- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Why has inflation risen much more in some countries in the eurozone than in others? In this Macro Flash Note, EFG chief economist Stefan Gerlach explores this issue.

Inflation continues its relentless rise across the eurozone. From a low of minus -0.3% in December 2020 it has risen to 7.4% in April of this year and is now much above the ECB's inflation objective of 2%.

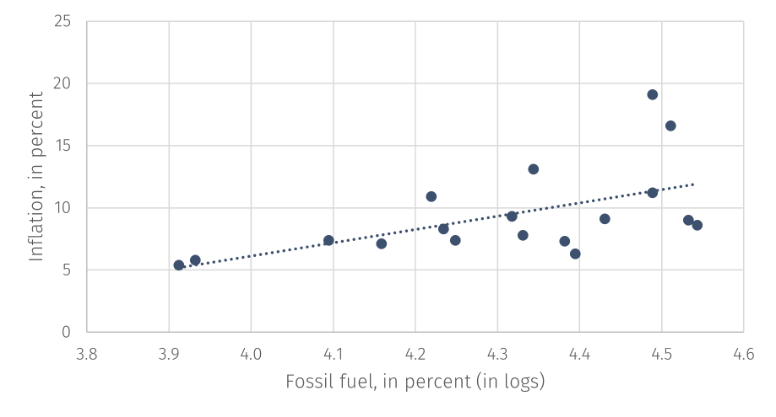

As shown in Figure 1, not only is inflation high but there is an extraordinary degree of dispersion of inflation across the member countries of the eurozone. Inflation in April ranged from 5.4% in France and in Malta to 16.6% in Lithuania and 19.1% in Estonia. The interquartile range of inflation reached 3.8% in March and in April, the highest level observed at least since 2000.

This surge in inflation is the reason why the ECB is preparing to stop its asset purchases and raise interest rates for the first time since 2011. In thinking about the monetary policy implications of this development it is important to have a clear understanding of whether the rise in inflation is due to sharp increases in demand for goods and services or a contraction in the economy's capacity to supply output at the going price level, caused by higher production costs or supply chain problems.

To address that question, it is useful to ask what factors can explain the exceptional rise and divergence of inflation in the eurozone. The public debate has focused on two factors.

The first of these is the surge in prices of oil, gas and coal following the Russian invasion of Ukraine. Since the relative importance of fossil fuel – relative to hydro power, nuclear power and renewables – in energy supply varies between countries, this may explain part of the divergence of inflation.

The second factor is the disruption of economic relationships – involving trade, finance, the flow of workers and supply chains – between Russia and the economies of Europe caused by the war. Since the strength of economic relationships depends critically on the proximity of economies, one would expect that the geographical distance between the various eurozone economies and Russia might also help explain the spatial distribution of inflation across the eurozone.

Interestingly, these two hypotheses are supported by the data. As shown in Figure 1, the correlation between inflation across the eurozone and the fraction of energy that comes from fossil fuels is very high at 0.57. Thus, countries that use a lot of fossil fuel have seen sharper increases in inflation.

Source: ourworldindata.org/energy-mix and www.euro-area-statistics.org. Data as of 19 May 2022.

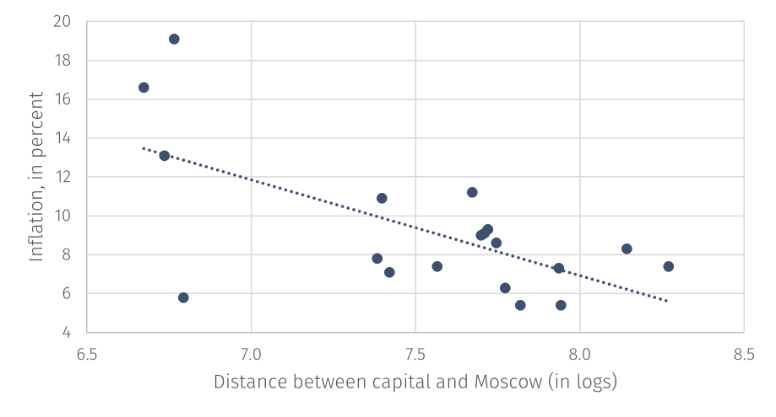

Furthermore, Figure 2 shows that the correlation between inflation across the eurozone and the distance to Russia, measured as the direct distance between the capitals of the different eurozone countries and Moscow, is also very high (-0.57). Thus, eurozone economies closer to Russia have indeed experienced a greater increase in inflation, arguably because they have suffered greater economic dislocation because of the war.

Source: www.distancefromto.net and www.euro-area-statistics.org. Data as of 19 May 2022.

Taken together, these two factors explain about half of the variation of inflation across the eurozone.

It is therefore apparent that eurozone inflation is unlikely to decline meaningfully until either fossil fuel prices fall or the economic dislocation associated with the war in Ukraine is partially or wholly resolved.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.