- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the February edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The beginning of 2023 has been the opposite of 2022. Whereas last year markets started what eventually was a pronounced drawdown, this year optimism has so far prevailed. Both equity and bond markets have had a strong start to the year, driven by emerging markets, in particular Asia. The reopening of the Chinese economy after the end of the zero-Covid policy and the willingness of authorities to support the economy, including the real estate sector, buoyed market sentiment. The effect was visible in the outperformance of those markets more closely tied to China, like the eurozone.

The importance of the reopening of China is evident in the upward revisions to the IMF’s forecasts for global GDP growth. China, the second largest economy, is now expected to grow by 5.2% in 2023, 0.8% more than the IMF forecast last October. The positive spill over from the improved Chinese outlook reverberates across Asia and to the eurozone. Furthermore, the IMF has also revised up the US GDP outlook by 0.4% and now sees a reduced risk of recession.

The good news for markets includes ongoing evidence that inflation is abating. Thanks to falling energy prices and moderation in durable goods and services prices, inflation has fallen faster than central banks expected only a few weeks ago. Although the reopening of China risks putting renewed pressure on commodity prices, it will also help normalise global supply chains. While interest rates are set to rise further, the timing of a pivot to a more accommodative stance is drawing closer in most countries. The exception is Japan, where the Bank of Japan is still to start its normalisation process in earnest and risks temporarily upsetting markets.

In terms of portfolio allocation, a moderate overweight in equities and bonds remains warranted. However, given the uncertainties around Japanese monetary policy, it seems advisable to trim the overweight in favour of Asian emerging markets.

Asset Allocation

Global Allocation

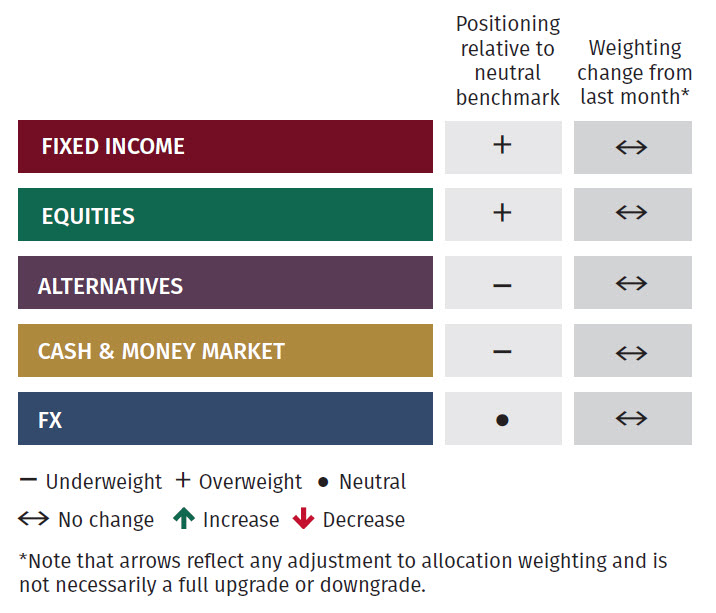

Based on a balanced mandate, the matrix below shows our 6-12 month view on investment strategy.

Economic activity continues to hold better than expected, evidenced by the recent set of economic data at the end of December. Markets had a strong start of 2023, with European stocks outperforming US markets and a strong rebound in Asian stocks following positive news from China. The weakening trend of the US dollar has extended into the new year, contributing to the strength of the euro and the pound sterling.

No changes were made to the broad asset allocation this month. We remain positioned with a slight overweight allocation into equities and fixed income versus the neutral benchmark allocation and an underweight in the exposure to alternatives and cash.

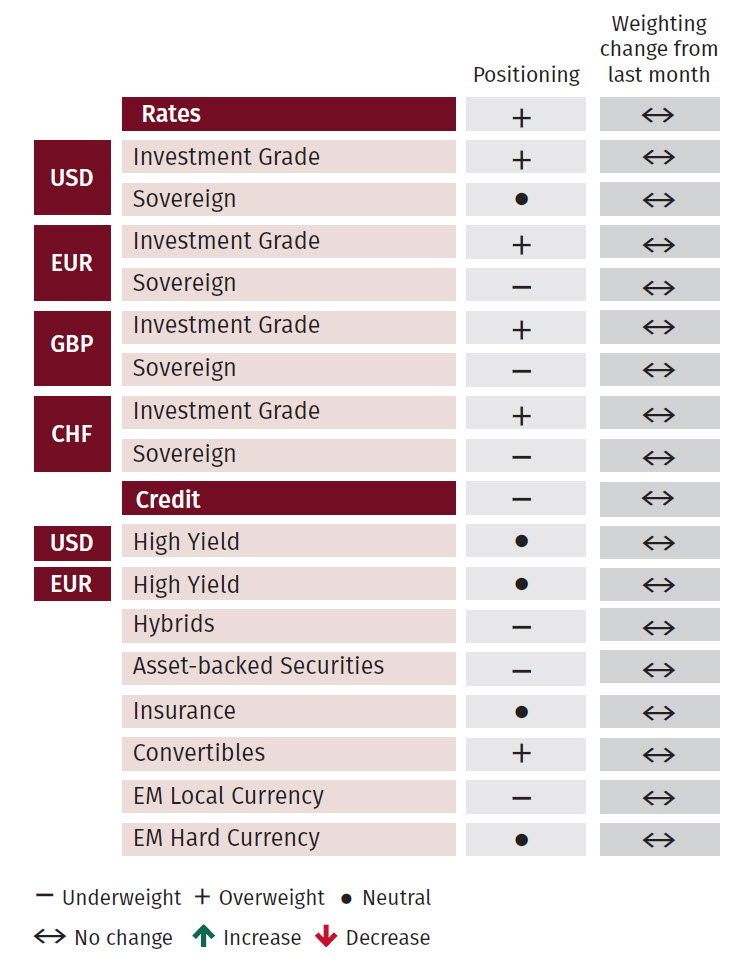

Fixed Income

No changes were made to our fixed income positioning, maintaining a small overweight position. Within emerging markets, there remains a preference for hard currency denominated debt but we could start to look into specific issuers in local currency given the US dollar weakness. We continue to be underweight in hybrids, asset-backed securities and all sovereign rates, apart from US sovereigns.

