- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

US inflation is falling but the Federal Reserve remains determined to keep raising interest rates. In recent speeches, Chairman Powell focused on the high prices of services ex-housing and their link to wage inflation. In this Macro Flash Note, GianLuigi Mandruzzato analyses the latest data and concludes that the return of inflation to 2% may be closer than the Fed anticipates.

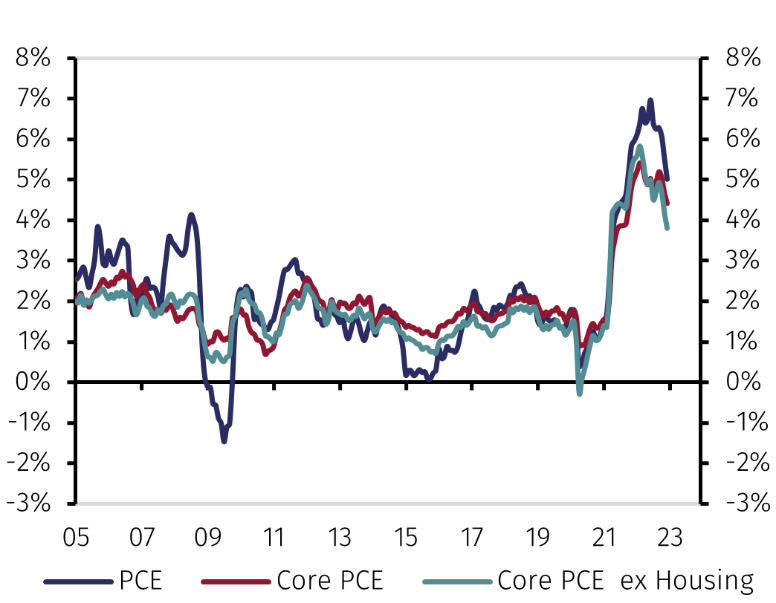

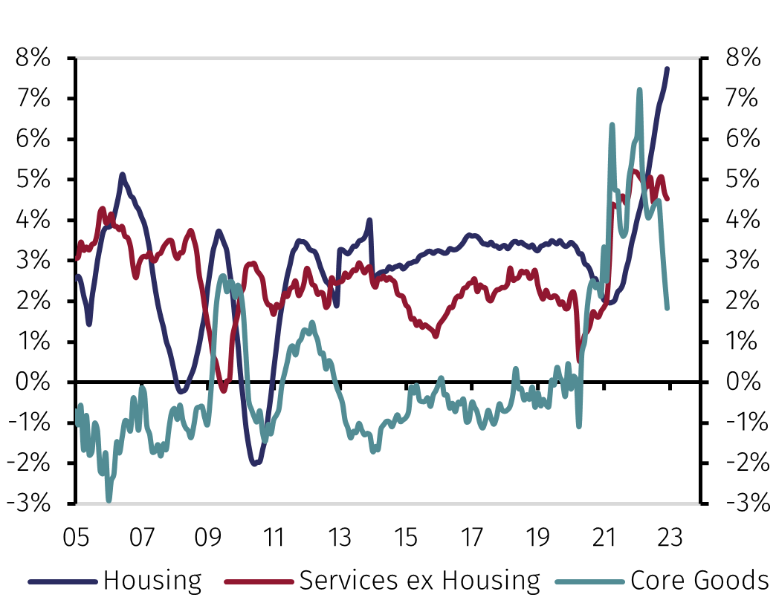

Federal Reserve Chairman, Jerome Powell, has signalled that although the disinflation process has begun, inflation is still high (see Chart 1a) and interest rates must rise further to return it to the 2% target. Powell has highlighted differences between the main groups within the core PCE deflator: housing, other services ex-housing, and core goods, i.e. excluding energy and food (see Chart 1b).

Source: Refinitiv and EFGAM calculations.

He has noted that the recent decline in annual core PCE inflation was almost entirely due to goods prices. In contrast, housing PCE grew strongly but Powell expressed confidence that the decline in new rents and house prices seen in recent months will soon be reflected in the PCE deflator. Overall, the Fed considers that monetary policy has achieved its intended effect on these two spending items.

