- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

March data on the US labour market and inflation support a 0.25% increase in the fed funds rate at the May Federal Open Market Committee meeting. In this Macro Flash Note, GianLuigi Mandruzzato summarises the key insights from the latest releases.

The message from the March labour market and CPI data is that the US economy remains robust and inflation is not falling fast enough. The Federal Reserve cannot yet declare victory over inflation and an 0.25% increase in the fed funds rate at its May meeting is likely.

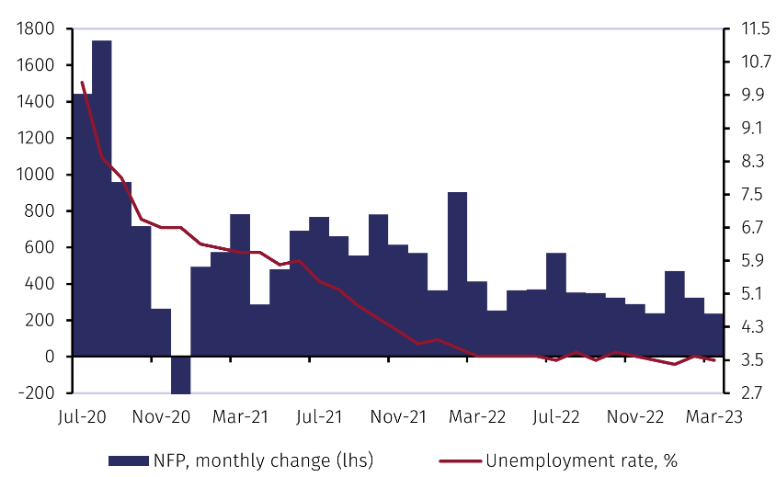

The resilience of employment, which grew by 236k, decreased worries of an imminent recession (see Chart 1). Although the job market lags the business cycle, it is nonetheless notable that the unemployment rate fell to 3.5%. Another positive in the job market report is the moderation in wage growth to 4.2% year-on-year, the smallest increase in almost two years.

Source: Refinitiv and EFGAM calculations.

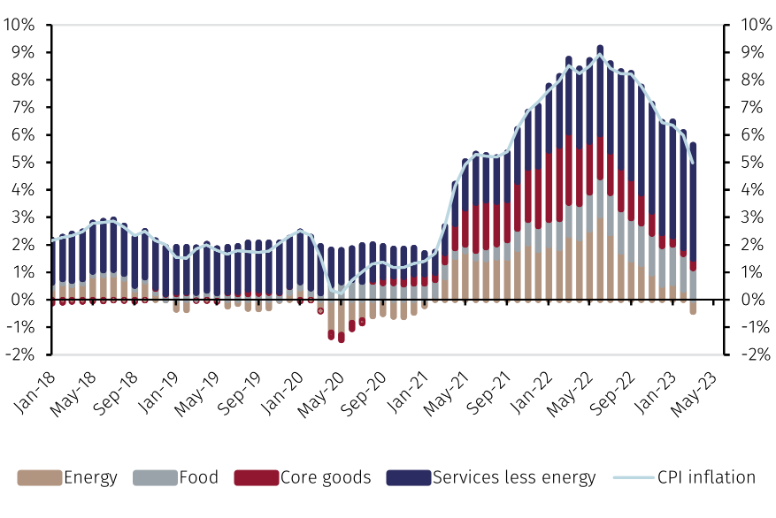

The CPI data only partially reassured markets on the inflation outlook. Headline inflation dropped to 5% yoy, the lowest since May 2021, but remains well above the Fed’s 2% target (see Chart 2). The fall was due to energy and food prices; excluding these items, core inflation rose to 5.6% yoy. Furthermore, the core CPI increased 0.38% month-on-month, more than double the monthly rate consistent with the Fed's definition of price stability.

Source: Refinitiv and EFGAM calculations.

Once again, core inflation was boosted by the shelter component, which rose 0.6% mom. However, this is a moderation from recent months and suggests that, with the usual lag compared to property prices, housing prices will soon become disinflationary.

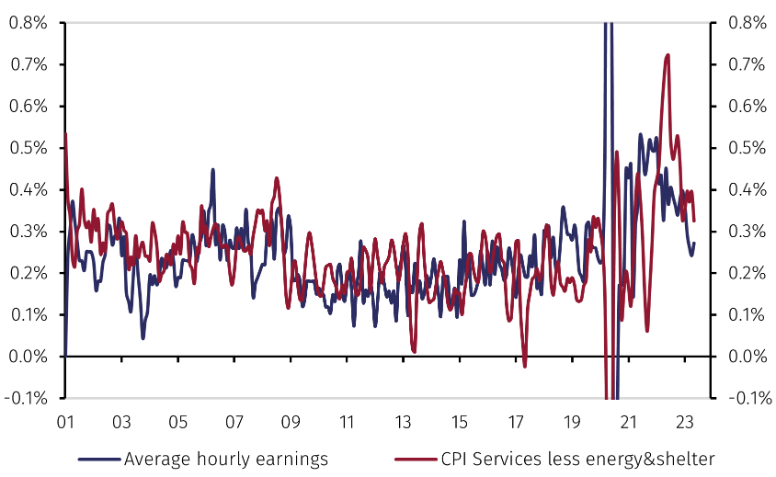

However, upward pressures on underlying inflation remain. Prices of core services, excluding shelter and energy, slowed to 5.9% yoy, but their rise is still too rapid. Furthermore, while the March monthly increase moderated from February, the average of the last three months was 0.37%, up from 0.33% in the three months to December (see Chart 3). The minutes of the March FOMC meeting report that participants saw "little evidence" that core services inflation was slowing, and the latest CPI data confirms that conclusion.

The Fed has recently linked inflation in core services to sustained wage growth. The slowdown in the latter could therefore be encouraging. However, it is not clear whether wage developments influence the prices of core services (see Chart 3). In the period since 2001, the correlation between the quarterly average of the monthly changes in wages and the core services CPI is slightly negative, and this is true also in the post-Covid period.1

Source: Refinitiv and EFGAM calculations.

In conclusion, March labour market and CPI data show a still healthy US economy, despite the banking sector turmoil, and sustained inflation. It is too early for the Federal Reserve to conclude that the current level of the fed funds rates will bring inflation back to 2%. Another 0.25% hike at the May meeting looks likely, but increased uncertainty over the economic outlook suggests the Fed will keep all options open at subsequent meetings.

1 In the sample period January 2001-March 2023, the estimation of a VAR(3) on the quarterly average of monthly changes in core wages and prices shows that the cumulated impulse response of core services prices to a standard shock to wages is not statistically significant . Rather, the Granger causality test suggests that the two variables influence each other.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.