- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the March edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

After a strong start to the year for markets, the February consolidation was not a total surprise. As is often the case, a catalyst was required to justify some profit taking following the sizeable gains recorded since the October lows. That came in the form of stronger-than-expected data on the US economy, leading investors to reassess their assumptions about the future path of monetary policy.

In January, the US economy created many more jobs than expected, highlighting the ongoing strength of labour markets despite the lagged impact of last year’s monetary tightening. Furthermore, revisions to past inflation data and higher-than-expected prices in the services sector have made the path back to central banks’ targets more uncertain. Markets raised expectations regarding the level at which interest rates will peak and also the length of time they will stay there, pushing bond yields higher across the term structure. As has often been the case recently, the sell-off in bonds was associated with a correction in equity prices.

However, despite the negative market reaction, several factors continue to support a more favourable investment environment than last year. First, the improved economic data and the expectation that China’s reopening will support global growth means that the risk of a recession in the next few quarters has diminished. An improved growth outlook means fewer headwinds for corporate profits.

In addition, it is worth remembering that monthly data are volatile and we should not place too much emphasis on a single data point. Extrapolating from one inflation report misses the broader point that underlying inflation trends remain consistent with a progressive moderation in the remainder of 2023.

This means that, in terms of portfolio allocation, a moderate overweight in equities and bonds remains warranted in our view. Within equities, the UK market lagged other developed markets in January, reflecting expectations of a recession and ongoing challenges associated with Brexit. However, most of the bad news seems now priced in, including tighter monetary policy. This justifies a reduction in the underweight in UK equities, financed with the trimming of exposures to US and Swiss equities.

Asset Allocation

Global Allocation

After January’s strong performance across equity markets it was not surprising to see a consolidation in February. Emerging market stocks lagged, while European equities have continued to outperform within developed markets. There has been a pullback in fixed income assets, which remain particularly sensitive to any new economic data releases. The dollar index strengthened in February, reversing the trend of the previous four months, consistent with a more risk-adverse environment. However, the trade-weighted US dollar is still weaker in comparison to levels seen in most of the second half of 2022.

Uncertainty remains high in financial markets, with elevated levels of volatility, especially in fixed income. This is likely to persist for the time being until there is greater visibility regarding terminal central bank rates. As a result, we have decided not to make any changes to the broad asset allocation this month. We remain positioned with a slight overweight allocation in equities and fixed income versus the neutral benchmark allocation balanced by small underweights to alternatives and cash.

Fixed Income

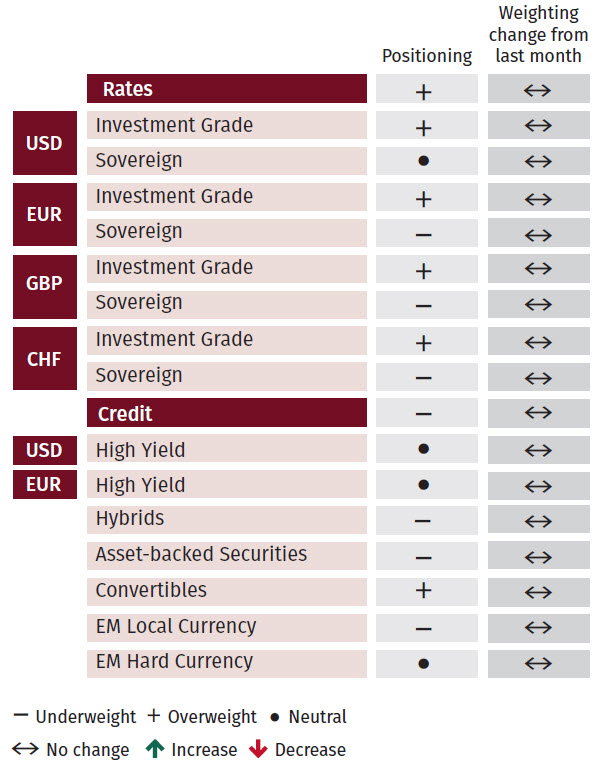

Fixed income assets have been unusually volatile this month, with sharp swings seen in response to various economic data points. Volatility is likely to persist for the time being until it becomes clearer where and when central banks will stop hiking rates. Against this background, no changes were made to our fixed income positioning, maintaining our modest overweight.

However, with yields having backed up sharply within a relatively short space of time, sovereign bonds are starting to look more appealing. For now, we remain underweight euro, Swiss franc and sterling sovereigns but neutral on US dollar rates.

Equities

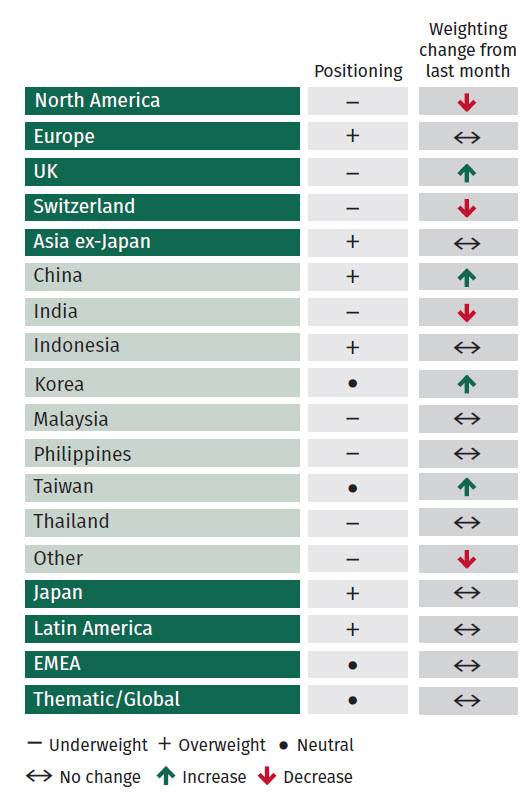

We added to our UK exposure although remain marginally underweight. The upward revision comes as technical trends appear strong alongside an improvement in economic data and the recent strength in the pound. To fund this our exposure to both Swiss and US equities was slightly reduced. While the move in US equities is small this builds upon previous moves to cut our exposure given the slowdown in the economy.

There has been an increase in risk in Latin America, related in particular to political noise in Brazil. While there has been negative news around the collapse of a Brazilian retailer, so far there has been no evidence of contagion to other Brazilian corporates. For now, we see no action required and therefore, maintain a modest overweight to Latin America.

We continue to hold an Asia ex-Japan overweight, primarily due to our preference for Chinese equities. Stabilisation of Chinese equity performance was anticipated given the seasonality around Chinese New Year. The China re-opening should continue to provide positive support to European equities.

Alternatives

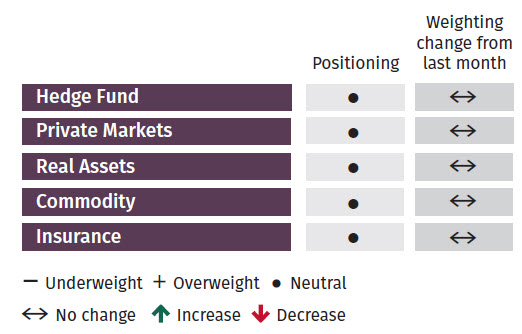

No changes were made to our alternatives exposure this month. We remain cautious on the real estate sector owing to liquidity concerns. Commodity positioning is neutral, noting that oil continues to trend lower, as demand from China is still not yet materialising into the energy sector.

Within hedge funds, heightened volatility stemming from uncertainty in inflation and rates should be supportive for equity market neutral managers. Similarly, commodity trading advisor strategies are preferred in the context of more market volatility.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.