Conversely, the Fed sees little progress in the rate of change of prices of services ex-housing, which represents almost 60% of the core PCE and includes healthcare, transportation, and leisure services. According to Powell, prices in these areas show no signs of moderation and, therefore, call for tighter monetary policy.

Powell also stressed the risks stemming from high wage inflation. Labour is the main productive input in services and rising wages are likely to encourage firms to raise prices, keeping overall inflation high.

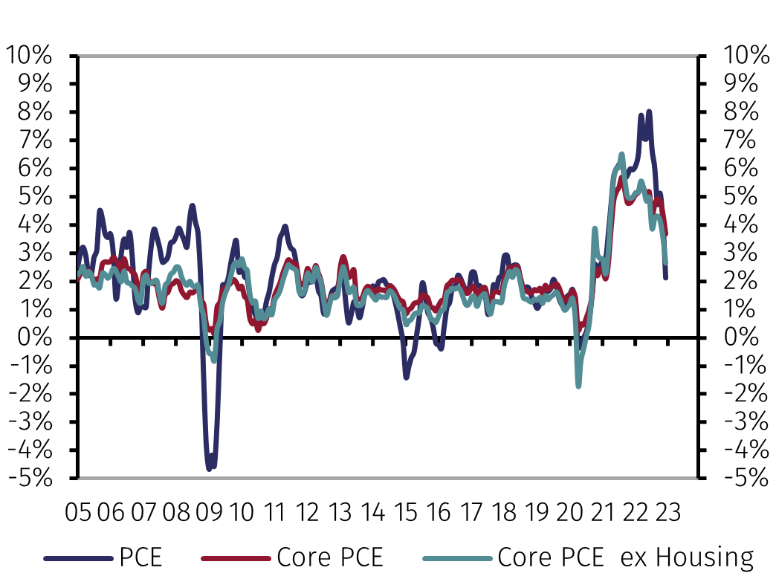

However, the latest data are more encouraging than the Fed's comments suggest. Charts 2a and b show the six-month annualised changes in the main components of the PCE deflator. Chart 2a shows that after peaking at 6% in late 2021, core inflation fell below 4% in 2022H2.

Source: Refinitiv and EFGAM calculations.

Furthermore, the core PCE deflator ex-housing only rose at an annualised pace of around 2.5% in the second half of 2022, not far from the Fed's 2% target. The slowdown of housing prices from the 9% pace reached in December is expected to start no later than 2023Q2. This could cause the core PCE deflator to decline on a monthly basis and push the annual inflation rate below 2%.

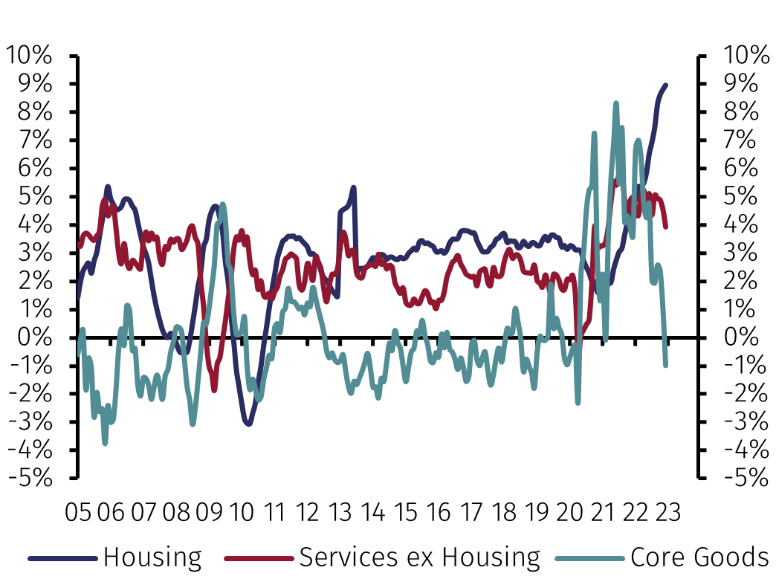

Goods prices are exerting a deflationary effect again, as they did before Covid. Chart 2b shows the anomaly in the period between mid-2020 and mid-2022 related to the surge in goods demand and the disruption of global supply chains seems to have ended.

