- Date:

- Author:

- Stefan Gerlach

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

In a unanimous decision at its 22 March meeting and as expected, the Federal Reserve brushed aside concerns about the state of the US banking system and the risk of financial instability, raising interest rates by 0.25% to the range 4.75% - 5%. However, it changed its language in a dovish direction. While it previously said that “ongoing increases in the target range will be appropriate” it softened that to “some additional policy firming may be appropriate". Chair Powell emphasised in the press conference the words “some” and “may” and that this change in language was due to the high degree of uncertainty arising from recent banking tensions.

Chair Powell stated that the US banking system is “sound and resilient” but acknowledged that credit conditions are likely to tighten as a consequence of recent events. That will lower inflation pressures, economic activity and employment, although the extent to which it will do so is highly uncertain. Nevertheless, the Fed does not expect that these tensions will have important macroeconomic effects.

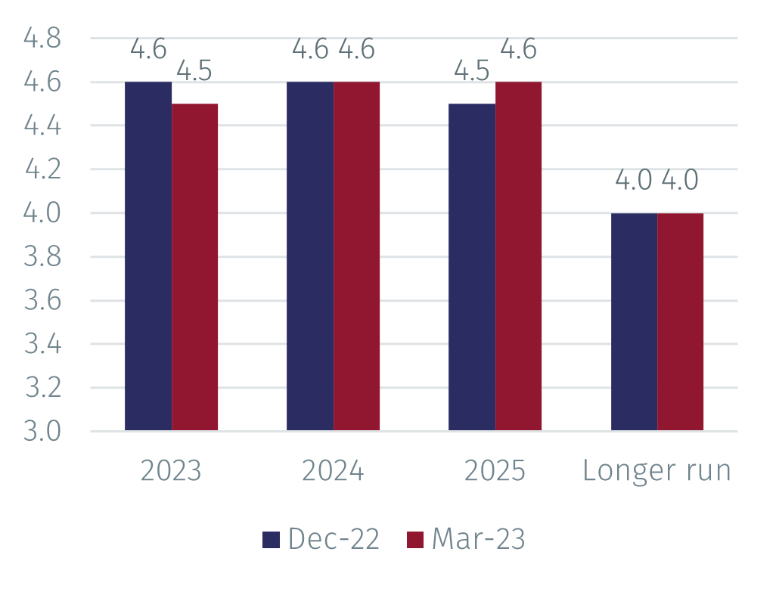

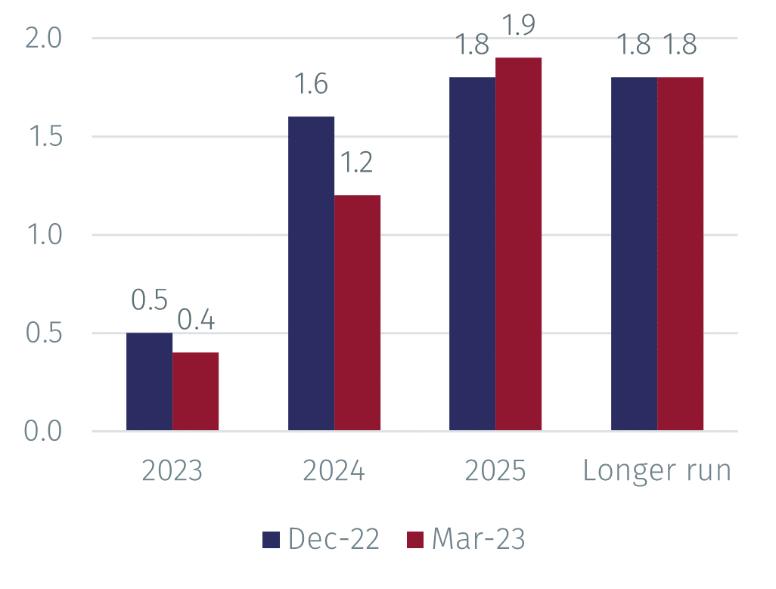

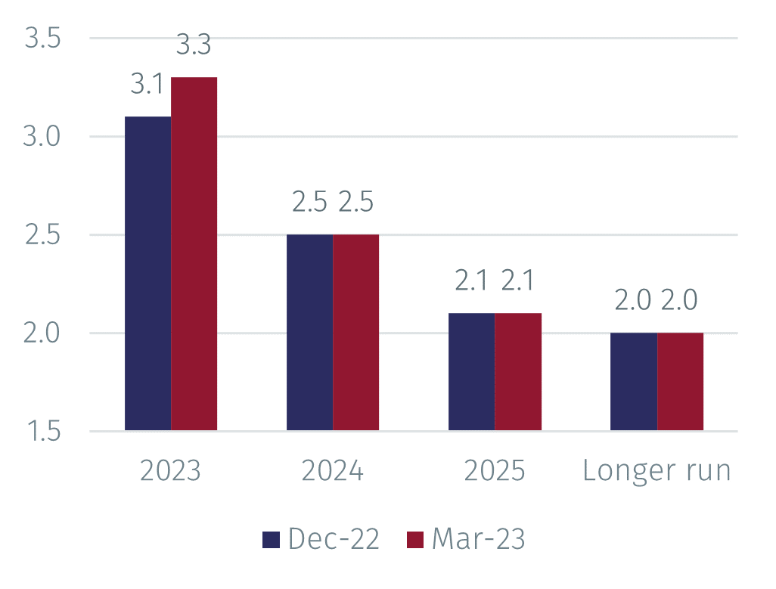

The Federal Open Market Committee (FOMC) projections (see charts below) were almost entirely unchanged. The median FOMC member expects unemployment to fluctuate around 4.5% in 2023-25, but to fall to 4% in the longer run. PCE inflation is expected to be 3.3% in 2023, 2.5% in 2024, 2.1% in 2025, and 2% in the longer run. Real GDP growth is expected to be 0.4% in 2023, 1.2% in 2024, 1.9% in 2025, and 1.8% in the longer run.