Although US high yield spreads have come down, these do not yet warrant an overweight position given recession risks and the potential for further widening providing a better entry point. European high yield looks more attractive in our view, warranting a preference in favour of Europe versus US high yield.

Equities

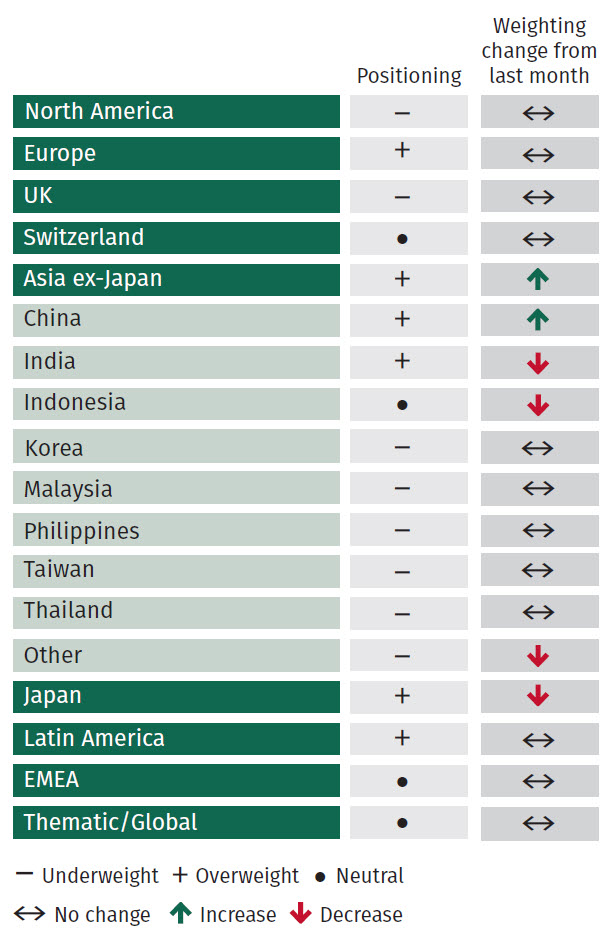

Within equities we have maintained a slight overweight position relative to the benchmark, with equity markets having a strong start to the year, particularly in Europe where we maintain a small overweight. Despite the recent rally, our analysis shows that stocks valuations have not changed significantly in comparison to the previous month, with most areas remaining cheap to neutral.

Consensus expectations have moved and currently expect the Federal Reserve to hike interest rates by 25bps at their next meeting in February, although Fed Chair Jerome Powell is expected to maintain a hawkish tone after the meeting to convey markets that the fight against inflation is not over yet. No action was taken on US equities at this point, maintaining the current underweight position. We will look to potentially reduce exposure to US, depending on the Fed’s comments and subsequent market reaction. Within US equities, the consumer discretionary sector has been one of the best performers year-to-date, despite all other sectors showing very strong technical support.

We have increased our overweight exposure to Asia. Technical and macro factors have deteriorated in Japan, while some of the risks have improved in the rest of Asia following the reopening of the Chinese economy, supporting technical factors across sectors. As a result, we are reducing exposure to Japanese equities and adding into other Asian economies. This is mostly a reflection of better short-term opportunities in Asia rather than Japan. However, it is important to note that we still hold a modest overweight position in Japan and remain supportive of the outlook for the rest of the year.

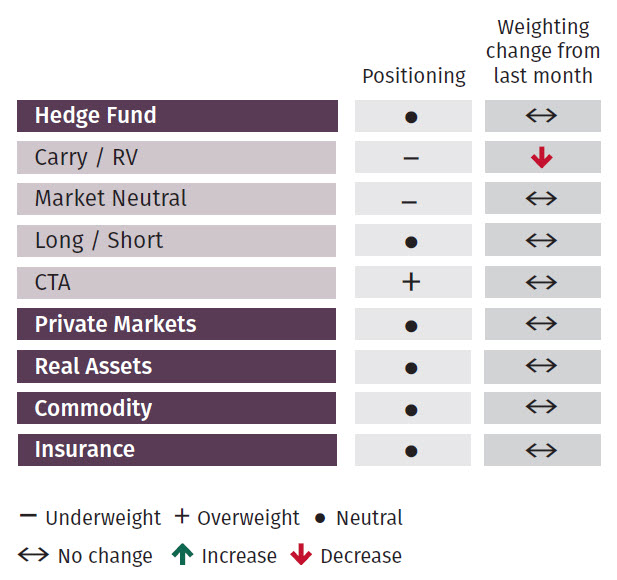

Alternatives

We maintain our concerns regarding the Real Estate sector. We are worried about the illiquidity of the sector and the gating of some products with direct exposure to commercial property. Additionally, the further deterioration expected in the sector warrant caution in the short-term exposure to real estate.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.