Finally, Chart 2b shows that prices of services ex-housing have also moderated. After peaking near 6% in mid-2021, price increases fell to 3.8% in 2022H2. If this trend continues, the increase in the prices of services ex-housing will converge towards its pre-Covid trend rate, pushing overall inflation close to 2%.

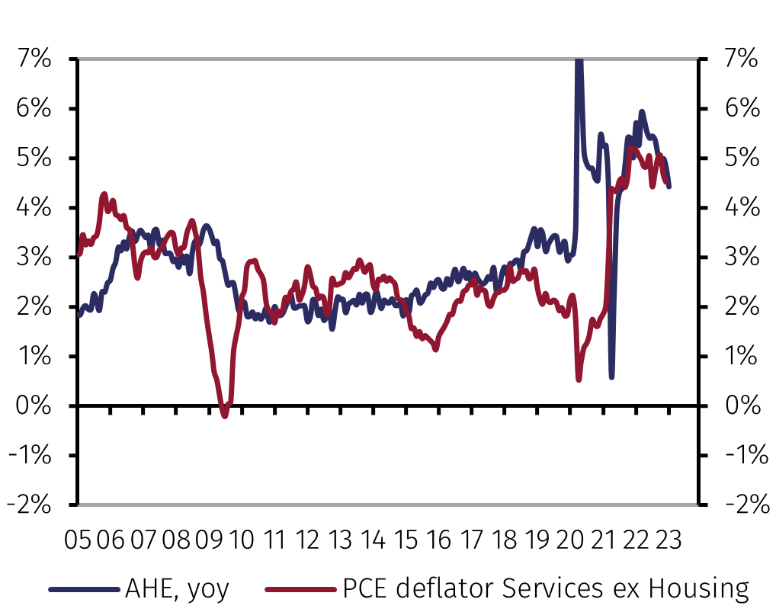

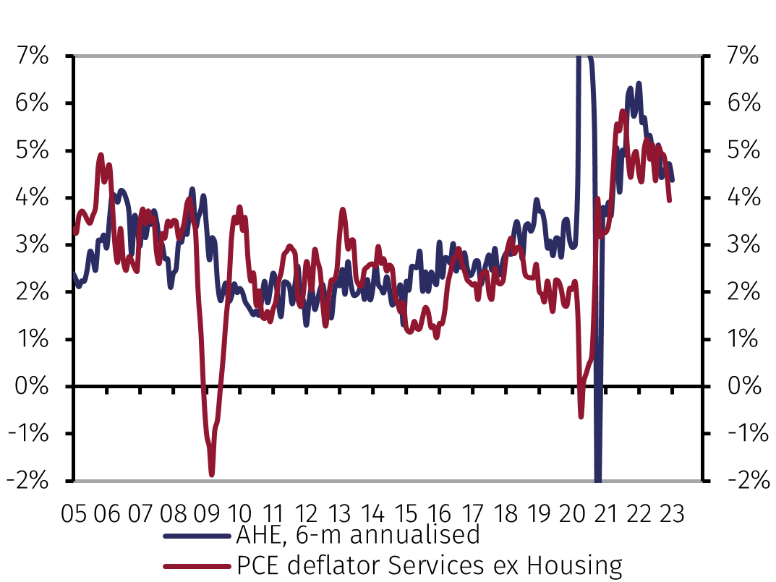

It is also notable that in 2022H2 the prices of services ex-housing fell faster than average hourly earnings (see Charts 3a and b). Historically, the correlation between hourly wages and the prices of services ex-housing is unstable and, if anything, it seems to have weakened after 2015.

Source: Refinitiv and EFGAM calculations.

In conclusion, Chairman Powell's latest statements indicate that the Fed links the need for tighter monetary policy to the prices of services ex-housing and it is therefore encouraging that the latest data show they are slowing. To confirm that the peak in US interest rates is drawing closer, it is crucial that this moderation continues in the upcoming data, starting with the January CPI released on 14 February.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.