues; Europe’s strengths (in technology and innovation) are most likely underappreciated; and the peripheral eurozone economies are a source of dynamism. US dominance can be questioned.

In the emerging economies, India has overtaken China as the world’s most populous economy. It has a younger demographic profile and is clearly providing an alternative to China as a manufacturing centre, building on its strength in business services. The Gulf economies have the financial resources for substantial green infrastructure development. Economies in Africa and Latin America are able to provide the raw materials for that transition and several are strong in their own right: Chile as a leader in clean energy, for example. This potential for a multi-decade transformation of the global economic landscape is huge.

Across the developed and emerging markets, however, the near-term attention is still on inflation and policy.

Inflation: the sticky core

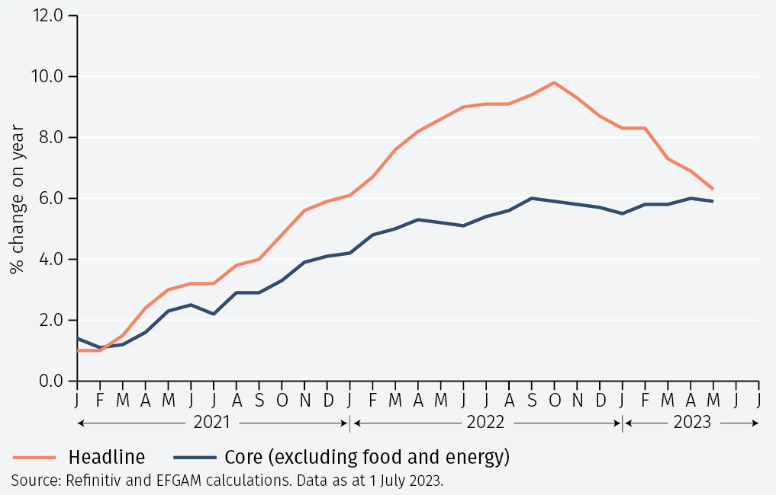

In the US, as in other advanced economies, headline inflation rates have declined but core inflation remains sticky (see Figure 3). One common reason for higher core inflation is stronger wage growth. But when the messaging around inflation control starts to emphasise wage restraint, the former technocratic success of central bank inflation targeting enters a messier political arena.

The good news is that longer-term inflation expectations (see Figure 4) have stabilised – suggesting that some new equilibrium has been found. And in the US, we seem to be nearing the peak in policy interest rates. There, and to some extent elsewhere, there is some acceptance of the case for waiting to assess the lagged effects of previous tightening. China should not be forgotten in this respect. It has no inflation problem – the headline and core inflation rates are close to zero. For many years it was the exporter of deflation to the rest of world. The ‘China price’ was the global phenomenon moderating global inflation. That may well happen again.

Policy rate games

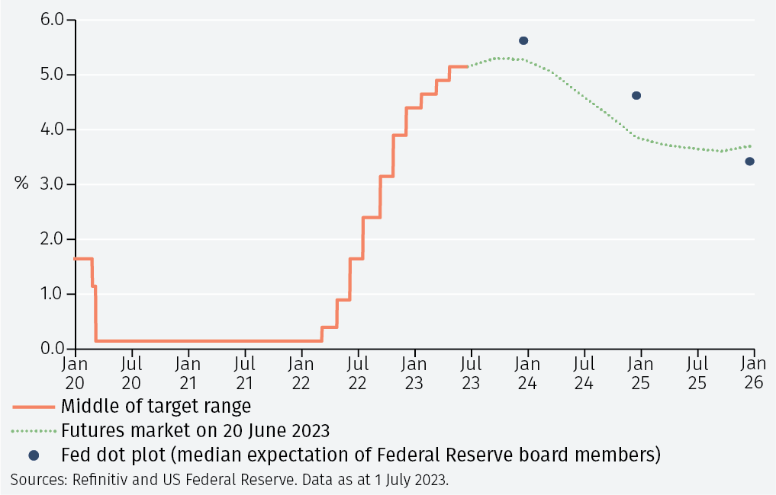

The interaction of market expectations and actual policy rate changes will remain a central feature in the rest of the year. If,for example, a US recession starts to seem more likely but the Fed continues on a path of higher rates (the ‘dot plot’ shown in Figure 5) market dislocation could result.

Calm equities, more nervous bonds

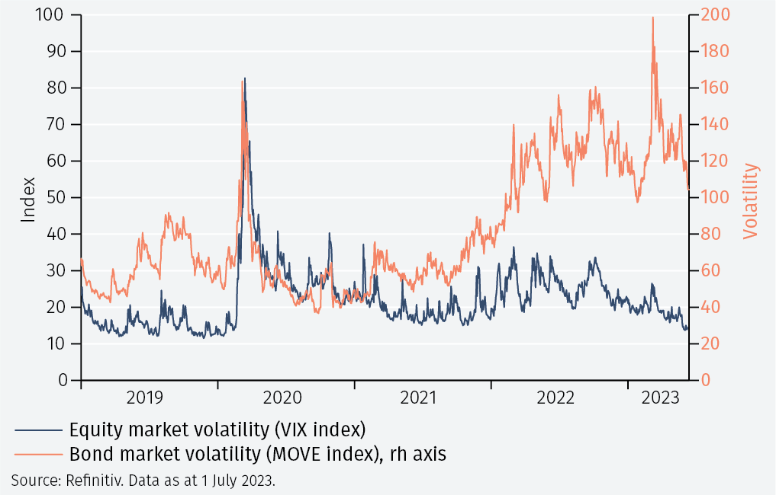

Having said that, some element of calm has returned to markets since the upheavals brought about by the banking sector problems earlier in the year. Lower volatility has been a particular feature of the equity market (see Figure 6) where the market’s ‘fear gauge’ – the VIX index of implied volatility – has returned to pre-pandemic lows. A similar measure for the bond market is still elevated but has recently trended lower.

These trends could, of course, be the calm before another storm. But we are cautiously optimistic that a new form of balance and equilibrium can be found in economies and markets over the rest of the year and into 2024.

To continue reading, please download the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.