- Date:

- Author:

- Sam Jochim

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The 20th National Congress of the Chinese Communist Party (CCP) closed on 23 October, with President Xi emerging more powerful and surrounded by closer allies. In this Macro Flash Note, Sam Jochim discusses the potential implications of the weeklong event which outlined China’s economic and social plans for the next five years.

President Xi was re-elected to serve a third term as Chinese President during the CCP National Congress, a feat which would not have been possible without a change of law. Presidents had previously been limited to two five-year terms since 1982 but this law was abolished in 2018, when President Xi began his second term.

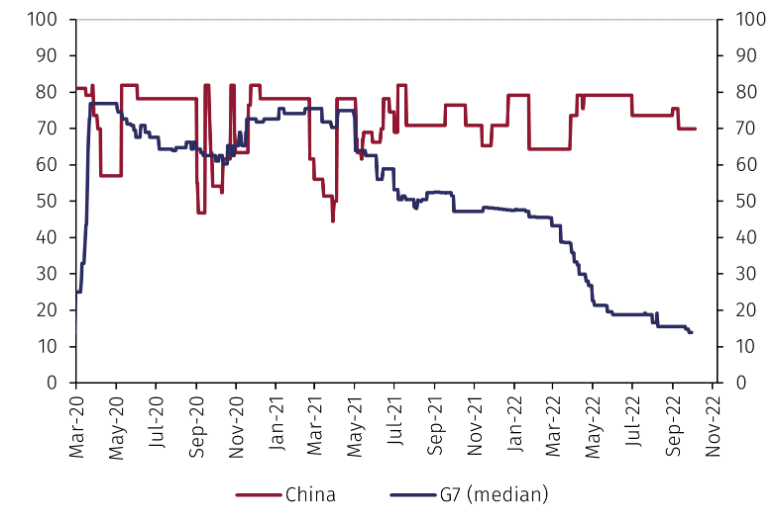

In opening the Congress, Xi gave a speech setting out China’s economic and social plans for the next five years. As expected, there was no hint of a pivot on China’s zero-Covid policy. Xi noted that China was putting life as the top priority and there was no wording that implied a balancing of the economic costs and benefits of this policy.1 This policy means that local lockdowns, which have a significant impact on economic activity in China, are enforced with a relatively small rise in Covid cases, a policy not pursued by most other countries (see Chart 1).2

Source: Our World in Data and EFGAM Calculations.3

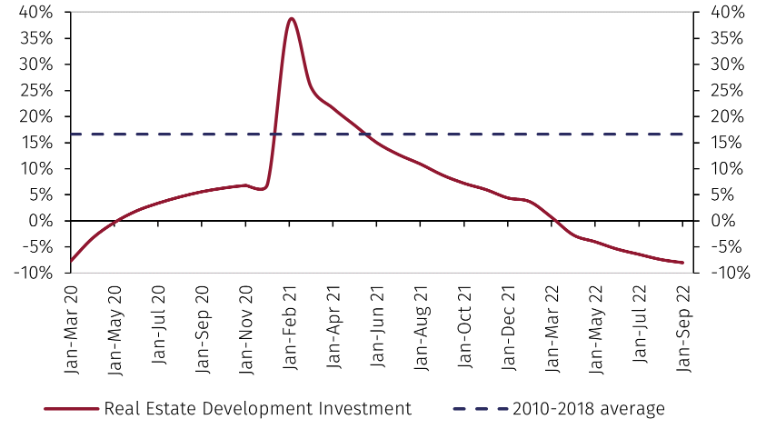

Xi only made one mention of the property sector in his speech. He pledged that the CCP will “move faster to build a housing system featuring multiple suppliers and various channels of support that encourages both housing rentals and purchases”. This implies that Beijing will increase fiscal stimulus to complete housing projects but there has been no sense of urgency to do this yet and there was no hint of a meaningful change in the future. Investment in real estate development has been slowing since February 2021 and has contracted since April 2022 (see Chart 2). Given the sector accounts for around 25% of gross value added in China, its recovery would be a significant boost for growth.4

Source: Refinitiv and EFGAM calculations.

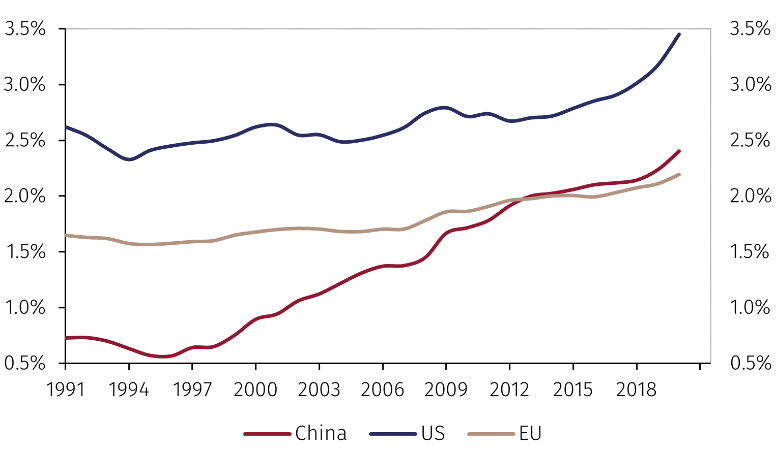

An entire section of Xi’s speech was devoted to the goals of making China a science and technology and advanced manufacturing power. Xi noted this policy is fundamental to China’s economic and supply chain resilience. Western governments now treat Chinese innovation as a matter of national security, with many boosting subsidies for industries such as chipmaking.5 It is no coincide that this is the industry of focus. With Taiwan accounting for 92% of the production of the most advanced semiconductors in 2020, it is clearly an industry with high geopolitical importance.6 In a speech to Chinese scientists in 2021, President Xi stated “technological innovation has become the main battlefield of the international strategic game”.7