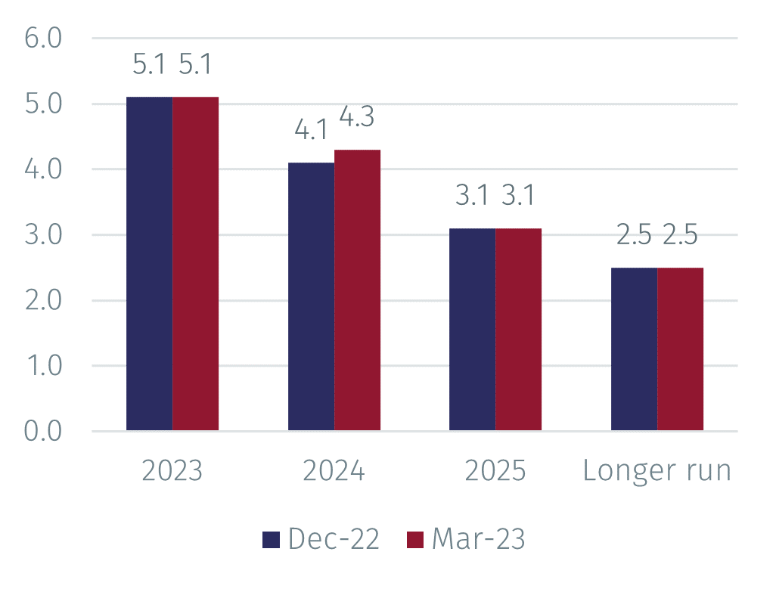

Interest rate projections were remarkably unaffected by recent developments. The median FOMC member expects interest rates at the end of 2023 to reach 5.1%, that is, they expect one further 0.25% increase. The median projection for 2024 is 4.3%, for 2025 3.1% and in the longer run 2.5%.

Source: Federal Reserve Board. Data as of 22 March 2023.

Overall, the tone of the press conference was surprisingly upbeat – no doubt many commentators expected the Fed to view worries about the banking systems as likely to have a greater impact on the economy. Indeed, according to the CME Fed Watch Tool, immediately after the meeting financial markets were pricing two interest rate cuts during the year, presumably because they expect inflation pressures to abate and economic activity to slow more rapidly than the Fed.

In recent weeks fixed income markets have been exceptionally volatile, reflecting sharp shifts in market rate expectations about the outlook for monetary policy. Such shifts are normal at inflection points in the interest rate cycle, although even by historic standards the shifts in this cycle have been unusually large. Depending on the incoming macroeconomic data, further shifts in expectations are likely to occur over the coming weeks until the outlook for policy has become clearer.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.