The Biden administration has banned the sale of high-end chips to China both by US firms and foreign ones using American kit. This action is perhaps understandable given that China is highly unlikely to invade Taiwan until it has secured its supply of semiconductors. The US does not want China to be able to produce this technology independently, particularly before it can do so itself. China’s spending on research and development has increased dramatically since the turn of the century and given the importance of this policy to President Xi, this trajectory appears set to continue (see Chart 3).

Source: OECD

President Xi’s tone regarding Taiwan itself was unchanged from recent communications. It was not suggestive of any imminent invasion, which is unlikely before China has secured semiconductor supply chains. Xi reiterated China’s preference for resolving the issue peacefully but again did not renounce the use of force.

The Party Congress concluded on October 23rd with President Xi announcing the new seven-man Politburo Standing Committee and leading them on stage in rank order. There were two notable omissions from the previous selection in 2017. Li Keqiang, the premier of China was not included in the Standing Committee. He is seen as being outside Xi’s inner circle and was pushed into retiring in March 2023, before reaching the retirement age of 68. Wang Yang, a previous vice premier of China, who, like Li Keqiang, was not seen as a loyalist to Xi, was also demoted. Li Qiang, party secretary of Shanghai, is a close ally of Xi and was second on stage, implying he is in line to become premier in March next year.

Notably, there were no obvious successors to Xi in the Standing Committee line-up. A designated successor is usually young enough to serve one term in waiting and two terms as leader before the retirement age of 68. This indicates that Xi may intend to remain Chinese President for at least another 10 years, despite being 69 himself.

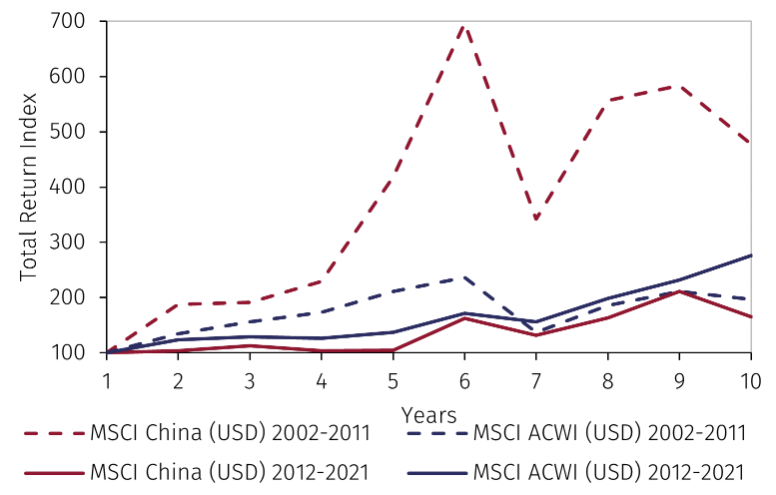

Markets reacted negatively to the Party Congress. MSCI China (USD) fell by 10.3% from the close of the Congress until the end of October. Over the same period, MSCI Asia Pac ex Japan (USD) returned -1.4%. Taking a longer-term view, MSCI China (USD) outperformed the MSCI ACWI (USD) by 280.4% in the 10 years prior to Xi’s initial election in 2012 (see Chart 4). This period was also associated with rapid growth of the Chinese economy, with annual GDP growth averaging 10.7% per year during that time. In the following 10 years under Xi’s leadership, MSCI China (USD) underperformed MSCI ACWI (USD) by 110.9%. It is important to note that much of this underperformance came in 2021, with MSCI China (USD) down 40.7% relative to MSCI ACWI (USD), and can be linked to China’s zero-Covid policy and struggling real estate sector. This situation could change rapidly if there were positive developments in these factors.

Source: Source: Refinitiv and EFGAM calculations. Past performance is not necessarily a guide to the future.

In summary, there were no near-term meaningful changes in policy implied in Xi’s speech from the CCP National Congress. There was an emphasis placed on science and technology dominance, which could play an important role both in driving future growth for China and in geopolitics, with China unlikely to invade Taiwan before its semiconductor supply is secure. One of the most notable outcomes of the Congress was that Xi fitted the seven-man Politburo Standing Committee with his closest allies, consolidating his power and possibly making room for another 10 years as President.

1 https://www.fmprc.gov.cn/eng/zxxx_662805/202210/t20221025_10791908.html

2 https://www.imf.org/en/Publications/WEO/Issues/2022/10/11/world-economic-outlook-october-2022

3 The stringency index is a composite measure based on nine response indicators including school closures, workplace closures, and travel banks, rescaled to a value from 0 to 100 (100=strictest).

4 https://thedocs.worldbank.org/en/doc/cb15f6d7442eadedf75bb95c4fdec1b3-0350012022/related/Global-Economic-Prospects-January-2022-Analysis-EAP.pdf

5 https://www.state.gov/the-passage-of-the-chips-and-science-act-of-2022/

6 See EFGAM Macro Flash Note, Taiwan caught in the middle of US-China power struggle (August 2022)

7 The Economist

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.